-

Solutions

- Solutions

-

Individuals & Families

- Individuals & Families

- Individual Investors

- Executives & Business Owners

- Families with Complex Needs

- Professional Athletes

-

Retirement Plan Sponsors

- Retirement Plan Sponsors

- Corporations

- Educational Institutions

- Healthcare Organizations

- Nonprofits

- Government Entities

- Endowment & Foundation Leaders

- See All Solutions

Comprehensive wealth planning and investment advice, tailored to your unique needs and goals.Investment advisory and co-fiduciary services that help you deliver more effective total retirement solutions.CAPTRUST provides investment, fiduciary, and risk management services for nonprofit organizations. -

About Us

- About Us

- Our People

- Our Story

- Learn About CAPTRUST

-

Locations

-

Resources

- Resources

- Articles

- Podcasts

- Videos

- Webinars

- See All Resources

Here are some of the key takeaways of the proposed regulation.

Any special rules associated with LTPT employees apply only if an employee is participating in the plan solely because of the LTPT rules.

LTPT employees are covered by the following special rules:

- They may be disregarded for purposes of complying with annual deferral percentage (ADP) or annual contribution percentage (ACP) nondiscrimination testing.

- They are not required to receive any minimum top-heavy contributions.

- They may be disregarded for purposes of coverage testing. However, they must be credited with a year of vesting service for the period with which they are credited at least 500 service hours.

An employee who is participating in the plan for any other reason is not an LTPT employee under the rules.

LTPT employees must be made eligible to make elective deferrals only. Employer contributions are not required, not even if they are safe harbor contributions. Top-heavy exemption would be lost if the plan currently uses more liberal requirements to make elective deferrals to the plan than what is required under the LTPT rules (e.g., immediate eligibility or elapsed-time method), yet does not require safe harbor employer contributions for such employees.

401(k) plan sponsors that provide a safe harbor contribution will need to evaluate their safe harbor notice to ensure it is consistent with the new LTPT rules and is provided to any newly eligible employees by January 1, 2024, for calendar-year plans.

401(k) plan sponsors will still be able to exclude job classifications from the right to make elective deferrals so long as the classification would not have the effect of imposing another age- or service-related requirement. This is the same as current rules. Thus, plan sponsors could exclude employees who work in a certain division but could not exclude part-time employees who would otherwise satisfy statutory service requirements, including the new LTPT requirements.

All LTPT employees will earn vesting service using the 500-hour rule, even if they do not receive any employer contributions as an LTPT employee. Additionally, if an LTPT employee later earns 1,000 hours of service, or otherwise begins participating for reasons other than LTPT status, the employee must continue to earn years of vesting service under the 500-hour rule.

Plan sponsors that do not currently allow LTPT employees the option to defer to their 401(k) plans may wish to do so in the future to avoid the extensive hours-counting requirements under the SECURE Act and SECURE 2.0, as well as the administratively complex vesting requirement for anyone who is, or ever was, an LTPT employee. Sponsors should consider any potential impact to nondiscrimination and top-heavy testing, additional employer contributions, etc.

There is no mention of 403(b) plans in the proposed regulations. However, LTPT rules for 403(b) plans are not effective until January 2025, so the IRS still has some time to issue regulations in that regard.

The proposed regulations are complex. Plan sponsors should review their plan design and current processes to determine if any changes are necessary in plan operation or communication.

Plan sponsors who have questions about this or other SECURE 2.0 provisions should reach out to their financial advisor or visit CAPTRUST’s dedicated SECURE Act 2.0 web page. The IRS proposed regulation is available here.

Should you have immediate questions or want additional information, please contact your CAPTRUST financial advisor at 1.800.216.0645.

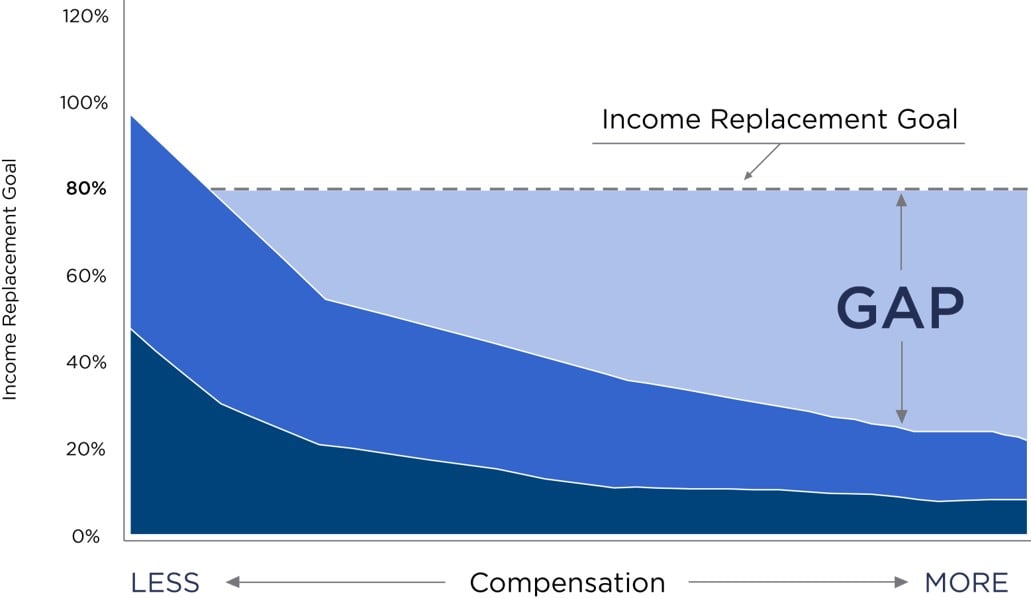

High earners relying solely on qualified plans and Social Security to generate retirement income will face savings shortfalls. And the higher an individual’s compensation, the more severe the potential retirement income gap can be.

Generally speaking, a highly compensated employee needs to save above and beyond the maximum 401(k) or 403(b) contribution limits—along with other options, including health savings accounts (HSAs) and individual retirement accounts (IRAs)—to maintain their current lifestyle when retired.

“Part of being highly compensated is the inherent challenge of saving enough to replace 70 to 80 percent of your working income in retirement,” says Scott Matheson, Managing Director of the Institutional Group at CAPTRUST. “High earners need to look for other ways of saving outside of traditional retirement plans. For these people, it’s much more complex than just maxing out your 401(k).”

According to a MarketWatch study, 51 percent of investors who have investable assets of $500,000 or more report feeling concerned about their financial security in retirement, and 46 percent are worried their portfolios are not properly tax optimized. Research from Urban Institute also reveals that one in 10 high-income families have no retirement savings at all. In fact, Neilsen reports, 25 percent of families making $150,000 a year or more are living paycheck to paycheck.

It’s counterintuitive, but what seems to be true is that a hefty income doesn’t necessarily lead to a successful retirement. The question is, what can high-earners do now, while they’re still working, to help make sure they have enough money to maintain their current lifestyle after retirement?

Don’t Go Belly-Up Keeping Up

First and foremost, live within your means. The trend of keeping up with the Joneses can affect high-income people just like anyone else. And living outside your means is a bad habit, no matter what yearly income you’re working with.

“People tend to have comparable margins for spending as a percentage of their compensation, but they don’t seem to have an expanding relative margin of saving,” says Matheson. “Which means when they make more money, they’re going to buy a bigger house. Make more money, maybe join the country club. Make more money, maybe buy a more expensive car and put the kids in private school, and so on.”

This trend can condition high-ranking employees to believe that a consumption-based lifestyle is expected or even necessary to take full advantage of their wealth. But showing the world that you’re making more money can come with a big cost.

“I’ve worked with families who are trying to keep up with other families who make double, triple, or more each year, and it’s a recipe for disaster, no matter how much you earn,” says CAPTRUST Financial Advisor Mike Molewski. “A high income can leave you more wiggle room, but it shouldn’t be used as an excuse to go out and buy yourself whatever you want.”

According to Molewski, people at every income level can have money problems, especially if they are trying to keep up with others who are in a higher earnings bracket. “It’s the same for high earners; they just have more at stake,” he says. “Failure to set a realistic budget and stick to it will hurt you regardless of your income.” This is one reason why it is so important for high earners to accurately assess all potential streams of income and maximize their savings opportunities.

Retirement Plan Jenga®—Stack ’Em Up!

The combination of qualified retirement plan benefits and Social Security retirement benefits fall quickly as income rises. In fact, according to CAPTRUST research, an individual earning more than $200,000 a year cannot maintain their standard of living in retirement by relying on Social Security benefits and qualified retirement plan savings opportunities alone. Unless high earners find a way to save the additional money necessary to approach a 70 to 80 percent income replacement rate, they are at risk of serious retirement savings shortfalls, as shown in Figure One.

