At work one day, a co-worker told Hylen that he knew just the place to find a vintage car. He’d seen a house in the foothills of the Sierra Nevada mountain range with about 30 junk cars scattered throughout the property— including a 1969 Firebird. “This old guy has one parked under a tree that’s been there for 10 years,” Hylen recalls the co-worker saying. So he drove out to take a look.

First Sight

White with a blue vinyl top, the Firebird was in terrible condition, but that made no difference. Hylen loved it anyway. He knocked on the owner’s door and offered all his money for it. His offer was accepted.

With his dad’s help, Hylen hauled the Firebird home on a trailer and devoted hours of work to get it running, rebuilding the car’s motor and transmission. He drove it everywhere through his junior and senior years of high school. “Once, I hit a tree in our driveway and had to put a different fender on it,” he says. It was a black fender that someone had lying around, so the car developed a multicolored look.

After the accident, Hylen wanted badly to do a proper restoration of the Firebird, but he figured he’d never have the $30,000 or $40,000 it would cost to do things right. Plus, after graduation, he was leaving town to join the Marines. So he bid a sad goodbye and sold his beloved car.

Love and Loss

Cars, especially vintage cars, have their unique personalities. It’s hard not to smile and sigh when remembering the loyal, if flawed, rust bucket that shuttled a fresh, enthusiastic, and younger you to dates, dances, jobs, and adventures. Even when it broke down on occasion or you got into that first accident, those difficult moments became memories of growing up.

A first-love car isn’t just a machine. It’s a trusty sidekick, a partner in crime, a taste of freedom, and a gentle reminder of responsibility, usually at a time when life feels like an open road ahead of you.

For many people, a first-love car isn’t the first car they ever drove or owned but one they spent time dreaming about, saving for, or fixing up. Because they feel a close connection, losing that car can feel like losing a friend or family member, like it did for Hylen.

A Reunion

Hylen kept the Firebird in the back of his mind as the years went by. He served in the military; returned home to the Sacramento, California, area; got married; and became a sergeant in the Sutter County Sheriff ’s Office. Six years ago, he dug up the number of the guy he’d sold the Firebird to and called, asking hopefully, “Do you still have it?”

He didn’t, but referred Hylen to someone else, who gave him yet another contact. Hylen doggedly left messages and followed up on leads. He searched online for clues to its whereabouts using the Firebird’s vehicle identification number, but it didn’t appear. Hylen figured it was likely off the road, parked somewhere in a yard or garage.

Nearly two years later, he finally reached someone who had information. “I heard that it got torn apart,” he says. “I found it in a field. It was open, with no windshield— rotting away. It was in worse condition than the first time I bought it.”

Again, Hylen knocked on a door. When the owner learned of the car’s special meaning, he initially asked for $5,000, despite the car’s dilapidated state. Hylen managed to talk him down. “I’ve bought it twice, for a total of $1,900,” he laughs.

The Second Act

Since reuniting with his first-love Firebird, Hylen has taken great pleasure in a painstaking part-by-part restoration. “This time, I’m writing the checks to get the restoration done perfectly,” Hylen says. “That was the money I couldn’t spend to fix it up back when I was a teenager.”

“I’m not restoring it to factory condition,” he says. “I’m modernizing it to a pro-touring car, with updated brakes, tires, engine, suspension, heat, and air conditioning. Each body panel has been replaced. It has a modern motor and transmission: an all-aluminum LS3 from a Corvette.” So far, he’s spent well over $10,000 on the interior and ordered specially cut rims for $8,000.

The mismatched blue-white-black color scheme is gone, replaced by a custom gunmetal gray paint job he has wanted since his high school days. He drove from dealership to dealership—Audi, Porsche, Land Rover—to compare different finishes and get just the right shade. “I love that it’s tough looking but still sleek,” he says. “It’s actually a Porsche color.”

The restoration and modernization, or restomod, is on track to be completed in 2023. “It’s been a 25-year journey with this car,” says Hylen. “I’m 41, and I’m finally getting the car I wanted when I was 14, except it’s so much better. This car is going to drive like a new Corvette or Camaro.” He’s spent $100,000 altogether and plans to insure it for $140,000.

During the nearly five-year restoration, Hylen has connected with an active community of classic-car buffs in his area. Friends frequently bring their own rehabbed or restored vehicles to local auto shows, but Hylen hasn’t gone to any yet. He is biding his time for his car to be finished to debut it at a huge car show. “This summer, I’m going to drive it up to Reno for Hot August Nights,” he says. “I’m so excited.”

