Lending a Hand

Your adult child would not have to pay the fees associated with a residential mortgage loan through a bank if you provide the loan at a lower interest rate than commercial lenders would charge. Also, the loan is as an income-generating asset in the fixed-income portion of your investment portfolio, says Jeremy A. Altfeder, CFP®, senior financial advisor at CAPTRUST.

An intra-family loan, in the right circumstances, can be “a really easy tool for parents looking for a way to do something nice for their children,” Altfeder says.

First Steps

This is not a do-it-yourself proposition, especially given the potential tax, legal, and other complications, says Lauren Campbell Maxie, an attorney and partner at NC Planning in North Carolina, whose primary practice area is estate planning for high-net-worth families.

Maxie says she gets the parents involved in a strategic discussion at the start, including their legal advisor, financial advisor, and others, to make sure they understand the details. She also brings in the prospective borrower early on, making sure he or she understands the benefits and obligations. “We tell them it’s a loan, not a gift, and that it has to be repaid,” Maxie says.

Parents may be uncomfortable with formalizing the loan, and they may not want the added expense of engaging various advisors, says Eric L. Green, an attorney with Green & Sklarz LLC, a Connecticut-based law firm, whose practice includes taxpayer representation before the Internal Revenue Service (IRS).

“But the reality is, if you do it correctly, you’re protecting your investment—and protecting the child” from creditors or would-be creditors, says Green, author of The Accountant’s Guide to IRS Collection.

“Everyone hates lawyers. I’m a lawyer, and I hate lawyers. But you’ve got to take the proper steps,” he says. For example, have the loan and related documents formally drawn up, signed, and officially recorded. That also helps avoid family fights down the road. “You don’t want a family to rip itself to pieces” over financial disagreements later on, he says. Also, keep track in writing of each payment to avoid unfavorable tax treatment.

Overall, you have to take a step back and make sure that the intra-family loan is the right fit for all involved, “because there’s lots of tools in the toolbox,” Maxie says. Altfeder agrees, saying, “It’s all about it financially making sense for both parties.”

A True Loan—with Interest

An intra-family loan must be a true loan, not a gift. Otherwise, it can trigger tax snags. To avoid such problems, charge at least a minimum amount of interest, using the rate from the table of applicable federal rates published monthly by the IRS.

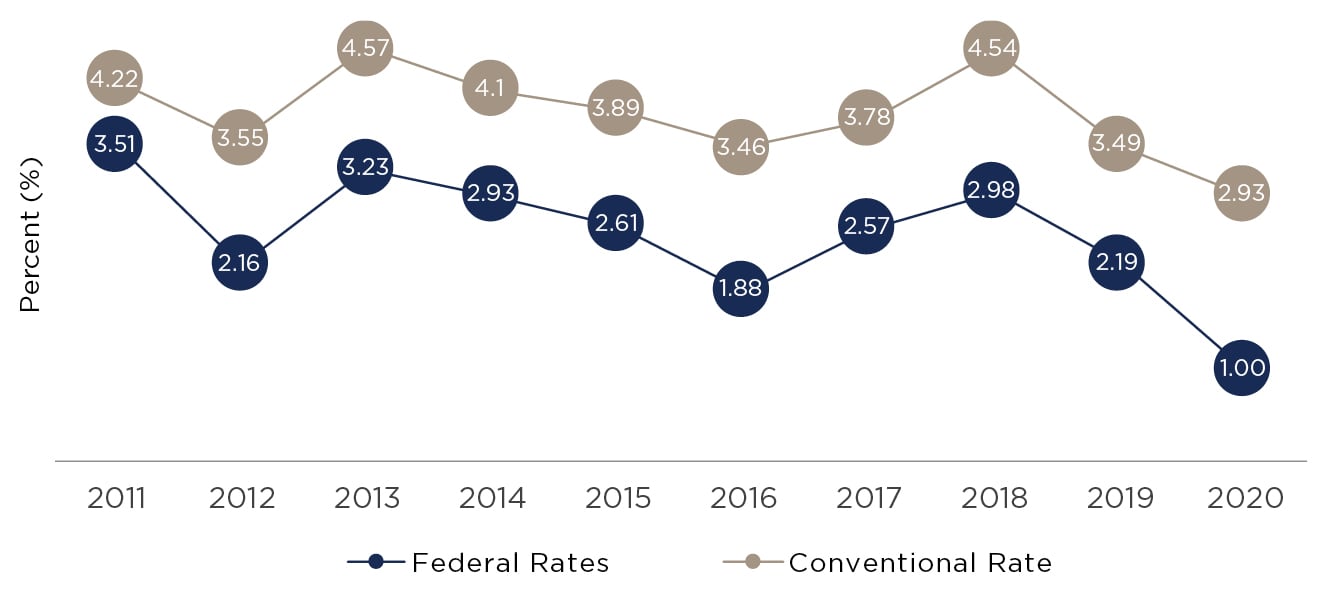

Conventional rates for 30-year, fixed-rate residential mortgages lately have been among the lowest in at least 10 years—and the applicable federal rates for long-term intra-family loans have been even lower, as shown in the rate survey illustrated in Figure One.