Figure One: Retirement Income Gap

Source: CAPTRUST Research

To attain the recommended retirement income replacement rate, high earners can utilize a combination of other savings programs, such as HSAs, nonqualified deferred compensation plans, stock purchase or stock option plans, and personal after-tax savings.

Layering benefit plans is a great way to maximize retirement savings and put away more money on a tax-favored basis. For example, high-income employees looking for further tax-favored saving should consider using an HSA. Participants can contribute up to $4,150 to an HSA if they have individual health insurance coverage or up to $8,300 for family coverage in 2024. People ages 55 and older anytime can contribute an extra $1,000. And, if you still have an HSA balance after the age of 65, you can take withdrawals from the account for non-medical expenses, penalty free.

“I can’t stress it enough to my clients, how important healthcare costs are for a couple retiring today,” says Molewski. “Maxing out an HSA and having those funds earmarked for healthcare expenses is a big deal. It’s not something you want to pass up.”

Additionally, those who have maxed out their employer-sponsored retirement plan savings limits and HSA contributions but still want to save more for retirement could benefit from using their company’s nonqualified plan. This type of plan offers high earners pre-tax savings proportionate with their income.

“Nonqualified deferred compensation plans are often used by employers as an added executive benefit, because 401(k) plans are inadequate, by themselves, for high earners,” says Matheson. “A nonqualified plan is like an agreement between employee and employer to defer a portion of the employee’s annual income until a specific date in the future. Depending on the plan, that date could be in five years, 10 years, or in retirement.”

Stock awards and stock options provide an added layer of long-term savings for high earners that can complement a stack of retirement plans. Executives, successful sales professionals, and business owners often receive stock purchase or stock option plans that can be used to supplement existing retirement accounts.

“While many recipients of equity compensation intend to use it to boost their savings and lifestyles, they often do not see this compensation as part of the bigger picture of retirement savings and post-retirement withdrawal plans,” says Matheson. “People often need a reminder to view these assets as a way to build up their long-term retirement nest egg.”

Possibility of Disability

Of course, long-term financial planning is not only about saving. It’s also about managing risk.

One big risk to your ability to save is the possibility of experiencing disability. And the reality is that more than 25 percent of Americans will acquire a disability before reaching retirement age, with numbers shooting upwards exponentially after age 65. Once a person becomes disabled, the Council for Disability Awareness reports that the average long-term disability absence lasts 34.6 months—nearly three years.

“Key employees acknowledge that their income is important, but they frequently misjudge the value of insuring it as an important asset,” says Matheson. “Adequate income protection, like disability insurance and life insurance, can help ensure financial obligations are met in the event of a disability or death.”

Many employers offer short- and long-term disability insurance options as employee benefits. Most commonly, these plans provide 60 to 70 percent of gross income in the event of disability. Nevertheless, Molewski says, the coverage that employer-sponsored disability policies provide is generally not enough for high-income earners because their base salary and incentive payments often end up exceeding the maximum policy coverage.

“In many cases, we have seen companies identify a shortfall and develop supplemental disability and life insurance plans that can help solve for these problems. Often at a minimal cost to the employer,” says Molewski.

Between lost income and increased healthcare expenses, the financial strain a disability can cause can create serious retirement savings shortfalls. A supplemental disability insurance plan and life insurance plan can help mitigate the risk of income shortfalls due to disability or death.

Tools and Advice Unique to the C-Suite

Integrating corporate benefits, equity compensation, and retirement risk management requires time and expertise that many busy professionals do not have. In fact, a nationwide survey of 1,000 equity compensation plan participants by the National Association of Plan Advisors found that half of respondents felt confident in their ability to make the right decisions about their equity compensation plan on their own.

Setting objectives, developing a clear picture of financial assets, understanding risks and time horizon, and measuring progress toward goals are four key pieces of the wealth planning process. But employers are increasingly finding ways to initiate financial advice and education that cater to the complex planning needs of high earners.

For any company expecting executives or partners to retire at a certain time, it makes sense to consult with these key employees at least five or 10 years before that date to gauge how their retirement plans are going. Executives may learn that they’ve fallen behind on their goals and may benefit from help with financial planning. Some high earners don’t even realize how much they may have amassed.

“Often, even those who are earning significant salaries don’t know they can retire because they have limited knowledge of their consolidated wealth, and this isn’t surprisingly, since it might be in four or five different places,” says Molewski. “The tools and resources available to high earners are lacking when it comes to being comprehensive and properly accounting for all of their assets.”

“A comprehensive program that looks at all the different layers of compensation is critical for high earners because it consolidates an employee’s full financial profile,” says Nick DeCenso, CAPTRUST director of wealth management. “As a core of the offering, the services need to overlay advice on top of the employee’s entire existing pool of assets, regardless of where they are held or who may have recommended the specific investment.”

“What we see is that the vast majority of retirement plan services fall short of providing adequate advice for executive-level needs,” says DeCenso. “It’s important that the tools and advice address more complicated payment packages that can include benefits like bonuses, partnership distributions, retirement contributions, and restricted stock units. This type of customized financial advice for executives is fairly unique in the industry.”

One way to position executives favorably against the possibility of a retirement income gap is to have these individuals complete a retirement needs calculation that truly encompasses their full financial picture. This exercise will help high earners determine how much they have amassed in different accounts and what they need to save to meet their goals. Armed with this crucial information, they may be motivated to save more, take advantage of other company-sponsored savings programs, and more accurately calibrate their retirement expectations.

The bottom line for high earners is that big paychecks don’t necessarily translate into high savings rates. While a high income gives people a distinct advantage when it comes to building wealth, that advantage can only take them so far. Customized advice and planning, enhanced risk protection strategies, and optimization of benefit and savings opportunities can make a big difference when trying to bridge a potential retirement income gap.

For some, fall and winter are exciting times, filled with leaf-peeping, football games, holiday gatherings, and cozy evenings at home. But for others, these chillier, shorter days—and the seasonal loss of light—feel ominous. In more common and less disabling forms, people call this the winter blues. But in its most extreme form, this seasonal shift is known as seasonal affective disorder (SAD).

What is SAD?

SAD is a form of depression that occurs in a seasonal pattern, most often in fall and winter. The symptoms can include all the hallmarks of major depressive disorder, including sadness, hopelessness, fatigue, a loss of interest in life, and changes in eating or sleeping habits.

“People with SAD can suffer just as much as people with any other form of depression,” says Dr. Norman Rosenthal, a clinical professor of psychiatry at Georgetown University School of Medicine. Rosenthal led the team that first recognized SAD as a distinct mental health condition in the 1980s.

Rosenthal says people who experience SAD “can feel suicidal and lose their jobs and lose their relationships. It can be a big deal.”

But SAD is different from other forms of depression in some ways, says Dr. Kathryn Roecklein, an associate professor of psychology at the University of Pittsburgh. Roecklein has devoted her career to finding the biological, psychological, social, and environmental causes of SAD so that she can improve treatment. She says one thing that makes SAD unique is that it is predictable. “It happens year after year, at the same time,” she says.

Also, Roecklein says, people with SAD are less likely than other people with depression to die by suicide, possibly because “hopelessness is less of a problem. People know that spring will come.” She says the average bout of SAD lasts four to six months, while the average instance of major depressive disorder lasts more than a year.

Another difference is a distinctive change in eating habits. People with SAD tend to gain weight as they turn to food for comfort, Roecklein and Rosenthal say. They also report sleeping more, not less, when they are depressed, although Roecklein says her most recent study suggests oversleeping isn’t as typical as once thought.

If you are not clinically depressed but are less cheerful, energetic, creative, and productive in winter, Rosenthal says you may be among the 15 percent of U.S. adults who suffer from the winter blues. Researchers often use a more technical term—subsyndromal SAD—to describe this less severe condition.

What Causes These Problems?

When Rosenthal was growing up in South Africa, he says he noticed the difference in his moods between the warm summers and the cooler winters. But, as he writes in his book, Winter Blues: Everything You Need to Know to Beat Seasonal Affective Disorder, he did not really understand the way winter could deplete his spirits until he spent a year in New York City.

“I had not anticipated how short the days would be,” Rosenthal writes. “Then daylight savings time was over, and the clocks were put back an hour. I left work that first Monday after the time change and found the world in darkness. A cold wind blowing off the Hudson River filled me with foreboding. Winter came. My energy level declined.”

In the spring, he writes, his energy and mood surged again.

Later, Rosenthal and other scientists from the National Institutes of Health (NIH) started to put the pieces together. Certain patients, they noticed, suffered as the hours of daylight declined, with some starting to feel blue by late summer, and most declining by mid-autumn and struggling the most in the dead of winter.

Rosenthal and his colleagues theorized that a shortage of daylight threw some people out of whack, perhaps by disrupting key hormones and the body’s circadian rhythms, the internal clocks that help regulate alertness, mood, and appetite.