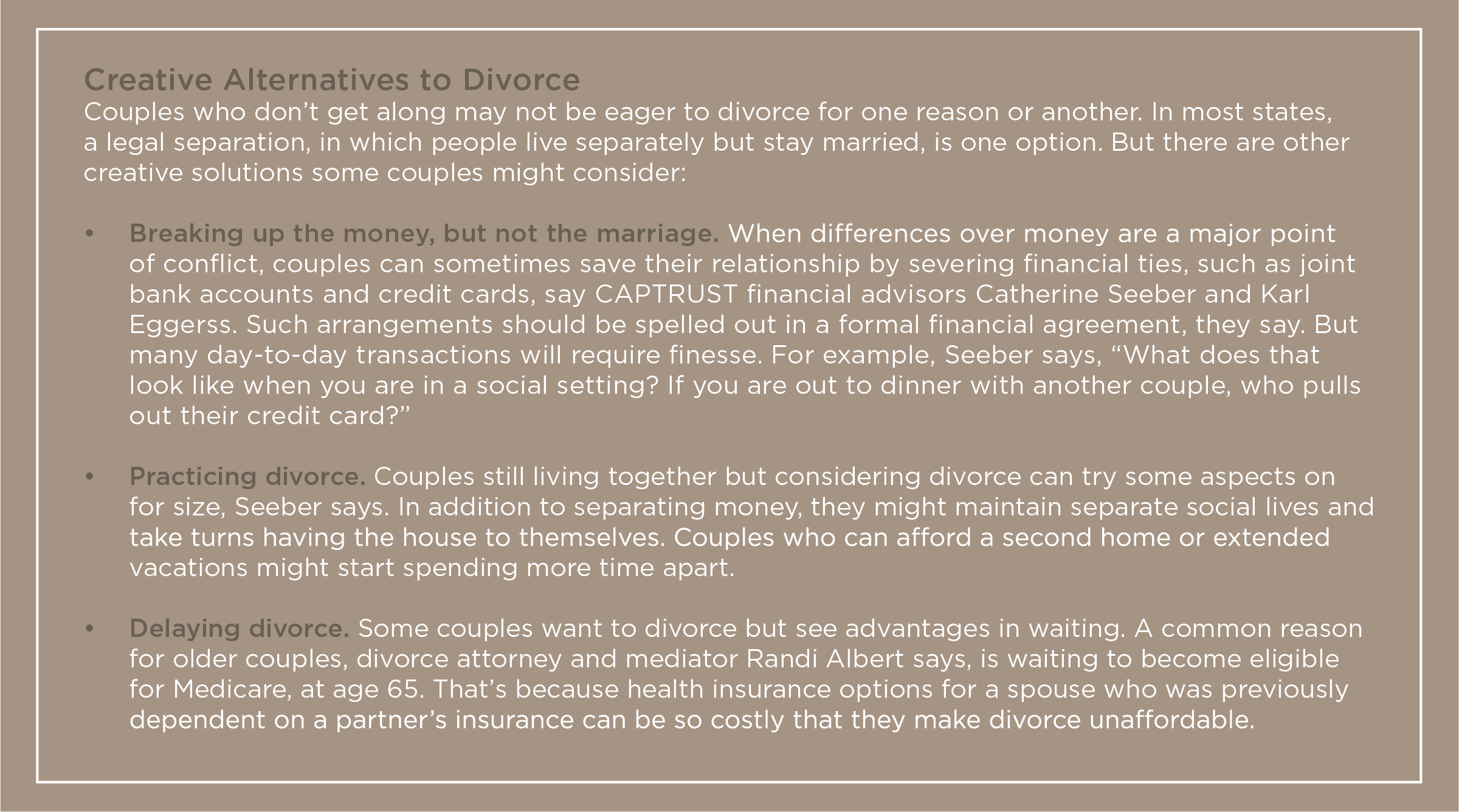

Frank blames herself, she says, for not knowing enough about her finances or divorce law and then rushing to complete the painful and costly process.

“I gave him free rein,” says Frank. “He did nothing wrong.” Frank lives in Hollywood, Florida, and has written two books: Divorced After 56 Years: Why Am I So Happy? and Life Has No Expiration Date: Misadventures of a Single Senior.

Divorce, at any age, comes with emotional costs. But, as Frank learned the hard way, a so-called gray divorce—a marital breakup after age 50—can also cost a lot of money, as years or decades of interrelated finances and acquired assets typically require extensive work to sort out.

“Divorce is definitely a financial hit for almost everyone,” and older couples face some extra challenges, says Randi Albert, an attorney who is a divorce mediator in Scotch Plains, New Jersey. The costs can be especially steep, experts say, for people who go into the process with too little information or planning.

Regardless of marital status, “it’s important to be aware of all your financial ins and outs, whether you are the money person in a relationship or not,” says Karl Eggerss, a CAPTRUST financial advisor in Boerne, Texas.

Even those who are happily married need to understand their personal finances to make good financial decisions. Yet Eggerss says he often sees couples rely on one person for financial management while the other partner remains disengaged.

CAPTRUST Financial Advisor Catherine Seeber, from Lewes, Delaware, agrees: “It’s common for one person to make all the financial decisions. I strongly encourage anyone who’s going through or considering divorce to talk to a financial advisor and understand all the things they need to gather to educate themselves. Otherwise, it can turn into a very emotional and reactive situation. Remember, a lot of irrevocable decisions are going to be made during this time.”

The Gray Divorce Trend

Gray divorce is much more common than it once was. Even as the overall U.S. divorce rate fell, the rate of divorce at age 50 and over doubled between 1990 and 2010, according to researchers at Bowling Green State University (BGSU). Since 2010, divorce rates over age 65 have continued to rise. Someone over age 65 was three times more likely to get a divorce in 2019 than in 1990.

More than one-third of all U.S. divorces now occur among people over age 50, researchers say. What’s causing all this later-life divorce?

Conventional wisdom says such divorces happen when a suddenly empty nest, a retirement, or a health crisis puts a rocky marriage to a test it simply can’t pass. But a recent study found no link between those transitions and post-50 divorce, says I-Fen Lin, a professor of sociology at BGSU.

Instead, Lin says, the trend is driven by generational shifts. Because baby boomers—now ages 58 to 76—entered adulthood just as divorce gained wide acceptance, they’ve remained more likely to divorce than generations before or after them. This is a generation that believes “it’s better to be alone than to be in an unhappy marriage,” she says. There’s also a snowball effect because remarriages are two and a half times more likely to end in divorce than first marriages. So remarried baby boomers often end up divorcing again. Today’s aging couples also live longer, giving them more time to divorce.

Another factor may be financial. According to Lin’s research, the odds of gray divorce are 38 percent lower for those with more than $250,000 in assets than those with $50,000 or less.

Lin and her colleague, Susan Brown, looked at the financial fallout of gray divorce and found a sobering picture, especially for women. Divorced women over age 50 see an average 45 percent drop in their standards of living after divorce, and men see a 21 percent drop. Men and women each lose about half of their wealth, including real estate, investments, savings, and other property, most likely as a direct result of divorce settlements.

If they remarry within a decade, most women regain their living standards and some of their wealth. But three-quarters stay single, Lin says. Remarriage does not help men regain their living standards or wealth. And because of their ages, gray divorcees have limited time to rebuild wealth in the future.

