Matching Your Investments With Your Financial Plan

By gaining a holistic picture of your financial life, including your goals and risk tolerance, a financial advisor can customize your investments to meet your unique needs and desires. They do it through a combination of inputs that include financial planning insights, capital market acumen, and tax perspective. Behind the scenes, the financial advisor is constantly trying to position each client’s portfolio so that it stands to benefit from a multitude of potential future events.

What difference does it make if your portfolio is 60 percent stock and 40 percent bonds versus 80 percent stock and 20 percent bonds?

Both portfolios might be equally likely to fund your retirement spending needs, but the difference may lie in what you leave behind. Or it could impact how much flexibility you will have to indulge in things like an 80th birthday cruise around the world, a large donation to charity, or the decision to fund a grandchild’s education.

“Imagine three buckets,” says Mark Feldman, CAPTRUST principal and head of tax services. “The first bucket is the one that’s going to take care of you for the rest of your life, so those assets are going to be invested more conservatively. We call this the capital preservation bucket.”

“The second bucket—the liquid risk bucket—contains more volatile investments to help grow the portfolio. And the third bucket—the illiquid risk bucket—contains assets that will grow the portfolio but are not able to be accessed immediately,” says Feldman. “If you know your needs are taken care of with the capital preservation bucket, you become more risk tolerant with the excess.”

By separating your assets into buckets like these, a financial advisor can craft an investment portfolio that’s personalized to meet your goals.