They tested this theory by treating some early patients with daily doses of bright light delivered from a huge two-by-four-foot box outfitted with fluorescent fixtures. The result: These patients felt better.

It would take years of research to solidify the theory, but today, seasonal loss of light is accepted as the primary trigger for winter SAD and the milder winter blues.

Is a Lack of Light the Only Cause?

SAD likely has several underlying causes that differ from person to person, Roecklein says.

In fact, many sufferers have retinas that are less sensitive to light. On dull winter days, their eyes might not process light in a way that keeps their circadian rhythms in sync. They feel sleepy and slow in the daytime because their brains haven’t gotten the message that it’s daytime at all.

Psychological factors also matter, Roecklein says. People with SAD, like others with depression, often report stressful or traumatic childhood events. “I want to interview people [who have had stressful or traumatic childhood events] and find out if the negative events happened in winter,” Roecklein says. “Maybe, each winter, the response is to hibernate—to turn inward.” Turning inward, she says, could lead to even less light exposure, less social contact, less exercise, and more pronounced symptoms.

Who is Most at Risk?

Research has found sharp differences in the risk for SAD by latitude, at least in the U.S. The farther north of the equator you live, the more likely you are to suffer, with rates ranging from about 1 percent in Florida to 10 percent in New Hampshire. Curiously, the same clear differences by latitude are not found in Europe, even in countries above the Arctic circle where people routinely experience whole months without daylight. Roecklein says this suggests that factors ranging from cloud cover to culture may be at work.

Women are more likely than men to be depressed, and this gender divide is especially wide when it comes to SAD. Women are four times more likely than men to experience SAD or the winter blues. And while you might suspect that older adults would be especially at risk because they spend more time homebound in the winter—particularly in cold climates—that’s not true. The risk is highest in early adulthood and middle age, Rosenthal says.

One other important risk factor is family history. Forty percent of SAD risk appears to be inherited, Roecklein says.

Can You Screen Yourself for SAD?

In Winter Blues, Rosenthal includes a questionnaire he helped develop called the seasonal pattern assessment questionnaire, or SPAQ. It can be found online and is one of several screening tools researchers use to determine who might have SAD or the winter blues. While Rosenthal says using this questionnaire to screen yourself can be useful, both he and Roecklein say that anyone who believes they are depressed should seek medical help.

What is the Treatment?

Light therapy remains a mainstay in SAD treatment. Today’s light boxes are much smaller than the 1980s prototypes and provide 10,000 lux of light, with harmful ultraviolet rays filtered out. Light use is typically recommended for at least 20 to 30 minutes a day, usually in the morning.

Antidepressant medications and a form of talk therapy called cognitive behavioral therapy also show effectiveness in studies.

Daily habits matter too. Rosenthal says he starts winter days with a stationary bike ride in front of a light box. He says everyone vulnerable to winter sadness should try to exercise, eat healthfully, get outside, and keep up social ties. “You’ve got a choice whether you are going to keep your head under the covers or get up and face the day,” Rosenthal says.

Brightly lit homes and offices and an occasional sun-soaked vacation can help, too, Rosenthal says. Lastly, it’s important to remember: Spring will always come again.

The last few years have been defined by unpredictability, and pension plan sponsors have faced their fair share. Federal Reserve interest rate hikes, market volatility, and an aging population have combined to create a perfect storm of uncertainty and change for pension plan sponsors. This confluence of factors has elevated the importance of liability-driven investing (LDI) and proven its usefulness.

Consider the interest rate environment of the last decade. For years, central banks around the world kept interest rates at historic lows, which reduced returns on fixed income investments—often a staple in pension plan portfolios because of their stable cash flows and relatively low risks. As a result, many pension plan sponsors faced a growing gap between their plan liabilities and the returns generated by plan assets. But things reversed quickly when rate hikes began in 2022. As interest rates rose, pension plan sponsors saw liability values shift downward, providing a tailwind for funded status improvements.

Enter LDI: an investment strategy that seeks to align the duration and risk profile of pension assets with expected future liabilities to smooth the rough edges of financial volatility. LDI is now becoming more of a focus for plan sponsors as they look for ways to lock in funded status. Funded status is the financial status of a pension plan, measured by subtracting liabilities from assets. If a plan’s funded status falls below a certain level, the sponsor may be required to make additional plan contributions to bring the funding level back above the threshold. LDI helps protect funded status by creating more alignment between liabilities and assets.

But making good use of LDI requires a shift in thinking, says Curtis Cunningham, an institutional portfolio manager at CAPTRUST. “It means transitioning away from an asset-only view of pension performance to a more holistic view that considers performance relative to liabilities,” says Cunningham. “LDI isn’t about maximizing returns. It’s about mitigating risk. And managing risk is the best way to make sure you don’t underperform your liabilities.”

LDI Benefits and Challenges

Nroop Bhavsar, a senior specialist in institutional portfolio management at CAPTRUST, says LDI offers three primary benefits: risk management, enhanced predictability, and improved funding discipline.

“When actively managed, LDI can significantly reduce interest rate risk and help moderate market volatility,” says Bhavsar. By aligning assets with liabilities, it ensures a more predictable funding outcome, helping plan sponsors avoid the wild swings that can lead to underfunding crises.

LDI can also help provide stable cash flows, making it easier for plan sponsors to meet pension obligations. This predictability can be hugely beneficial, especially when facing unpredictable market conditions.

Lastly, the structured approach of LDI promotes responsible funding practices. Combining responsible funding patterns with LDI helps solidify funding gains associated with those contributions. Encouraging plan sponsors to increase their allocations to fixed income instruments can effectively secure their funded status, ensuring the financial well-being of retirees and bolstering long-term financial stability.

But LDI also poses potential challenges, the most significant of which may be the ability to actively manage the LDI portfolio vs. the plan’s liabilities to avoid underperformance, downgrades, and defaults. This is one reason an active LDI manager may outperform a passive manager, as this article will discuss later.

Considerations for Implementation

Plan sponsors considering LDI should approach implementation holistically, carefully assessing their specific needs and objectives. Every pension plan is unique, with distinct cash-flow characteristics and liabilities based on its participant makeup. LDI can create a portfolio that structurally matches the key rate durations of the plan’s liabilities. This is called duration matching. A core principle of LDI, duration matching means aligning the interest rate risks of pension assets with those of the pension liabilities.

Most commonly, sponsors will assign a percentage of plan assets to LDI. Funded status shapes the intent and composition of the LDI portfolio. As funded status improves, so does risk mitigation. “The higher your funded status, the higher percentage of assets you can allocate to LDI because you want to protect that status by being more conservative,” says Cunningham. “But a lower funded status often means you may need to take more risk. In that case, you’ll typically have a lower allocation to LDI and a higher allocation to return-seeking assets.”

Hard frozen pension plans are usually the best candidates for LDI, since these plans are no longer accruing liabilities. Hard frozen means the plan is closed to new participants and existing participants are no longer accruing benefits. Soft frozen plans may also be eligible, depending on funding status. In soft frozen plans, existing participants are still accruing benefits, so the plan is still accruing liabilities.

But LDI isn’t only fit for frozen pension plans. “It can be appropriate for lots of different plan types—even open plans that are still accruing benefits if the sponsor is looking to mitigate risk and create more predictable outcomes,” says Cunningham.

The Impact of Interest Rates

Although hard frozen plans may be easiest to track and predict, all pension plans face uncertainty because interest rates impact liabilities. Duration of assets and liabilities, allocation to LDI, and funded levels can all serve to make liabilities more rate sensitive than assets.

“Changes in the rate environment can have a meaningful impact on liability valuations and cause discount rate and duration to change over a plan’s life,” says Bhavsar. Simple hedging solutions, like blending mutual funds to match duration, may be appropriate under certain circumstances, but for many sponsors, they can be difficult to manage.

LDI strategies help to soften the volatility created by interest rate movement. “They do this by matching cash flows along the yield curve to mitigate interest rate risk each year,” says Bhavsar. “Liabilities are interest-rate sensitive, but investments are only interest-rate sensitive up to the amount of LDI that you have in your portfolio.”

The intention is to create an investment strategy that is more aligned with the interest rate sensitivity of liabilities. This way, even in times when fixed income performance is challenged, funded status will remain stable relative to liabilities.

Stability protects participants’ benefits and helps make Pension Benefit Guaranty Corporation (PBGC) premiums more predictable. In 2023 and for 2024, PBGC variable-rate premiums are set at $52 per $1,000 of unfunded vested benefits—a 478 percent increase since 2013. “There is a significant cost to being underfunded,” says Cunningham. “And that cost will likely continue to increase in the next few years.”

Active vs. Passive LDI

Navigating changing rate environments and their impacts on liabilities may present challenges when not using an active LDI manager. Given the constant change in plan duration and plan discount rates, utilizing an off-the-shelf fixed income solution limits the precision with which a fixed income portfolio can hedge liabilities across a range of interest rate environments.