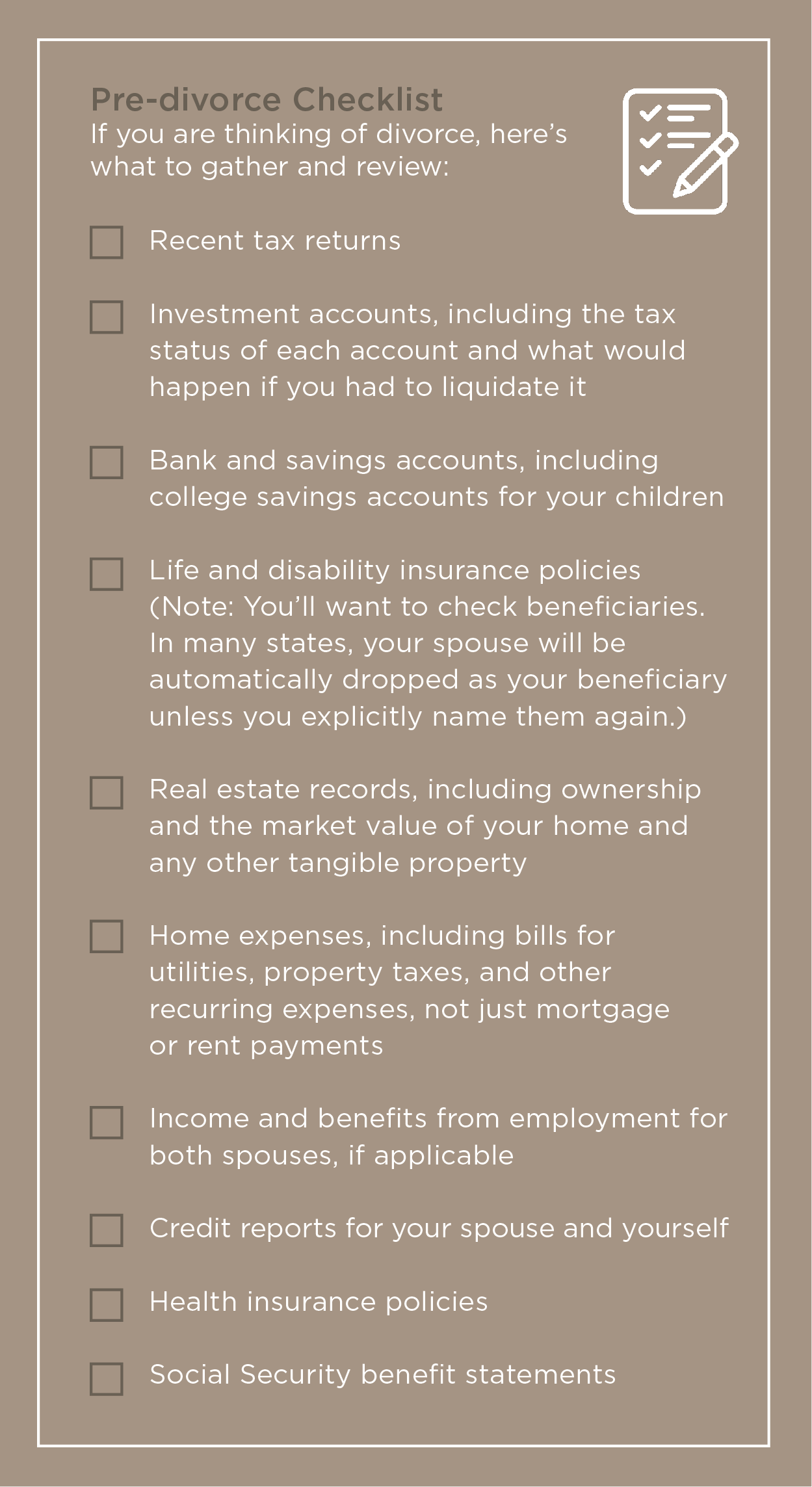

Do Your Homework

Fortunately, experts say, there are things you can do to soften such financial blows.

Eggerss says his first piece of advice is to take it slow unless there are strong reasons for haste. He likens the period around a marital breakup to the period around a death, when it’s wise to delay major life changes. “When people are under stress, they’re going to make really bad financial decisions,” he says.

That doesn’t mean you shouldn’t think about money. On the contrary, it’s crucial to do your homework on what assets, debts, income, and expenses you and your spouse have—and how a divorce might affect your bottom line, Eggerss and other experts say.

“I think a lot of people are putting finances on the back burner,” Eggerss says, “and then make this decision before they have really thought through whether they can afford to do it.”

If you haven’t paid close attention to family finances in the past, it’s especially crucial to get up to speed. Start by gathering account passwords, Seeber says: “Ensure you have online access to anything and everything financial.” You will want to see everything from your spouse’s credit report to their Social Security statements.

Keeping communication open and civil will make information exchanges easier, Eggerss says. Whatever you do, he says, don’t try dirty financial tricks, like funneling money into new accounts you hope to hide from your spouse. Such maneuvers are likely to be uncovered, he says: “You are not going to get away with it.”

Negotiate a Settlement

If you decide to move forward with a divorce, you and your spouse might hire separate divorce lawyers and battle over details or hire a mediator and work together on an agreement. Randi Albert, the New Jersey mediator, says some couples litigate part of their settlement and use a mediator to work through less contentious issues.

Also important to know: Nine states—Arizona, California, Idaho, Louisiana, Nevada, New Mexico, Texas, Washington, and Wisconsin— have community property laws that dictate an even split of all assets and debts built up during the marriage. Other states call for a fair and equitable split that considers factors like each spouse’s earning potential and contributions, such as child-rearing. Those rules apply if a couple hasn’t worked out their own property agreement before getting to court.

“People are more likely to follow an agreement that they’ve developed on their own, as opposed to one that was foisted upon them by the court,” Albert says. “So if you have the kind of relationship dynamic that allows you to work together, it’s definitely the way to go.”

Fairly dividing assets isn’t easy though. “It’s really not advisable to just put numbers on paper,” Seeber says, and decide, for example, that one spouse will take a house valued at $1 million and another will take investments valued at $1 million. You need to consider home maintenance costs and the tax hit you might take after an eventual sale, she says. If your money is tied up in a home, will you have cash available when you need it? Will you have enough credit to borrow in the future? If you are receiving an investment account, are proceeds taxable, or not? “You have to run the long-term projection to be able to say that, in 10 years, you really still are equal,” Seeber says.

Albert and her partner, family therapist Michele Weinberg, say they encourage divorcing spouses to run draft property agreements past separate financial advisors as well as separate attorneys.

Weinberg cautions that some gray divorcees will need to work years longer or go back to work after retirement to pay alimony or cover new living costs. “Sometimes, people who have never worked or have worked in a limited way now have to find a full-time job,” she says.

Couples who own a business together will face additional challenges. Will the business be sold, bought out by one spouse, or reorganized with two ex-spouse owners? The last is a fraught situation most people reject, Weinberg notes.

Divorce typically also means reconsidering everything from wills to plans for long-term care. Someone who expected a spouse to care for them in their later years will now need other options. That might mean moving in with a friend or jump- starting a move to an over-55 or assisted living community, says Eggerss.

Frank, the Florida divorcee and author, says she’s been able to stay happily single in her own apartment. She’s doing just fine now, she says. But she does share this advice for anyone going through a late-life divorce: “A second pair of eyes and ears, even from a trusted friend, can save you time, money, and grief. Don’t sign or agree to anything without having someone else review it.”

An ancient art form around the world, calligraphy has stood the test of time. What began as a way to preserve historical and religious texts has become a form of personal expression now used in everyday life.

From diplomas on sheepskin to elaborate wedding invitations on heavy card stock, calligraphy has elevated the look and feel of documents and paper products for centuries.

The precision of calligraphy’s nib-to-ink process is part of its allure. “The basic definition of calligraphy is just beautiful writing,” says Carole Murray. Murray owns and operates a custom calligraphy business, Calligraphy by Carole, based in Winston-Salem, North Carolina. In recent years, demand for calligraphy services has grown rapidly across the country, with thousands of professional calligraphers now creating art and products in their own distinct styles.