Planning for Investment Goals

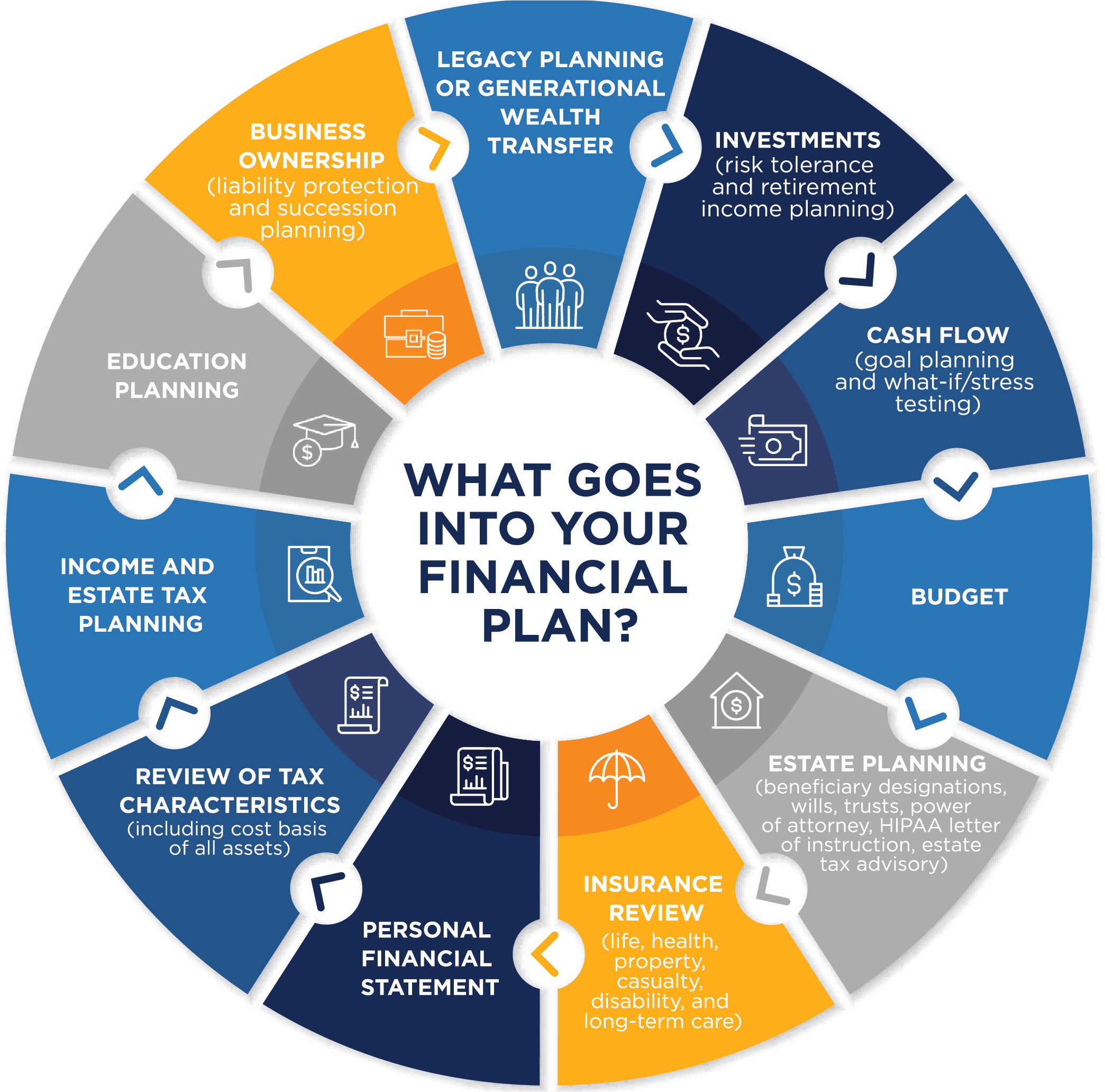

“We do the planning first,” says Briana Smith, CAPTRUST financial advisor. “Then the plan informs how we will manage the portfolio. First, we need to know your cash flow, your long- term legacy goals, your charitable intention—all those things. Then, we can align your portfolio appropriately to reach your goals.” A robust financial plan will take account of your income, expenses, investments, estate planning, insurance, taxes, and more.

Investment planning is one part of financial planning. It involves portfolio construction, selection of investments, monitoring, rebalancing, and trading for clients. It is the merging of investments with financial planning.

What is key, says Smith, is for the financial advisor to have a complete picture of your financial activities, needs, and goals.

The Investment Engine

To create that holistic picture, your financial advisor will strategize your unique investment plan, evaluating available investment portfolios to find the ones that best align with your goals and risk tolerance.

The hidden driver behind this investment plan is the investment team that designs each individual portfolio. This is the group of people responsible for doing deep research and weighing all the crosswinds—in the markets and the global economy—to guard portfolios against outsize losses that would compromise clients’ financial plans.

The investment group is always dealing with uncertainty, but it is also always planning and preparing for a wide range of outcomes. What happens in the markets if a war breaks out tomorrow? What happens if a war abruptly ends? The investment team faces the capital markets every day, making decisions about where they see opportunities and where they take risks, always with your interests in mind.

In other words, the investment team is responsible for developing a range of portfolio options with enough variety that your financial advisor can easily match your individual assets to the goals set by your financial plan. That means offering multiple investment engines that meet the needs and life goals of a large and diverse client base with unique tax profiles and circumstances. And it means balancing the risk and reward of any given security in a portfolio.

Proactive Tax Strategies

Perspectives from tax planning and advisory services are another big piece of the investment planning puzzle. To create a fully optimized investment plan, your financial advisor will pair your portfolio and investment opportunities with income tax strategies.

Eric Ensign, CAPTRUST financial advisor and tax consultant, says most people still think of doing a tax return as if it is only meant to take account of the past. “Most people are looking backward at the tax year that just occurred,” he says. “They’re usually not looking forward to the future with one eye on strategic tax planning.” That’s a potential missed opportunity.

The aha moment is when advisors can find synergies between tax planning, estate planning, and investment strategy that enrich your financial picture.

Tax advisory involves not only planning and strategizing but also considering tax implications and analyzing the tax impact of various investment strategies. As Jennifer Wertheim, CPA, a director of tax at CAPTRUST, explains, “Although tax might not be the biggest driver of a financial plan or financial decision, understanding and being aware of the potential consequences is important so that there aren’t surprises on the back end. If advisors can understand what your goals are, then they can plan and try to make your tax consequences complement the choices you’re making and the choices you plan to make in the future.”

Assembling Your Roundtable

Robust planning is simply not possible unless your financial advisor has all the necessary information at their fingertips, right when they need it. “Unless we’re looking at the tax return right next to the balance sheet,” says Feldman, “we’re going to miss the ways to connect them. We can save people more money when we view those two things together.”

Of course, that can mean more work upfront for you, namely in tracking down and uploading tax reports and account statements. But with recent technology, including secure files and uploads, it’s not as hard as it used to be.