Active LDI investment managers focus on plan-specific risk factors like key rate duration to maintain a high degree of correlation between plan assets and liability valuations, which helps preserve funding levels. Key rate duration measures how the value of an asset changes at a specific maturity point along the entirety of the yield curve.

“Unlike a fixed income portfolio of similar quality, plan liabilities are immune to the effects of credit downgrades,” says Cunningham. “In an LDI context, this necessitates active investment in the portfolio to avoid downgrades and keep pace with plan liabilities.”

Utilizing active LDI management can protect the portfolio against unnecessary risk. Since trading activity can be based on research, not only index changes, there is an opportunity for performance to outpace the index and for managers to take advantage of market inefficiencies. “Active managers are often able to select bonds from a much wider opportunity set than a passive index,” says Cunningham. “By doing so, they can potentially avoid the impact of downgrades and defaults.”

A downgrade is when a ratings agency lowers the credit rating of a borrower. Actuaries for corporate pension plans calculate discount rates for pension liabilities using high-quality corporate bond yields to determine how much is needed today to fund future benefit payments. These rates are created by screening the universe of corporate bonds based on criteria such as credit quality. Investment managers use the same universe of bonds as part of the opportunity set when investing in LDI portfolios. When one of the bonds included in an LDI portfolio is downgraded below an acceptable credit quality or defaults, it no longer passes the screen and is removed from the discount-rate calculation in the next period.

With an active manager, removal can happen immediately, or even preemptively. “Active managers have the expertise to identify struggling companies and their probabilities of default,” says Bhavsar. “With a passive manager, removal happens only when the index is reconstituted.”

Yet passive strategies can be lower cost and more tax efficient, making them an attractive option for some defined benefit plan sponsors. “The important piece is to do your research so you’re really comparing apples to apples,” says Cunningham. “Passive strategies can sometimes help sponsors save money on fees but at the expense of outperforming the plan liabilities. You can get some custom LDI managers at a relatively attractive cost that will likely save you money in the long run. But if you’re looking at only fees—not the overall opportunity cost—passive strategies will almost always be less expensive.”

Risk Budgeting

In an era defined by unpredictability, LDI is one answer to the question of how to manage pension plan risks. As the complexities of the financial world continue to evolve, so must the strategies employed by defined benefit retirement plan sponsors. It’s not just a matter of financial prudence; it’s a way for pension plan sponsors to navigate the rough seas of uncertainty, reduce risks, and secure the financial future of retirees.

Before constructing an LDI portfolio, plan sponsors should do three things. First, identify the desired liability that they would like to hedge (e.g., the ASC 715 projected benefit obligation). Then, quantify the acceptable funded status risk given the plan status, current funded status, market conditions, and risk tolerance. And lastly, recognize the limitations inherent in hedging pension liabilities. With these pieces of data in hand, sponsors can make more robust decisions about LDI implementation and future measures of success.

DOL Challenges $1.3 Million Reimbursement of Plan Sponsor Expenses: Inadequate Records and Process

The Department of Labor (DOL) has challenged a plan sponsor’s receipt of $1.3 million from its three retirement plans as reimbursement for staff time spent on plan administration. According to the complaint, the plan sponsor and fiduciaries did not track the services provided to each of the three plans. Rather, the amount of staff time spent was determined by asking employees at the end of the year to estimate how much time they had spent working on the plans. An hourly rate was applied, and the total amount was assessed from the plans pro rata based on their respective assets. No steps were taken to ensure the reasonableness of the amounts reimbursed.

The DOL alleged the fiduciaries breached their duties by “instituting and maintaining a faulty process rather than doing their jobs as fiduciaries to protect participants’ and beneficiaries’ interests.” A motion to dismiss the complaint was recently denied, so the case will proceed. Su v. CSX Transportation, Inc. (M.D. Fla. 10.11.2023).

This case is a reminder to fiduciaries to be careful when paying expenses from plan assets, particularly the reimbursement of staff expenses. When asking permission to charge staff expenses to a plan, the DOL usually directs that detailed records be kept, and it challenges reimbursing the services of an employee who does not spend at least 50 percent of their time on plan matters. The assumption here is that if the employee spent more than half of their time on non-plan matters, the sponsor would have hired them—and incurred the corresponding expense—regardless of whether the plan existed.

We Can Use Forfeitures to Offset Future Employer Contributions, Right?

Participants who leave employment before meeting a plan’s vesting requirements forfeit the non-vested portions of their accounts. It is common practice for plan sponsors to use these forfeitures to offset employer matching or other contributions in 401(k) plans. Four nearly identical lawsuits have been filed alleging that it is a fiduciary breach to use forfeitures in this way, under the applicable plans’ terms. The same law firm has sued Clorox, Intuit, Qualcomm, and Thermo Fisher Scientific.

In the case against Intuit, as an example, the complaint acknowledges that the plan document allows forfeitures to be used either to pay plan expenses or to offset future employer-matching contributions. As a result, plan fiduciaries have discretion over how to use forfeitures. The argument is that the plan fiduciaries chose to use forfeitures to offset future matching contributions, thereby benefiting the plan sponsor, rather than using them for the payment of plan expenses, which would have benefited participants. This approach allegedly violates the ERISA exclusive benefit rule that says plan fiduciaries must always act in the best interests of plan participants and beneficiaries. Rodriguez v. Intuit Inc. (N.D. Cal. Filed 10.2.2023).

The use of forfeitures to offset employer contributions is a longstanding and widely accepted practice, permitted under IRS regulations and consistent with guidance from the DOL. Legal commentators have expressed skepticism about the legitimacy of this novel argument. It will be interesting to see if these cases survive motions to dismiss. In the meantime, plan fiduciaries should confirm that they are following their plan documents, and they should track finalization of the IRS’s proposed regulation on forfeitures, which is scheduled to go into effect on January 1, 2024.

Flow of 401(k) and 403(b) Fee Cases Continues

The flow of cases alleging fiduciary breaches through the overpayment of fees and the retention of underperforming investments in 401(k) and 403(b) plans continues. Here are a few updates from the last quarter:

- Approximately 10 cases were settled, with settlement amounts ranging from $61 million (GE) to $975,000 (Estée Lauder).

- Approximately 15 cases had motions to dismiss decided, with about one third being dismissed and two thirds proceeding.

- One case went to trial before a judge, with the plan fiduciaries prevailing. Plan participants sued fiduciaries of the B. Braun Medical Inc. Savings Plan, which has approximately $800 million in assets, alleging that the plan fiduciaries failed to investigate and select lower-cost alternatives to the plan’s investments and failed to monitor or control the plan’s recordkeeping expenses. After a three-day trial, the judge found that the plan committee had:

- Appropriately selected and monitored investment options.

- Met regularly, including annually for some of the applicable time period, and quarterly thereafter.

- Engaged financial advisors who presented reports on the performance of investment options.

- Had an investment policy statement.

- Used a watchlist and removed underperforming funds.

- Monitored whether to move into lower-cost share classes.

- Monitored recordkeeping fees using benchmarking and requests for proposals (RFPs).

- Negotiated lower recordkeeping fees.

- Changed recordkeepers during the applicable period after issuing an RFP.

- Kept regular minutes documenting the actions above.

The judge took into account industry trends and standards with respect to plan fees and noted that the committee had acted in line with industry practice. Based on all of this, the judge found the committee’s conduct regarding plan investments and recordkeeping fees was objectively prudent, and the investments used and recordkeeping fees paid were objectively prudent. Nunez v. B. Braun Medical, Inc. (E.D. Pa. 2023).

This case is a reminder of some key elements of a good fiduciary committee governance process and their importance.

- In one dismissed case, the judge rejected the claim that plan fiduciaries are required to use the least expensive share class of plan investments—net of any revenue sharing allocated to plan participants. The court said, “While a prudent fiduciary might consider the net expense ratio, no court has said that ERISA requires a fiduciary to choose investment options on this basis.” England v. Denso International America, Inc. (E.D. Mich. 2023).

DOL Tries Again to Expand Fiduciary Responsibility—Plan Distributions Targeted

On October 31, the DOL issued a proposed rule expanding ERISA’s fiduciary protections to more retirement investors. The current fiduciary rules apply to participants and assets in plans like 401(k)s, 403(b)s, and pensions that are covered by ERISA. However, financial services providers are not subject to these rules in the context of retirement plan distributions. The DOL is concerned that they may act in their own financial interests rather than those of their clients. The new proposed rule would extend ERISA’s fiduciary coverage to situations in which:

- Investment advice or recommendation is made to a retirement investor,

- The advice or recommendation is provided for a fee or other compensation, and

- The advice or recommendation is made in the context of a professional relationship, and the investor would reasonably expect to receive sound advice in which:

- The provider has discretion,

- The provider regularly provides individualized advice based on investors’ particular needs, or

- The provider states that it is acting as a fiduciary.