Murray’s interest in calligraphy was first sparked in the 1980s when she wanted to address the envelopes for her wedding invitations. But it wasn’t until 2008 that she turned her hobby into a full-time job, focusing on the wedding industry. Murray offers products ranging from table numbers and place cards to invitations and large signage. Her work is based on the copperplate style, a method of writing that has existed for centuries.

If you’re learning calligraphy today, it is likely based on the copperplate script. The writing instrument—a nib—is dipped in ink and then whisked, dragged, or flicked across the page as necessary to achieve the desired effect. The fundamental techniques are upstrokes and downstrokes, which work together to create the shape and width of each letter.

Murray describes her process: “I use a pointed pen nib that fits into an oblique holder. I dip the nib into calligraphy ink. When I apply pressure on my downstrokes, the slit in the nib will open and separate the two tines, allowing the ink to flow out thicker. When I don’t apply much pressure— typically on the upstrokes—the lines are thinner.”

Something for Everyone

Another, perhaps more approachable, style is modern calligraphy, which some say requires less precision. Modern calligraphy can also be described as loopy calligraphy. Jess Perelle, owner of Letter and Ink in Los Angeles, California, uses this style in her full- service design studio. “Modern calligraphy is a more casual, free-form version of calligraphy,” she says.

Perelle has always been an artist and dates her interest in calligraphy all the way back to middle school. “I started a little business, writing people’s names in Crayola marker,” she says. “I do that now, but the fancy version.”

Today, her design work includes custom drawings, wax seals, and letterpress designs. Perelle is self-taught from the comfort of her coffee table through a combination of online videos, classes, and ample practice.

A Sense of Nostalgia

In part, calligraphy’s growing popularity may be attributed to a sense of nostalgia and society’s enduring feelings of delight around physical objects. In an increasingly digital world, it still feels good to turn the pages of a book or receive a handwritten note.

“When you get your mail, aren’t you looking for something that’s handwritten first?” says Murray. “People still like anything handwritten. If it’s written in calligraphy, that is even better.” Handwritten items carry a sense of human connection that printed materials cannot emulate.

Maghon Taylor of All She Wrote Notes, a calligraphy studio and classroom in Gibsonville, North Carolina, felt a similar connection when she inherited a calligraphy set from her grandmother. “I had always loved doodling and handwriting, so I wondered if I could learn. I signed up for a calligraphy class, and I was not good at all!” she says.

Taylor strayed away from the traditional copperplate style and practiced at home in her own way. She found the most joy and success in hand lettering, a whimsical style she has coined faux-ligraphy. With hand lettering, there’s flexibility to use pointed-tip markers in lieu of the traditional nib and ink, plus options to write on unconventional materials—like chalkboards, holiday ornaments, or signage—in addition to paper.

Handwriting and lettering can be just as much of an heirloom as jewelry or other possessions. “In a world where everything is text and email and digital, handwriting is such a legacy,” says Taylor. The market for reprinting and preserving the handwriting of loved ones has expanded rapidly in recent years. On sites like Etsy, you’ll find custom products that can include your loved one’s handwriting etched into jewelry; printed on tea towels; burned into cutting boards; or featured prominently on scrapbooks, ornaments, bags, coffee cups, and more.

“If I could have anything of my grandmother’s, it would be something with her handwriting,” says Taylor.

Just Put Pen to Paper

Taylor turned her interest in handwriting into a career. She now teaches classes in person and virtually, has written four books about calligraphy, and sells products of her own design through Walmart stores nationwide.

But calligraphy doesn’t have to be your passion to be fun and impactful, Taylor says. She encourages her students to simply start somewhere and get back to handwriting. “Don’t worry about perfection; just start writing again,” she says.

Especially for those who may be worried about shaky hands or handwriting changes that sometimes come with aging, hand lettering can be a more forgiving technique than the nib-and-ink approach. After all, a handwritten note is a treasure no matter what the writing looks like.

Also, handwriting is good for the brain. A study from the University of Tokyo suggests, “The act of physically writing things down on paper is associated with more robust brain activation in multiple areas and better memory recall.”

Murray agrees. “Your hand, after all these years, still knows what to do,” she says. Sometimes, the action of handwriting and modern calligraphy can even feel meditative.

“It’s really not like writing; it’s like drawing letters,” Murray says. “You get into a rhythm when you write, and it’s very therapeutic.”

These days, there are thousands of online classes available across the country, and most major cities have calligraphy groups that meet in person to practice together. Writing place cards for a dinner party and addressing an envelope to a friend are two simple ways to get started.

“Who doesn’t love to see their name written beautifully? It’s just a special touch,” says Murray. And it’s one that has endured for centuries.

At the heart of this détente was the concept of mutually assured destruction, otherwise known as MAD, an appropriate acronym for the idea that should one of the then-superpowers launch a military attack or invade a sovereign nation, the other would retaliate with an all-out nuclear strike. And, of course, that strike would be followed by another retaliation, creating a cycle of destruction so dire that neither side would dare to start it.

The Day After

Thankfully, the Cold War came and went without MAD. Nonetheless, growing up during the Cold War meant that you lived with the constant overhang of nuclear war. This was made real to American citizens by duck-and-cover air raid drills at school, signs denoting fallout shelters intended to house survivors in the event of nuclear war, and myriad science fiction dramas, such as Dr. Strangelove, A Boy and His Dog, and the made-for-TV movie The Day After.

The Day After portrays a superpower skirmish over Germany that escalates into a full-scale nuclear war. The story is told through the eyes of regular Americans as they experience the bleak aftermath of a nuclear exchange. More than 100 million people watched the film during its initial broadcast on November 20, 1983, which made it the highest-rated television film in history, a record it held for more than 25 years.

Of course, we no longer have the Cold War in its original format, but we have since written or produced the end of the world countless times via movies, television series, and books. Let’s face it; humans are good at catastrophic thinking.

No Nukes Needed

Catastrophic thinking—or catastrophizing—occurs when you imagine that the worst possible outcome will occur in a situation with little basis in fact or reason, according to the American Psychological Association (APA). Sometimes, that imagined outcome results from a choice you have made. It’s a type of cognitive distortion we all experience at one time or another. Catastrophic thinking is part of being human.

It doesn’t take the threat of nuclear holocaust to set us off. It can start with a small thought that escalates rapidly, leading to stress and anxiety. In turn, this anxiety may cause you to react impulsively or keep you from reacting when action is required. At the very least, it creates worry.

Catastrophic thinking takes many forms. It happens in small ways when we are hours from home and wonder if we closed the garage door, when we text a friend and don’t get an immediate reply, or when we make a mistake at work. It happens in big ways as we absorb the news of the day: the 9/11 attacks, the financial crisis, or war in Ukraine.