The best-case scenario, says Jeremy Altfeder, CAPTRUST financial advisor, is when clients connect him directly to their other advisors, including tax professionals, insurance agents, estate attorneys, and more. “Then, if you are making big tax payments or moving money around, your CPA can just tell me what needs to happen and copy you on the conversation. Or the estate attorney can send documents directly to me so we can spare you the time and hassle. You probably don’t want to play the middleman, and frankly, you don’t have to,” he says.

This way, your financial advisor can act as a general contractor or project manager on your behalf.

Also, Altfeder says, “If it is only a financial advisor and a client working together, the voice of the financial advisor can sound a lot like the mom from the old Peanuts cartoons: ‘Wah wah wah.’ But when there are multiple perspectives from professionals with different expertise, that group of people is likely to generate better outcomes than one advisor alone.”

Creating this group of experts and putting them directly in touch with each other increases operational efficiency, reduces room for error, and can enhance the overall value of the advice. “You may be wary of bringing more advisors to the table,” says Wertheim, “because you haven’t needed to in the past, or you like to keep things simple, or you want to avoid fees. But having more people in the room—all your professional advisors talking to each other—adds tremendous long-term value that will exceed the short-term cost.”

Reducing Risk

What are the risks of not integrating your investment management with your tax and financial plans? In Feldman’s words, “Suboptimization of the options.” Or as Altfeder phrases it, “If your advisor can see only half of the picture, they can only give you half of the great advice.”

Wertheim agrees: “From a tax perspective, it could undermine your goals. If you aren’t aware that you are going to have a huge tax bill at the end of the year because of whatever strategies you’ve engaged in, it can leave you feeling very frustrated.”

“If you have a gain, yes, you’ll also have a tax bill at the end of the year, but hopefully we can minimize or strategize how to use that gain,” says Wertheim. “If you have a loss, that can also be beneficial. In fact, you might strategically plan to have a loss so that you can use it against something else. The key is to avoid unbeneficial losses.”

By integrating investments, planning, and tax, your advisors create a benchmark and can give you a clear-eyed vision of the future. You can practice scenarios so that you feel prepared. In this way, investment planning creates better outcomes, and it grows your confidence.

“We’re going to constantly test our assumptions about what the excess is,” says Feldman, “and we need you to guide us on how you want to allocate and design your plan. We need you to tell us what happens with the excess. And to the extent that we know there is excess, and the excess is unguarded by taxes, we look for ways to design the excess more tax-efficiently.”

Making Changes

For some investors, this type of long-term planning can feel prescriptive or limiting. Others wonder: What if this financial advisor isn’t the right one for me? What if I change my mind in five years? Remember that nothing is set in stone. Your financial plan is a living document.

Unlike the old days, when plans were reviewed only every three to five years, today’s technology allows advisors to make frequent updates and model different scenarios, like changes in spending, market environments, and tax rules. Your financial advisor will also help you edit your plan whenever there is a big shift in your financial situation, whether that means an unexpected gain, the selling of a business, or the loss of a family member.

You can also replan and recalculate when you feel your risk tolerance changing. For instance, if the market takes off, you can probably have a less risky portfolio and still achieve your life goals. Or you can choose to keep the pedal to the metal and leave a bigger legacy behind.

Right on Target

Smith says, “Having a path to follow—that is, the recommendations determined from the plan—and your financial advisor as an accountability partner is the biggest value to having a holistic plan, rather than just setting a portfolio. The plan will provide peace of mind when the market dips and give you clarity on what impact short-term decisions will have on your long-term projections.” Also, “Having a sounding board to discuss your goals and fears before making a big decision helps to make sure you aren’t acting out of emotion,” she says.

For Ensign, the beauty of integrating investments with tax and with financial planning is that advisors can provide more accurate, personalized guidance. Ensign says, “We often find ourselves challenging the investment thesis, which says, ‘This is the right thing to do right now. Sell this and buy this.’ But we can look at a client’s unique situation and say, ‘OK, that might improve the performance report, but for this particular client, it would be absolutely disastrous.’” That’s why it is critical advisors have a variety of portfolio options to choose from.

“It feels almost magical when it all comes together and we can find these big wins for people,” says Ensign. “We do this one thing over here, shift this other thing over there, and suddenly 1+1=3. Those moments don’t come for every client, every month, or every year necessarily. But when they do, that’s a bull’s-eye.”