The proposed rule specifically nullifies written disclaimers of fiduciary status that conflict with what an investor is told.

It is clear from the DOL’s guidance and announcements that the target of this is advice and sales efforts in the context of retirement plan distributions. There is a 60-day comment period for the proposed rule. The DOL’s last effort in this area was overturned by the U.S. Court of Appeals in 2018. A spirited debate on the new rule can be anticipated.

Rare Employee Win in ERISA Retaliation and Benefits Interference Claim

Thomas Kairys was hired by a small trucking company, and soon after diagnosed with degenerative arthritis. He had to have hip replacement surgery, and a second hip replacement was expected. Medical costs for the first hip replacement were paid through the trucking company’s health plan. However, the health plan was self-insured, so the costs passed through to the employer. When Kairys returned to work after his surgery, his supervisor advised him to “lay low” because the company owner was unhappy with the additional medical costs. In the weeks following, Kairys was seen as a high-performing employee and earned a bonus for good work. Even so, four months after the first surgery, he was fired, allegedly because his work was no longer needed. Soon after, another person was hired to replace him.

ERISA prohibits a plan sponsor from firing an employee in retaliation for using their employee benefits or to prevent them from using those benefits. Kairys sued, alleging that he was fired because he had used his health benefits and was likely to continue using them. Following a trial, the district court judge found that Kairys was fired because of his past and anticipated future use of health benefits. The former employer was ordered to pay attorney’s fees and front pay of $180,000. The decision was upheld on appeal. Kairys v. Southern Pines Trucking Inc. (3rd Cir. 2023).

Securities and Exchange Commission: Neutralize AI Bias in Favor of Broker-Dealers and Advisory Firms

The Securities and Exchange Commission (SEC) has issued a broad proposed rule that is intended to prevent broker-dealers and investment advisers from using predictive data analytics and similar technologies, including artificial intelligence (AI), to place the firms’ interests above those of their investors. The concern is that a firm could use these technologies to advance the firm’s revenue or otherwise change investor behavior to benefit the firm at the detriment of the investor.

The proposed rule would require a firm to “eliminate or neutralize” situations in which technology optimizes the firm’s interests over those of the investor. It would not regulate investment advice provided to ERISA plans but would apply to advice provided to plan participants, including recommendations about investments and distributions—when assets are leaving an employer-sponsored retirement plan.

This rule has been openly criticized, with industry groups calling for its withdrawal. However, withdrawal seems unlikely. On October 30, President Biden issued an Executive Order calling on federal agencies to address AI issues and potential misuse. A White House release says, “The Executive Order establishes new standards for AI safety and security, protects Americans’ privacy, advances equity and civil rights, stands up for consumers and workers, promotes innovation and competition, advances American leadership around the world, and more.” If not already the case, it seems likely that the DOL will soon weigh in on AI issues.

Although Congress has been considering AI regulation, action on that front is not expected in the near term.

DOL Approves Diverse Investment Manager Support by Plan Sponsors

Citigroup (Citi) sought and received DOL approval for its racial equity program to support diverse-owned investment managers. As part of this program, Citi identified diverse investment managers as firms with at least 50 percent minority or female ownership. To support diverse managers, Citi will pay directly—in its capacity as the plan sponsor—some or all of the investment managers’ fees on investments used in Citi’s retirement plans.

Citi will not be acting as a fiduciary in the selection of firms to participate in this program or in the payment of fees; these would be settlor functions. However, not having investment management fees deducted from investment returns can be factored into the Citi investment committee’s fiduciary investment review and selection process.

The DOL cautioned that investment decisions should not be made based solely on an investment manager’s participation in the program or to further Citi’s public policy goals. This DOL letter serves to emphasize the difference between settlor and fiduciary functions. And it is a reminder to plan sponsors to only consider relevant financial factors in their manager selection and monitoring processes. DOL Adv. Op 1023-01A (9.29.2023).

DOL Wins Challenge to Most Recent ESG Rule

In 2022, the DOL finalized the Prudence and Loyalty in Selecting Plan Investments and Exercising Shareholder Rights rule, neutralizing the prior rule’s restrictions on consideration of ESG factors by plan fiduciaries in the selection of retirement plan investments. Twenty-six states and other parties sued to have the DOL’s new ESG rule thrown out. The court refused to set aside the DOL’s new rule. It noted that ESG factors could be considered even under prior rules if they are expected to have a material effect on the risk and/or return of an investment. The judge noted that some scholars have observed that changes from the prior rule are merely cosmetic. Indeed, the ERISA provisions these rules are based on have not changed since their 1974 passage. State of Utah v. Walsh (N.D. Tex. 2023).

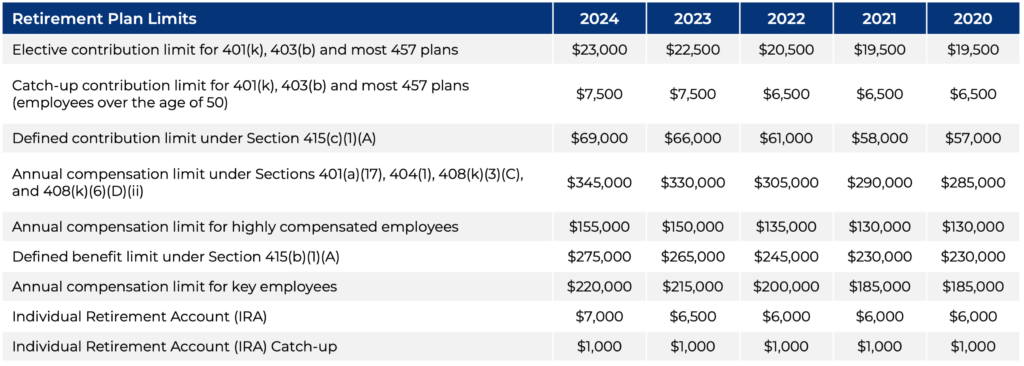

The Internal Revenue Service (IRS) has released its annual cost-of-living adjustments for retirement plan contribution limits for the 2024 tax year. These updates impact individuals contributing to 401(k), 403(b), IRA, and other qualified retirement plans, as well as employers managing benefit programs.

Staying informed about these limits is essential for maximizing contributions, planning for tax efficiency, and aligning your retirement savings strategy with your financial goals. Whether you’re an individual investor or an employer sponsor, understanding how these changes apply to you is key to making the most of your retirement planning opportunities.

The table below outlines a few key highlights for 2024:

Have Questions About Your Retirement Strategy?

Contact your CAPTRUST advisor at 800.216.0645 or visit your nearest CAPTRUST location to learn how to optimize your retirement savings for 2024 and beyond.

For example, consider the gymnastics events. Long before sprinting toward the springboard in the vault competition, each gymnast has calculated the necessary number of twists and turns required to earn a medal. But success is not decided solely by the complexity of their routine. It also depends on whether they can stick the landing. The same is true in an economic context.

Over the past few years, we have witnessed a dizzying array of economic twists and turns, from pandemic-driven volatility to an inflation surge and aggressive interest rate hikes by the Federal Reserve. Now, investors are watching to see whether the Fed can stick the landing and control inflation while avoiding a recession.

Will policymakers be able to achieve an economic soft landing, or will they create conditions for a rough landing that pushes the economy into recession? Or could we experience something in between: a bumpy landing with an extra step that costs us a few points but doesn’t do much damage?

As the Fed carefully watches the economic data, there are some signs that suggest the rate-hiking cycle could soon end. But others could signal there is more work to be done. The stock and bond markets seem similarly confused; equities have shown continued resilience this year, while bonds have undergone a painful recalibration.