In any case, thanks to our ancient ancestors, our brains are experts at extrapolating inputs into their worst-case outcomes. When early humans were wandering the savannas, underestimating what was rustling in the bushes ahead could be deadly. As a result, evolution has endowed us with survival instincts when faced with uncertainties, big and small. Sadly, some of these instincts are ill-suited to modern life.

Time Traveling

The financial version of catastrophic thinking comes in many flavors. A recent economic downturn may fuel fears of being laid off. Loss of a big client may make you feel like your job is in jeopardy. A market pullback or concerns about the future of Social Security may make you question if you’ll ever be able to retire. Worry and fear about money issues like these can lead to stress, insomnia, and depression.

A common theme is time travel—these catastrophes exist in the future—so the first step to heading off catastrophic thinking is to stop leaping ahead and focus on what is true right now. Here are four tips to help you manage your catastrophic thinking when it arises.

Replace fears with facts. It’s impossible to be reasonable when you’re in a state of fear, so shift your thinking to your rational brain. “Ignore the mass media,” says CAPTRUST Senior Director and Portfolio Manager Jim Underwood. “You can always find what you’re looking for, so you’ll likely find plenty to support your fears there. Instead, engage experts, read up on the topic, or talk to a trusted friend about your fears.”

Look at the worst-case scenario using data from the past to inform what you think might actually happen in the future. You should quickly find that, while possible, your worst fears are highly improbable. “The fact is, and history supports this, the worst outcome we think about is also the least likely to occur,” says Underwood.

Explore the in-between. Catastrophizing is a form of binary— that is, either/or—thinking. And human nature inclines us to focus on and worry about the negative possible outcomes more than we relish the positive ones. Instead, explore all possible outcomes: bad (but informed by facts!), good, and in-between.

Ask yourself: Is this what I really think will happen? While the worst case could happen, what is most likely to happen? When you dig into the most likely outcome, you may be relieved to find there is much to like about it. It may be much closer to the best-case than the worst-case scenario.

Take appropriate action. We don’t rule the world around us, so catastrophic thinking is often enhanced by a fear that we might end up as victims of forces that are beyond our control. This fear can drive us to take action as a way to feel better and regain a sense of control.

“When and if you feel this urge, make sure that you are not acting rashly,” says Underwood. “Make sure that your actions are based on facts rather than emotion. In reacting to the worst case, you don’t want to make an all-or-nothing decision that closes you off to the best-case or most likely scenarios.”

Live and learn. While you may worry or engage in catastrophic thinking, you are not alone. It’s part of the human condition, not a mental disorder. Our brains are unique tools that have given us many advantages. They also carry baggage from a simpler but much more dangerous time. When you feel yourself slipping into a mental catastrophe, take note, call a time-out, and let yourself off the hook.

“In the end, rather than catastrophizing, it’s important to focus on controlling the variables we can control,” says Underwood. “That includes using data to inform our thinking and trying to manage our emotional state. Things rarely turn out as bad as we fear, so it doesn’t make sense to lose sleep over them.”

How bad could it be, after all? It’s not like the world is going to end.

“I did not have any intention to foster,” says Sanders, an independent consultant in Raleigh, North Carolina. “It was not on my radar at all.” She had never been a parent, foster or otherwise.

But some friends had encouraged her to volunteer with a youth group. Some of the kids were from unstable family situations, and the activities provided them with a respite. “They needed me, and the people steering me to it thought I needed it too,” she says.

Immediately, she felt a sense of purpose, helping teenagers and finding out about their circumstances. In particular, she hit it off with one boy, Mark, a teen who seemed to have adult-sized burdens on his shoulders. He was staying in a temporary foster home with his younger sister, Maddie, and was also trying his best to look out for his mother, who was struggling with issues of her own.

Sanders saw quickly that this young man deserved to have some lightness and joy and a chance to act his age. On a long drive to a camp in the mountains, “he just talked my ear off,” she says. “It was unusual that he had so much fun with me, and that was noticed. That’s how this whole thing started.”

Later, the group leaders asked Sanders if she would consider taking the siblings into her home, just for a couple of weeks, to help relieve pressure at their temporary living situation. More than that, if she was willing, these weeks could be a trial run to becoming their foster parent.

“It was a new endeavor to work with youth,” Sanders says. “I have been my own person for a long time. Now, helping teens become their own person is fascinating.”

Multiple Entry Points

People don’t often think of midlife and beyond as prime parenting years. But older folks, empty nesters, and retirees have a lot to offer to kids in need. Also, many baby boomers and generation xers feel a strong desire to give back. They may have more time, patience, and resources at their disposal than in the earlier stages of their lives. The idea of channeling some of that energy to help nurture children in distress can be appealing.

Sanders agreed to the trial period. She felt herself already falling for Mark and Maddie (not their real names)—and seriously considering turning her life upside down for them. She reasoned, “I’m in my late 50s, widowed,” she says. “I have no kids. I have means—not endless means—but it’s not going to hurt me. It’ll stretch me mightily, but these are good kids, and they don’t have any good options. They were going to be split up, and I couldn’t bear it. I didn’t want them stretched.” She soon realized she would take them.

Sanders attended many Saturdays of foster training conducted by county social workers, who also visited her home and checked personal references as part of their process. Since she already had a relationship with the kids through the youth group—what social workers call a kinship—the teens were able to live with her during her training period. “I’d mostly heard about people fostering who already had kids, raised and grown, but that ain’t the only way! There is no one path to all of this,” she says.