Figure One: Interest Rates for Conventional Mortgage versus Applicable Federal Rates for Intra-Family Loans

Sources: Freddie Mac, Internal Revenue Service. Data is for 30-year fixed rate as of first week in September of each year. Data for conventional (i.e., bank) loans is based on Freddie Mac survey. Data for intra-family loans uses Internal Revenue Service’s long-term applicable federal rate.

At the time of the survey, the average fixed rate charged by banks was 2.93 percent, while the applicable federal rate for a long-term intra-family loan rate was 1 percent. That makes the intra-family loan “a great tool to look at while we’re in this low-interest-rate environment,” Maxie says.

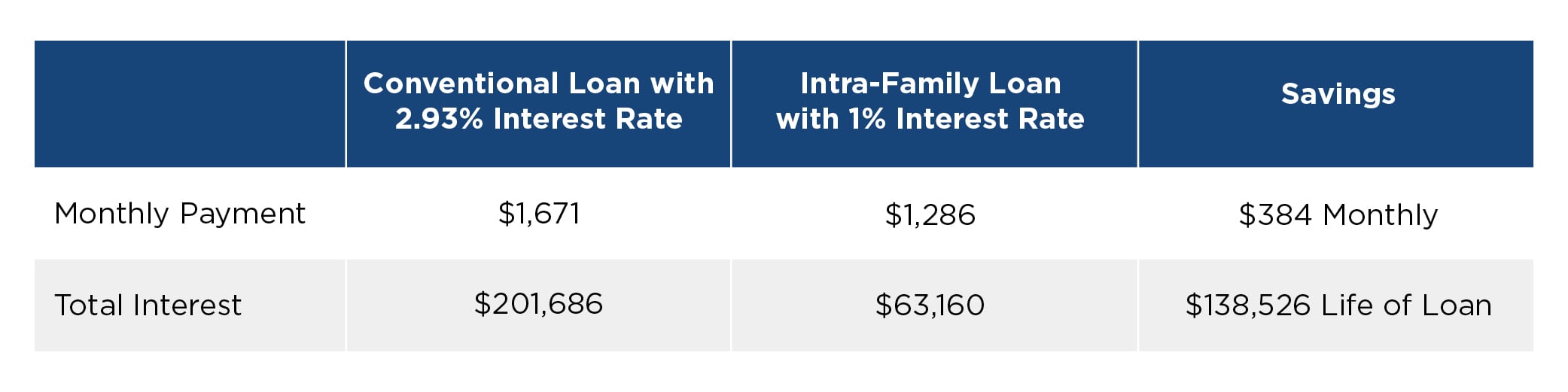

Suppose Harold and Maude plan to lend their son, Bud, $400,000 to buy a house. With a conventional 30-year, fixed-rate loan of 2.93 percent, he might pay about $1,671 a month in principal and interest as shown in Figure Two. But if he takes the loan from his parents, who use the long-term applicable federal rate of 1 percent, he’ll pay about $1,287 a month—saving about $384 monthly.

Figure Two: 30-Year Residential Mortgage versus Intra-Family Loan

Sources: Freddie Mac, Internal Revenue Service

Over the life of the loan, he’d pay about $201,687 in interest on the conventional mortgage, but about $63,161 on the intra-family loan—saving about $138,526 in interest expense overall.

An intra-family loan can also be from a grandparent, aunt, uncle, or any high-net-worth family member to a child or other relative. Such loans aren’t just for mortgages. They can also help the child or other relative pay college expenses, start a business, or accomplish other long-term family goals.

By following the proper procedures, no federal gift tax will apply and the interest paid by the adult child can generally be deductible as personal mortgage interest or as a business expense (depending on the purpose of the loan and other factors). And the interest received by the parent will be treated as ordinary income.

Flexibility

Intra-family loans can be more flexible than working with a bank, Maxie says. For instance, you can structure the loan as interest-only, with a balloon payment at the end, she says.