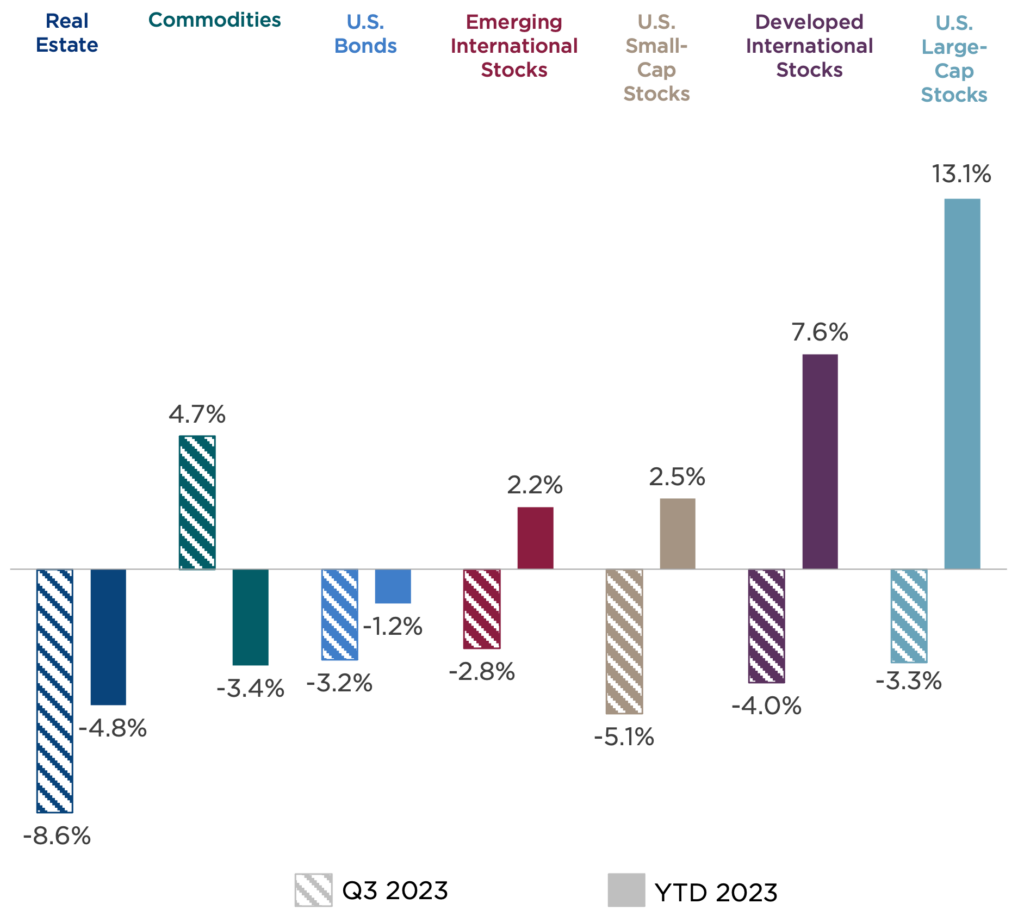

Third-Quarter Recap: Losses for Stocks and Bonds

After a strong first half of the year, U.S. stocks fell in the third quarter, particularly in September when the S&P 500 Index dropped nearly 5 percent. Although this ended a three-quarter streak of consecutive gains for large-cap U.S. stocks, as shown in Figure One, U.S. large- and small-cap equities remain positive for the year.

Growth and value stocks moved in tandem, although growth still leads the year by a generous spread. Interest-rate-sensitive sectors such as real estate and utilities lagged for the quarter, each with losses near 10 percent. Energy was the best-performing sector by a wide margin as the price of oil climbed by more than 20 percent during the quarter. This pushed commodities into positive territory as the only major asset class to end the quarter with a gain.

Figure One: Third Quarter and Year-to-Date Returns

Outside the U.S., both developed and emerging market stocks slumped, due in part to a U.S. dollar that strengthened for 11 consecutive weeks. European shares were weighed down by concerns about the impacts of rising interest rates as the European Central Bank raised policy rates twice during the quarter.

The third quarter was particularly difficult for bond investors. The total return from U.S. core bonds was -3.2 percent, as the 10-year Treasury yield advanced by more than three quarters of a percent to the highest levels in more than 15 years. These losses pulled year-to-date returns for core bonds into negative territory, at -1.2 percent. The Fed’s higher-for-longer interest rate message finally seems to be sinking in with investors.

The Economy Surpasses Expectations

2023 began with widespread anticipation of a recession, yet the U.S. economy has held up far better than expected and continues to grow. Now, easing inflation pressures and signs of a loosening labor market are fueling optimism that the economy could attain the elusive soft landing.

Several factors have helped the U.S. avoid the economic slowdowns witnessed across Europe and China. This includes inflation that has fallen to more manageable levels and a jobs market that, although tight and challenging for employers, offers consumers the ability and confidence to spend. Also, the housing market, an important driver of household wealth, appears to have stabilized despite limited supply and high mortgage rates.

Can Consumers Go the Distance?

The key question heading into this year was how long American consumers could continue as the driving force behind the economy. Even with dwindling savings and rising interest rates, consumers have almost single-handedly kept the economy out of recession.

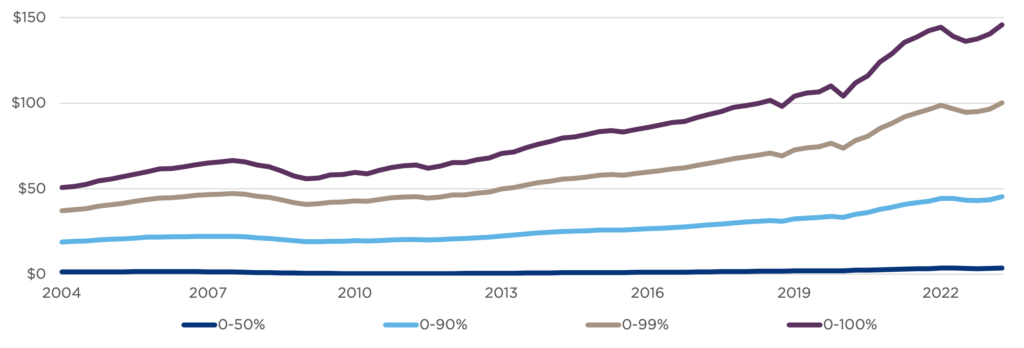

Personal consumption increased by more than 5 percent this quarter compared to a year ago, while retail sales continued to surpass expectations. And, as shown in Figure Two, although the excess savings people accumulated during the pandemic has been largely depleted, household net worth has bounded upward, increasing by a staggering $42 trillion since the first quarter of 2020, to a record-high level of $146 trillion.

Figure Two: Household Net Worthby Wealth Percentile Groups ($T)

Sources: Board of Governors of the Federal Reserve System, Distributional Financial Accounts

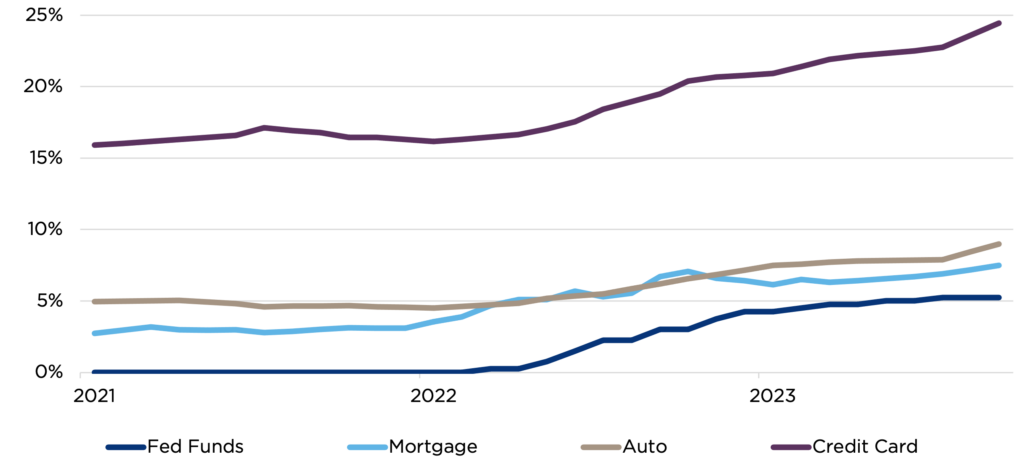

But even as U.S. consumers carry the economy on their shoulders, they face several significant headwinds moving into 2024. One important headwind is dramatically higher interest rates. As shown in Figure Three, consumer borrowing costs have risen across several important categories, including credit cards, auto loans, and mortgages. Rising debt balances and interest costs harm consumer spending because consumers must divert money away from current spending to pay interest and repay debt.

Figure Three: Soaring Consumer Borrowing Costs

Sources: St. Louis Federal Reserve, Board of Governors of the Federal Reserve System, Freddie Mac, Bankrate, LendingTree, CAPTRUST Research

Other headwinds include the resumption of student loan payments, with the net effect of an $8 billion per month drain on consumers’ spending capacity. Likewise, gas prices have risen by $0.63 per gallon since year-end 2022—the equivalent of an $86 billion tax on the U.S. economy.[1]

Finally, both consumers and businesses are facing tighter lending standards as banks respond to tough business conditions. However, although loan delinquencies have risen, they remain in line with the pre-pandemic trend, largely because of the amount of outstanding debt that is set at a fixed rate.

Given these challenges, it’s no surprise that measures of consumer confidence declined further in September. A slowdown in consumer activity seems likely from here.

Mixed Signals from the Labor Market

Another source of economic resiliency this year is the continued strength of the U.S. labor market. The September payroll report exceeded estimates as employers added 336,000 jobs in September—the highest reading since January. This report also revised July and August numbers upward by nearly 120,000 jobs.

Wages increased at a rate of 4.2 percent on a year-over-year basis, as the unusually tight labor market has increased the bargaining power of workers. This is also evidenced by ongoing labor strikes across various sectors, including the entertainment industry, health care, and manufacturing.