Where to Start

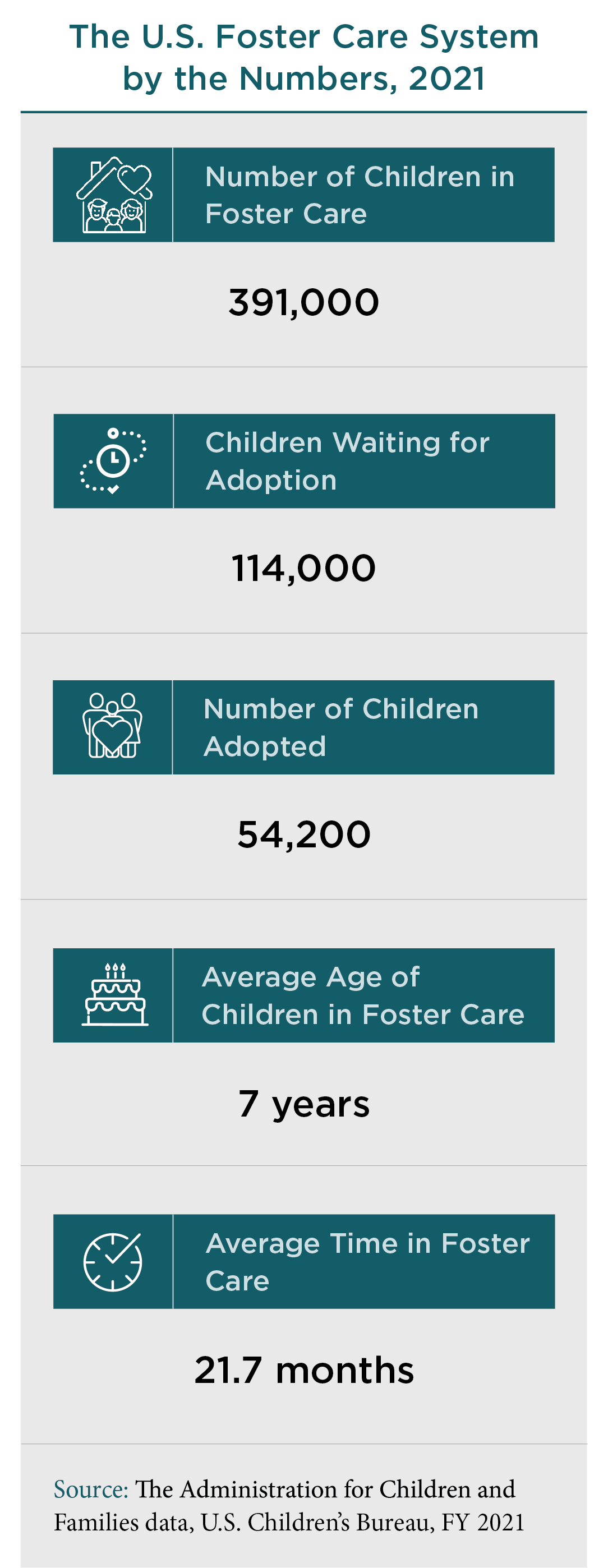

The U.S. child welfare system is notoriously complicated, and there is a perennial shortage of foster families. The need is great. In 2021, there were 391,000 U.S. children in foster care, according to the Department of Health and Human Services. At year-end, 54,200 children had been adopted out of the system, and another 114,000 children were awaiting adoption.

For parents and non-parents alike, fostering later in life has both challenges and rewards, especially considering that many kids enter the system after experiencing neglect or abuse in their youngest years.

The foster process varies by state and sometimes by county. Anyone who is exploring the idea of fostering can learn about the steps required in their community by reaching out to a local foster care agency.

A directory of state and local agencies is available on childwelfare.gov, the federal Child Welfare Information Gateway. There are also national agencies, such as AdoptUSKids, Casey Family Programs, and Kidsave.

The National Foster Parent Association has resources for online education and training. Generally, to become licensed, foster parents undergo 10 to 30 hours of training and complete interviews, a home inspection, medical exams, background checks, and financial assessments.

Sanders and the kids have been together ever since, including throughout the COVID-19 lockdown, when their world shrank to only three. It sometimes feels strange to her how deeply connected they became—and how quickly—in the house she had once planned to sell. Now there are dings on the walls, but she’s in no hurry to fix them. After all, she recently became legal guardian to the siblings, so “we will be here for a while.”

Sometimes, Sanders says she wonders what her late wife would think about her life now, her new family, and her role as a foster mom to two teens. It’s not a path that the two of them would have chosen together, she is certain. Her wife had a child already, one who is now a 32-year-old adult. “She’d been there, done that,” says Sanders. “This is my adventure, but I think she had a hand in it. I think she’s laughing.”

How would her wife have responded to the two teens? “I think she sent them,” Sanders says.

Q: What are digital assets, and what role do they play in estate planning?

A digital asset is any item or information that is stored electronically. Most commonly, this means your logins, passwords, PINs, and anything contained within an online account. What happens to these accounts when you die? The answer depends on the type of account and whether you have included its assets as part of your estate plan.

To add digital assets to your estate plan, start by making a list of all accounts. If you are already using a password management application, such as 1Password, LastPass, NordPass, or Keeper, a master list will be included as part of the service. Internet browsers can also show a list of saved logins and passwords. Check under settings and search for passwords.

Next, determine which accounts are valuable to you. Even if the asset has no financial value, its emotional significance might mean it’s worth saving. For instance, you may save your photo storage accounts and movie or music collections. In general, don’t bother creating plans for online shopping accounts, since these are likely to be deactivated on their own after a certain period of inactivity.

Most social media and email accounts have end-of-life provisions that can automatically transfer the account to a designated person after a specific number of days without access. But you must make sure you set these up.

For cryptocurrency, there are various digital asset inheritance services, such as Inheriti by Safe Haven and Covenant by Casa, that will guide your beneficiary through the transfer process.

Financial institutions do not recommend letting anyone else access your account using your credentials, whether you are dead or alive. Usually, your spouse or executor will simply need to contact the company and let them know you are deceased to begin the closure process. All financial accounts, including credit and debit cards, should be shut down soon after death to prevent fraud.

One digital asset worth preserving: Your frequent flyer accounts. Most airlines will transfer miles to a spouse or child.

As part of your estate planning, you will want to designate a specific person and provide them with authority to manage your digital assets. However, this does not mean you should include your passcodes or other access information in your will. When you die, your will becomes a public document, which means anyone can read it.

One solution is to reference an outside document in your will that contains all the necessary information to settle your digital estate. This way, you can continue to revise and update the outside document without having to either change your will or put your digital assets at risk.

By including digital assets as part of your estate plan, you make things easier for your loved ones, who would otherwise be responsible for tracking down and managing these accounts.

Yes, it means getting organized now, but doing so will protect you both in the short term and long after you are gone.

Q: Last year was challenging for my fixed income investments, but I hear 2023 might be a good time to buy bonds, specifically municipal bonds. Is that true?

From an investment perspective, 2022 was a wild ride. Just as quickly as interest rates rose, bond prices fell. You probably saw the headlines that said fixed income isn’t working anymore. Now, the same media outlets are saying it’s a good time to invest in bonds. At first, those comments may seem at odds, but the truth is that they’re intertwined because 2022 market conditions created an attractive environment for future returns on bonds.

As with most areas of investing, deciding if tax-exempt municipal bonds are a good fit for your portfolio will depend on your unique circumstances. However, for those who are considering buying bonds, it may be helpful to understand what makes an attractive municipal bond environment. In 2023, tax-exempt bonds, such as municipal bonds, may offer a compelling opportunity for four reasons:

- Attractive yields. The yield on any bond is the expected return on investment over its remaining life. Today, both tax-equivalent yields and overall yields on core municipal bonds are near decade highs.

- Improved financial conditions. Historically, credit defaults on investment-grade municipal bonds are exceptionally low. In the past few years, many municipalities have further strengthened their financial positions, accumulating cash reserves through federal stimulus programs and robust tax collections.

- Increased demand. With a divided Congress, significant changes to individual tax rates are unlikely. The combination of stable tax rates and improved credit fundamentals is likely to increase investor demand for tax-exempt municipal bonds.