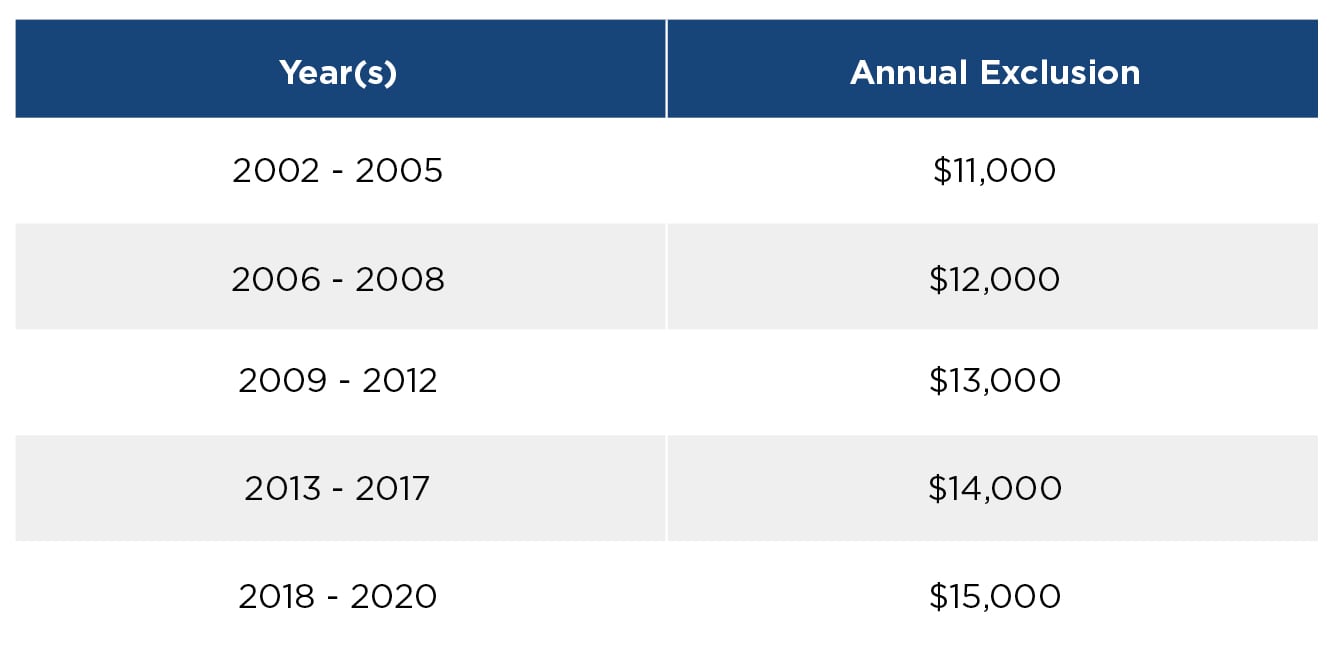

Another option is for parents to forgive some principal, perhaps annually, Altfeder says. Forgiving some principal on the back end can be the “icing on the cake,” turning a 30-year loan into a 15-year or 10-year loan, he says. Altfeder explains that to avoid federal gift-tax complications, be sure that the portion of the principal you forgive is within the annual federal gift-tax limit.

The annual limit—the annual exclusion—applies to each person to whom a gift is made and can increase each year, as shown in Figure Three. For 2020, the limit is $15,000 and the total amount of the gift can double if both spouses agree. In our example, Harold and Maude could forgive up to $30,000 of the loan’s principal each year, with no federal gift-tax consequences.

Figure Three: Federal Gift Tax Annual Exclusion Amount

Source: Internal Revenue Service

Suitability

An intra-family loan is best suited for those who can afford to offer it—typically high-net-worth couples who have a portfolio that sustains them in retirement and who are looking to help their adult children with a life-cycle event, such as buying a house or starting a business, Altfeder says.

Maxie says it’s not suitable if the parents need cash flow, or if the loan would affect the parents’ retirement. And according to Altfeder, he typically only recommends intra-family loans if the parents have at least $3 million to $5 million of liquid net worth.

Consider family issues, too. You may want to avoid making a loan if “it’s going to cause a big upheaval” in the family, Maxie says. Make sure that the family member borrowing the money will be in a position to repay it consistently. Overall, the intra-family loan is “a great tool. It’s just got to make sense for the family,” Maxie says.

Risks

Understand the risks involved. At the top of the list: “The kids stop paying,” Altfeder says. Family relations may suffer, too. So, follow the proper procedures from the start.

If the money is for buying a house, make sure the loan is formalized, with the various parties signing all of the mortgage, security, and related documents that would be involved if a bank were doing the loan, including having the formalized mortgage recorded in the local land-office records, Green says.

The same principle applies if the loan is for another purpose, such as helping the adult child establish, buy, or expand a business. Make sure there’s a promissory note [the written promise to pay], and a security agreement [giving the lender a security interest in the assets], Green says. Be sure, too, that the terms of the security agreement are filed under the Uniform Commercial Code with the Secretary of State and the local land-office records, he adds.

Intra-family lending isn’t for everyone, but in the right circumstances, “It has the opportunity to be mutually beneficial to the parents and the children,” Altfeder says.

Just make sure to get professional advice first, understand the family dynamics and risks involved, and make sure the proper steps are followed.