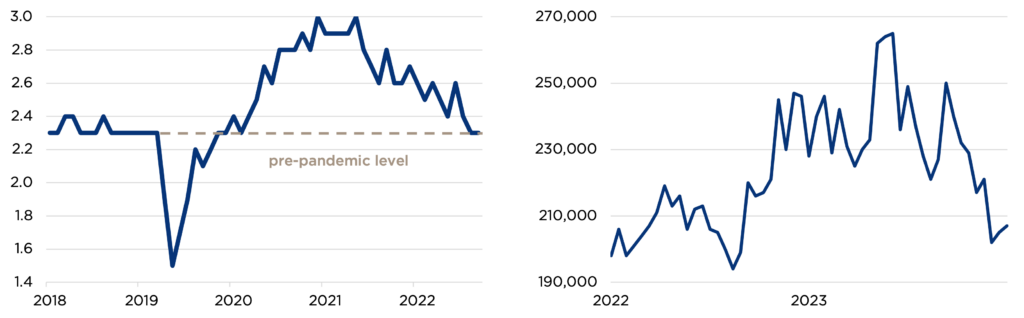

Many signs point to a still-red-hot labor market. As shown in Figure Four, after briefly topping a level of 250,000 in mid-summer, initial jobless claims data has trended steadily downward, indicating employers’ reluctance to let go of workers. However, there are also signs that the labor market is beginning to normalize. The quits rate, one measure of worker confidence in the labor market, has cooled considerably since the post-pandemic resignation boom. These mixed signals are difficult for economists to interpret.

Figure Four: Labor Market Mixed Signals: Quits Rate vs. Initial Claims

Sources: U.S. Bureau of Labor Statistics, U.S. Employment and Training Administration

Fed Policy Apparatus

The Fed left its policy rate unchanged in June and again in September, signaling optimism that it may be approaching the end of its rate-hiking campaign. However, following the last Fed meeting, Fed Chair Jerome Powell hinted that another rate hike could be in the cards for 2023, along with a somewhat cryptic statement that one can know when monetary policy is sufficiently restrictive, in his words, “only when you see it. It’s not something you can arrive at with confidence in a model or in various estimates.”

In other words, there remains significant uncertainty about the future path of Fed policy.

There is also uncertainty about the path that potential future rate cuts could take. If inflation remains elevated above the target while the economy stays strong, then interest rates could stay high for some time. But if inflation recedes to more comfortable levels, the Fed could begin mild rate cuts as soon as next year. Or, if the economy stumbles into recession, the Fed may be forced to cut rates more rapidly.

The Bond Market Dismount

Although the economy has not been knocked off course by the Fed’s actions, the bond market has been. The Fed’s higher-for-longer mantra has caught the attention of bond investors, sending yields up and prices down.

Core bonds are now flirting with their third consecutive year of negative total returns, even though fixed-income markets are offering their highest yields in more than 15 years. In this environment, only bonds at the short end of the maturity spectrum showed gains.

The tumbling bond market was somewhat surprising, given the widespread view that both the global and U.S. economies were moving toward recession. Slowing growth should be supportive of bond prices as investors seek safe haven investments, alongside an expectation for lower inflation and central bank rate cuts. One theory is that bonds were slow to react to rising rates because of recession expectations. Another possible explanation is the growing U.S. deficit and the growing burden of government debt servicing costs.

Earnings Face Hurdles

As the third-quarter earnings season kicks off in earnest, many investors are optimistic that S&P 500 earnings will land in positive territory after three consecutive quarters of decline. Early estimates are largely unchanged given the uncertain macroeconomic backdrop.

One area of focus this earnings season will be interest costs. Rising rates will have a growing impact as more companies must refinance maturing debt at significantly higher rates. However, if companies can deliver positive earnings growth, it could put stocks on a firmer footing for the fourth quarter following a year when stock price gains have far outpaced profit growth.

The Global Stage

Conditions outside the U.S. reflect a global economy that is losing steam. Thus far, Europe has narrowly avoided recession amid energy shortages and central bank tightening. In China, dimmed consumer confidence and a debt and property crisis have cast shadows over its economy, as well as other emerging market nations.

Finally, continuing conflict in Europe and the outbreak of war in the Middle East add new uncertainty to a fracturing global economy that poses risks to commodity prices, as well as to the decades-long globalization trend. Deglobalization would have significant implications for global growth and inflation conditions.

Trials Remain

As we enter the final quarter of 2023, major questions remain on the minds of investors. Can a stronger-for-longer economy coexist with higher-for-longer interest rates, or does continued strength today mean more pain later? Will corners of the stock market that have not seen gains in 2023 rally by year-end, or will recession pressures drag all sectors down?

As always, investors should assess both the risks and opportunities presented by the current market and economic conditions. A wide range of potential outcomes makes a strong case for portfolio diversification.

When we tune in to the Olympics for a welcome distraction next year, there will be a few new additions alongside our longtime favorite events. This includes breaking, also known as break dancing. The sport was, apparently, an outstanding success in the Buenos Aires Youth Games and features dancers who must improvise to changing music. Like these acrobatic athletes, investors must adapt to changing conditions as we hope that the economy can bend, but not break, under the pressures of higher rates and slowing growth.

[1] Fitch Ratings, Energy Information Administration, CAPTRUST Research

Today, perhaps more than ever, employers have the opportunity to enhance talent recruitment and increase employee retention by rethinking their retirement benefits to better align with their employees’ needs and expectations.

As Joanne Sammer writes for the Society for Human Resource Management, “At the most basic level, employee benefits are designed to provide workers with a sense that their employer supports them both in- and outside of the workplace.” Although it may be impossible to give every employee every benefit they want, employers can adjust existing benefit menus to show employees that they are listening.

“As an industry, we talk a lot about the shifting social contract between employers and employees,” says Jennifer Doss, defined contribution practice leader at CAPTRUST. Over time, the line between people’s personal and professional lives has thinned. Employees today want to be recognized as complex and complete individuals, not just workers.

To support them, employers should start with the basics, such as offering retirement plans. Research from Voya Financial shows that, among working Americans, 60 percent are more likely to stay with their current employer if they are offered an employer-sponsored retirement plan. Yet in 2021, only 52 percent of American employers offered a 401(k) or similar employee-funded retirement plan. And 41 percent did not offer any retirement benefits at all, according to data from Benefits Pro.

“Offering a retirement plan is the first step, but for companies that already sponsor a retirement plan, personalization and financial wellness are the next frontiers,” says Doss. “As the workplace contract continues to shift, employees are asking for financial wellness benefits beyond retirement savings.” And maybe just by coincidence or serendipity, they’re asking at a time when employers are starting to see improved capabilities for information-based solutions that can help them personalize their financial benefit packages.

Understanding Employee Needs

The path to a customized financial benefits program starts by understanding what employees want. Increasingly, employers are polling employees to learn which benefits are most attractive and which can be removed as population demographics and needs shift.

To balance employee and organizational desires, it can be helpful for employers to write an employee mission statement, describing the specific outcomes they want for people while they’re working at the organization. Most companies have an overarching mission but not one focused on the employee experience. “Knowing the goal will help you decide what to offer and explain why the organization provides each specific benefit or plan design feature,” says Chris Whitlow, CAPTRUST senior director of advice and wellness.

Although it’s a good idea to start by understanding which financial benefits employees want, the company may also choose to offer less-sought-after benefits that align with its employee mission statement.

As an example, consider health savings accounts (HSAs). These are tax-advantaged, member-owned accounts that allow participants enrolled in high-deductible health plans (HDHPs) to save pre-tax dollars for qualified healthcare expenses. HSAs are less popular with younger groups because younger individuals often have fewer medical needs and may not see the value in proactive saving for healthcare. Organizations with an HDHP option—and especially those with younger employee populations—might not see polling data that asks for an HSA but may still choose to offer one as part of their employee mission.

Personalized Investment Allocation

Another major area where employers are leveraging personalization to improve employee outcomes is investment allocation within retirement plans. Recordkeepers have more data now, shared by both the employee and the employer, and they can use that data to customize allocations for individual employees.

“In the past, we had just one data point—the person’s birthday. That’s what made target-date funds so impactful. That one data point felt like a very big deal,” says Doss. With a person’s birthday in hand, plan sponsors could figure out a participant’s estimated retirement date—assuming retirement at age 65—and could adjust allocations to optimize investment returns as the person aged.

“But now, with better data, we can customize further,” says Doss. Employers today can leverage information about each employee’s current retirement savings, salary, deferral rate, assets outside the retirement plan, financial goals, budget constraints, and more. “Atop this information, sponsors now have access to managed accounts, targeted education campaigns, and algorithm-driven recommendations for investment allocation, so they’re moving the needle that much more,” she says.

But personalized investment advice can only take an employee so far. The next piece is to personalize financial education campaigns to be sure the company is meeting every person where they are.