- Limited supply. Typically, the supply of new municipal bonds is driven by entities that are refinancing existing debt. With the recent surge in bond yields, refinancing is significantly more expensive, thereby limiting the overall supply of bonds. Also, with increased cash reserves, municipalities may choose to delay additional capital raises in hopes of lower future rates. While there will always be exceptions to every rule, in this case, most investors are likely to be rewarded for locking in decade- high yields for the foreseeable future, even if the journey remains a little bumpy.

Q: I am the primary financial decision maker in my household. How do I encourage my spouse to be more engaged in our finances?

When it comes to financial matters, having two informed and active partners is almost always better than one. You’ll make stronger decisions, and you can ensure that neither of you ends up lost or overwhelmed with financial business when the other partner is disabled, is incapacitated, or dies.

It is common for spouses to have different financial personalities—for instance, different perspectives on spending, philanthropy, or risk. You don’t need to be completely aligned to have a unified financial life. What’s more important is that both people participate in reaching decisions. Here are a few steps you might consider to get your partner more engaged.

First, let them know why you want their involvement and perspective. Think of your financial life as a road trip. You will only need one driver at a time, but it’s helpful when the person in the passenger’s seat knows where you are headed and can be excited about it. If your partner can also help you navigate the turns, that’s even better.

If you don’t have a will, this can be a great first step to take together. Developing a will and an estate plan often involves dozens of decisions that will jump-start conversations about financial goals and desires. For instance, do you both have contact information for your tax, legal, and financial advisors? Does your spouse know the access code for your phone and where the keys to your safe are located?

It’s common for the less-engaged spouse to feel embarrassed, frustrated, or overwhelmed at first. Be patient as your partner learns the ropes.

You may also want to consider a similar process with your adult children and parents. By handing over financial knowledge before it is truly necessary, you can minimize emotional decision-making and avoid traditional pitfalls in the generational transfer of wealth.

It may be helpful to create a visual map of your financial life—including assets, accounts, and advisors—to illustrate how your money moves around and who else is involved in the process. Connecting family members with professional advisors is a critical piece of the puzzle, even if only by email.

And remember: Working as a financial team is like dancing together. For your partner to take a step forward, you’ll need to take at least a small step back.

SECURE 2.0: Investment and Fiduciary Issues

The widely reported SECURE 2.0 law includes more than 90 provisions, most of which pertain to retirement plan design and operation. As a point of reference, the first SECURE Act included only 31 provisions. A few provisions of the new law relate directly to fiduciary and investment issues.

- 403(b) plans, which are a close cousin to 401(k) plans, have not been permitted to use collective investment trusts (CITs). CITs have long been used in 401(k) plans for stable value investments, and CIT versions of traditional mutual funds are increasingly used in 401(k) plans to reduce investment expenses. The new law permits 403(b) plans to use CITs. Although the rule is effective as of December 29, 2022, this provision will not be available until corresponding changes are made in securities laws.

- Under current fiduciary law, when a plan participant is overpaid from plan assets, plan fiduciaries must take reasonable steps to recover the overpayment. SECURE 2.0 leaves recovery of overpayments to the discretion of plan fiduciaries. Under tax law, if the exact terms of a retirement plan are not followed, including overpayments to participants, the plan’s tax-preferred status can be challenged by the Internal Revenue Service (IRS). The IRS has previously issued guidance providing some relief if overpayments are not recovered, and SECURE 2.0 codifies preservation of a plan’s tax-preferred status if overpayments are not recovered. Plan sponsors experiencing a situation like this should consult with their ERISA attorneys for guidance.

A few other aspects of SECURE 2.0 touch on topics that have been covered in earlier Fiduciary Updates.

- The penalty for not taking required minimum distributions (RMDs) has been reduced from 50 percent of the late distribution amount to 25 percent of the late distribution amount. This penalty is further reduced to 10 percent if the corrective distribution is made during a two-year correction window.

- The 10 percent withdrawal penalty for early retirement plan distributions will be waived for individuals with an illness that is reasonably expected to result in death within 7 years, per a doctor’s certification.

401(k) and 403(b) Fee Cases Continue

The flow of cases alleging fiduciary breaches through the overpayment of fees and the retention of underperforming investments in 401(k) and 403(b) plans continues but without significant new developments. Here are a few updates.

- Two of the approximately 10 cases alleging that it was a fiduciary breach to retain the BlackRock LifePath Index Funds have been dismissed and amended complaints have been filed. The challenged funds are an indexed target date series with a to-retirement design. Tullgren v. Booz Allen Hamilton v. Hall (E.D. Va. 2022); Hall v. Capital One Financial Group (E.D. Va. 2022).

- We previously reported on three Court of Appeals decisions dismissing fees suits because the initial claims did not sufficiently make a case that plan fiduciaries had breached their duties. District courts have applied the reasoning of these cases and dismissed other cases early in the litigation process. Nohara v. Prevea Clinic (E.D. Wis. 2022); Glick v. Thedacare (E.D. Wis. 2022).

- In a rare victory for a plaintiff in an ERISA fiduciary breach case, a judge in Connecticut has permitted a jury trial on some claims. Garthwait v. Evercore Energy Co. (D. Conn. 2022). Over the years, judges have written many pages on whether a jury trial is available in ERISA cases, with virtually all concluding no. Juries decide cases where the resolution would be legal, such as resolving an alleged breach of contract, and judges decide cases where the resolution would be equitable in nature. This is generally understood to be the situation with issues involving trusts, which fund retirement plans.

$750,000 Cybersecurity Loss Case Progresses with One Defendant Out

We have previously reported on a participant’s lawsuit attempting to recover more than $750,000 taken from her 401(k) account through cyber-fraud. The suit was filed against the recordkeeper, the plan fiduciaries, and the asset custodian/trustee, alleging various fiduciary breaches in making or allowing the fraudulent distribution. All three defendants filed motions to dismiss.

The asset custodian/trustee was released from the case, but the recordkeeper and plan fiduciaries were not. The court concluded that the asset custodian/trustee was not a fiduciary because it did not exercise any discretion or independent control over the plan or its assets. Its role was exclusively to follow the directions of others. This directed trustee role is different from the role discretionary common law trustees play in retirement plans, such as deciding which investments to offer in a 401(k) plan.

The judge noted that plan fiduciaries could be liable for the loss if they failed to reasonably select or monitor the recordkeeper. However, he observed that, “ERISA’s duty of care requires prudence not prescience. [Fiduciaries] must adopt reasonable procedures, but not absolutely air-tight procedures, to protect against the possibility of what happened here, which was a heinous crime.”