Targeted Education

Like investment allocation, until recently, financial education campaigns were generic by necessity. Mass personalization was simply not possible. Now, plan sponsors are leveraging technology to create customized campaigns at scale. “Technology can help you reach everybody by going beyond one-size-fits-all messaging, because you have the ability to gather more data on each person and draw smarter, less generic conclusions,” says Whitlow.

For instance, recordkeepers can scan employee data to identify all the people who are not saving at least enough to qualify for their company match. Those employees then receive a personalized email that tells them exactly how much money they’re leaving on the table and how much their company would give them if they saved more.

“In these targeted campaigns, the call-to-action is usually very specific, and it has the person’s name on it, so they’re already much more likely to open it and respond,” says Doss. Although targeted education services may not be available through all providers today, they are expected to trickle throughout the industry as converging technologies accelerate data collection and messaging capabilities.

Financial Wellness and Advice

Sponsors are also seeing increased capabilities for personalization of financial wellness programs. These are courses or educational materials that teach people how to manage money, invest, save, grow their assets, pay down debt, and more. Whitlow says technological advancements have improved financial wellness, “but at the end of the day, what I’ve learned throughout my career is that individuals want real, humanistic, empathetic advice and coaching.”

Doss agrees. “I don’t think anyone would argue that the best way to reach people—the best way to help people—is to meet with them one-on-one to understand their financial picture, their financial education level, and their financial goals, then give them the tools and knowledge to help them reach those goals,” says Doss. “But most people can’t afford a personal financial advisor. That’s why financial wellness is such an important and desirable employee benefit.”

By offering financial wellness services as part of benefit packages, companies ensure all employees have access to personalized, expert advice, not just those who can afford it on their own. And with so many data points at their fingertips, financial advisors can give better guidance faster.

Fortunately, financial wellness services are now more cost effective than ever before. Also, research shows that they are worth the investment. According to data from HR Professional and Ernst & Young, companies with financial wellness programs in place saw increases in employee retention (56 percent), employee well-being (50 percent), and employee productivity (46 percent).

“Financial wellness programs benefit participants, but they also benefit plan sponsors by improving participation, increasing contribution rates, and more generally, increasing engagement, satisfaction, and productivity at work,” says Whitlow. “Sponsors are already making thoughtful, future-focused plan design choices, but those mean little if employees don’t know how to put them to the best use.”

Now, plan sponsors don’t have to assume a general level of financial education for all employees. They can use recordkeeper data and internal surveys to deliver personalized education campaigns to all employee groups, from new workers to sandwich-generation caregivers to sophisticated investors in executive positions.

Driving Outcomes

Ultimately, Doss says, personalization benefits the individual participant, but it should also be driving better overall plan health and plan outcomes. “The big four measures of plan success are getting people in the plan, getting them to save enough, getting them invested, and then getting them to decumulate well,” she says. “If you’re leveraging personalization to do those four things, then you should be on the right track.”

Company culture also plays a part in this equation, says Whitlow, “by helping plan sponsors drive better outcomes for both employees and the organization, or detracting from their shared success.”

Many companies aim for a workplace culture that nurtures their most engaged employees: those who are both highly productive and an inspiration to their peers. Financial wellness programs, including benefits such as retirement plans, play a pivotal role in fostering this culture, he says. “Some employers grapple with the challenge of increasing employee participation in financial wellness programs. Yet it’s clear that success lies with employers who invest in understanding their workforce.”

By crafting personalized programs and clearly communicating the importance and value of these benefits—from the executive level down—employers often see significant improvements in engagement, productivity, and employee retention. These are cyclical forces. Company culture can drive participation, and participation can improve company culture.

What’s clear is that the personalization of benefit options and messaging makes a difference. Regardless of whether sponsors give participants a limited lineup of curated options or a robust, cafeteria-style menu, the most successful organizations will likely be those that have a clear picture of what employees want, and what the company wants for employees. By polling employees, writing an employee mission statement, and making use of recordkeeper data to personalize financial benefits, employers can put personalization to work for mutual benefit.

It’s OK to start small, but it’s important to get started. To keep employees engaged and on track financially, start by offering a retirement plan. Then work with a financial advisor to understand which plan features, financial wellness programs, and education campaigns will help them make the best use of it.

“From the day Jake was born, people said, ‘Don’t save anything in his name,’” Gehringer says. They told her if someone with a disability had more than $2,000 in cash or other resources, the person might not be able to qualify for certain government benefit programs, such as payments from the federal Supplemental Security Income (SSI) program and home and community-based services from the joint federal-state Medicaid program.

So, whenever Jake received cash, checks, or other such gifts—on his birthday, for example—the money typically was spent, not saved. Today, the picture is different.

Jake, now 27, is the owner of an Achieving a Better Life Experience (ABLE) account. It’s a special type of savings account intended to help individuals with disabilities pay for disability-related expenses—and it does impact the person’s ability to qualify for government benefit programs.

In 2014, Congress approved legislation creating ABLE accounts “to encourage and assist individuals and families in saving private funds for the purpose of supporting individuals with disabilities to maintain health, independence, and quality of life,” according to the bill.

The bill was also intended to “secure funding for disability-related expenses on behalf of designated beneficiaries with disabilities that will supplement, but not supplant, benefits provided through private insurance” as well as through Medicaid, SSI, the beneficiary’s employment, and other sources.

The federal law also allowed states to establish their own ABLE programs. The first, in Ohio, launched in 2016. As of September 2023, 46 states and the District of Columbia have ABLE account programs, says Miranda Kennedy, director of the ABLE National Resource Center, which was founded and is managed by the National Disability Institute in Washington, D.C., and serves as an independent clearinghouse for information on ABLE accounts. The exceptions are Idaho, North Dakota, South Dakota, and Wisconsin.

“Having a disability is expensive,” Kennedy says. An ABLE account “gives people with disabilities who need public benefits the chance to get out of a life of poverty, to be able to save and grow their money” without jeopardizing those benefits, she says.

Account Basics

An ABLE account can be opened online, usually for a minimum initial investment of $25 or less. Anyone can contribute, including family members, friends, and the account owner.

The person with the disability is the account owner and designated beneficiary, although a parent or other authorized person can have signature authority over an account established on someone’s behalf, such as a minor.

Investment options, which vary by state, are typically fairly conservative and often include not only mutual funds but also savings and checking accounts backed by the Federal Deposit Insurance Corporation (FDIC), says Stephen Dale, an attorney at The Dale Law Firm, PC, in Pacheco, California. Dale is a disability rights advocate. He works with families that have members with disabilities, focusing mainly on special needs trusts.

ABLE account contributions are not federally tax-deductible, but money invested in an ABLE account grows on a tax-deferred basis, Dale says. This means interest, dividends, and capital gains that are earned inside the account are shielded from federal income tax.

Withdrawals may also avoid tax consequences if they are used for the disabled person’s needs. The list of what counts for tax-free treatment includes expenses for education, housing, transportation, employment training and support, assistive technology, personal support services, health, prevention and wellness, financial management, administrative services, legal fees, expenses for oversight and monitoring, and funeral and burial expenses, according to Internal Revenue Service Publication 907, “Tax Highlights for Persons with Disabilities.”

Although some programs require the account owner to be a state resident, programs in a majority of states are open to residents and nonresidents alike, Kennedy says.

The ABLE National Resource Center website, www.ablenrc.org, includes a tool to compare all the available programs, summarizing features such as tax breaks for in-state residents, investment options, and debit cards or checking accounts for withdrawals.

Congress has made some changes to the law since its enactment. Under one of these changes, some funds now may be rolled into an ABLE account penalty-free from the designated beneficiary’s own 529 college-savings plan.

Limitations

ABLE accounts have limits. For example, you’re eligible to open one only if you have a significant disability (generally based on Social Security Administration rules) and if the disabling condition arose before you turned 26 (even if you’re now older than that).

If you clear those two hurdles and you’re already receiving benefits under SSI or Supplemental Security Disability Insurance (SSDI), you’re automatically eligible to open an account. If you’re not receiving either SSI or SSDI benefits but otherwise meet the guidelines, you can still open an account, but you’ll need to obtain a letter of certification from a licensed physician, Kennedy says.

A designated beneficiary can have only one ABLE account, and contributions from all sources are generally limited to $15,000 a year in the aggregate. This limit can increase annually with inflation. Also, an ABLE account owner who has a job typically can contribute an additional sum, within limits, from their work earnings.

There’s also an overall cap on the amount that an ABLE account can hold. For California’s program, for example, the cumulative balance limit is $529,000; for North Carolina’s, it’s $450,000, according to the ABLE National Resource Center’s state-by-state summary.

Although amounts in an ABLE account—and withdrawals that are used for qualified expenses—are typically disregarded for purposes of Medicaid or certain other government benefit programs, if the account balance exceeds $100,000, the person’s SSI benefit will be suspended until the account balance falls beneath that threshold.