With respect to the recordkeeper, Alight, the court found that it may be considered a functional fiduciary but cautioned that it might not be. Under ERISA, a person or institution is a fiduciary if they exercise discretion or control over plan assets, regardless of whether they have been appointed as a fiduciary. The judge took the unusual step of recommending that the participant file a negligence suit against Alight. He went on to point out that the statute of limitations would run out in March 2023, concluding with, “the clock is ticking.” Disberry v. Employee Relations Committee of The Colgate-Palmolive Company (S.D. NY 2022).

Surprise! Ex-husband Inherits 401(k) Account Balance

A plan participant was divorced in 2002, and it was agreed that her ex-husband would have no claim to her 401(k) account. At that time, the ex-husband was the sole beneficiary. In 2008, the participant changed her 401(k) plan beneficiary from her ex-husband to her three siblings, with each to receive 33 1/3 percent. Unfortunately, the beneficiary designation form required that the allocation be in whole percentages. As a result, the beneficiary change was rejected.

In 2019, when the participant died, her $600,000 401(k) benefit was paid to her ex-husband. The participant’s estate sued the plan sponsor for breach of fiduciary duty in failing to correct the beneficiary designation form. At trial, it was revealed that, soon after the erroneous beneficiary designation form was submitted, the plan sponsor telephoned the participant and left a message notifying her of the error. The participant also received 11 annual account statements showing her ex-husband as the sole beneficiary. Award of the 401(k) account to the ex-husband was upheld at trial and on appeal. Gelschus v. Hogen (8th Cir. 2022).

Surprise! $24,000 Payment Resolves $2 Million Claim

An insurance company determined that it had overpaid a healthcare provider in Texas by more than $2 million through the payment of participant claims. The insurance company demanded repayment and months of discussions and correspondence ensued, but no agreement was reached. The provider eventually sent a letter and refund check for $24,000 to the insurance company.

The check included a notation saying it was in “full and final payment” of the repayment claim. Copies of the letter and check were sent to seven different addresses and individuals at the insurance company who had been involved in the negotiations. The physical check was sent to the insurance company’s lockbox where payments were received.

Five days after the letters were received by individuals at the insurance company, the check was deposited by the lockbox provider, and copies of the check and letter were scanned into the insurer’s tracking system. The next day, upon seeing the letter and check in the tracking system, an insurance company representative emailed the healthcare provider’s general counsel to reject the settlement offer.

The healthcare provider contended that acceptance of the check was full satisfaction of the insurer’s claim for reimbursement. Disappointed with that outcome, the insurance company sued. Applying Texas law, the trial court and court of appeals concluded that acceptance of the $24,000 check resolved the matter. United Healthcare of Texas, Inc. v. Low-T Physicians Service (Tex. App.—Fort Worth 1-5-23).

Accidental Death Coverage: What Is an Accident?

In addition to traditional life insurance, many employers’ benefit programs include additional coverage if a death is the result of an accident. Two recent cases illustrate differing outcomes.

In Goldfarb v. Reliance Standard Insurance Co. (S.D. Fla. 2023), a covered employee was an avid mountain climber. He decided to go mountain climbing in Pakistan in the winter. After making reasonable preparations, he embarked—but did not return. Aerial surveillance identified a body and what appeared to be his equipment in the area where he was climbing. The employee was then declared dead.

A claim for accidental death benefits was denied, with the insurance carrier taking the position that winter mountain climbing in Pakistan was so dangerous that death was not considered an accident. However, the policy did not have a mountain climbing exclusion. The trial court found that the deceased did not expect his mountain climbing expedition to cause serious injury or death. The accidental death benefit was ordered to be paid.

In another accidental death case, McChristion v. Sun Life Assurance Co. of Canada (W.D. Tex. 2022), a motorcyclist lost control and wound up under the trailer of an 18-wheel truck. He was dragged for some distance and did not survive. The crashed motorcycle’s speedometer was found locked at 105 miles per hour. Where the accident happened, the speed limit was 45 miles per hour.

The employer-provided accidental death insurance claim was denied. In this case, the denial was upheld because the behavior of the deceased was so intentionally reckless that it was excluded. The claim was also denied because it resulted from criminal behavior in the violation of motor vehicle laws, but the judge did not reach this issue.

DOL Finalizes ESG Regulation

In November 2022, the most recent volley of guidance from the U.S. Department of Labor on the use of environmental, social, and governance (ESG) factors, also known as socially responsible investment factors, in retirement plan investments became final. The bottom lines continue to be:

- In ERISA-covered plans, investment decisions must be made based on economic factors and in the best interests of plan participants and their beneficiaries.

- In certain cases, ESG factors may be considered economic factors by plan fiduciaries.

- Making socially responsible investments available to participants through a self-directed brokerage vehicle versus a core investment option can be advantageous.

- If properly structured, plan fiduciaries are not responsible for specific investments available in the brokerage window.

- If socially responsible funds will be made available, a brokerage window can permit a wide range of choices for plan participants to select what they are passionate about.

Becoming a parent is a life-changing adventure, one that can be fun, fulfilling, nerve-wracking, exciting, and overwhelming all at the same time. New babies often make us dream about the future, and we feel encouraged to make plans that will help ensure the best possible outcomes.

As you consider what your family’s future could look like, take time to evaluate your financial health. This financial checklist for new parents may be a helpful resource.

Health Care

- Review your deductible, co-pay, and maximum spending amounts for health insurance.

- Look to see what your policy year is (i.e., the 12-month period before your deductible, maximum spending, and other key metrics reset). If pregnancy and the child’s birth will occur in separate policy years, the timing could impact your out-of-pocket costs.

- Check if pregnancy and birth are covered under your existing insurance policy. If not, reach out to your insurance company to explore your options.

Tax Planning for the Year after Birth

- Learn about new tax deductions and credits and ensure your tax professional knows you had a child.

- Consider the child tax credit, dependent care tax credit, dependency exemption, flexible spending account (FSA), and medical expense deductions.

Foundational Planning (101)

- Edit your budget to include new monthly expenses that could be anywhere from a few hundred to a few thousand dollars. Beyond the universal pieces, such as diapers, clothing, food, and toys, some families may also need to account for childcare, increased doctor visits, medical expenses, and more.

- Consider setting up a savings account specifically for unexpected expenses, such as car repairs or home maintenance, with three to six months’ living expenses.

- Make a list of all your debts and put them in order of importance.

- Review insurance coverage to ensure you have adequate protection for your family, including insurance for your home, vehicles, potential disabilities, and long-term care.

- Review your retirement savings and make sure you are on track to meet your goals.

Next-Step Planning (201)

- Create or revise your estate planning documents, including a will to outline financial and parental guardianship if you and your spouse die prematurely.

- Set up a financial power of attorney to designate someone who can manage your financial affairs if you become incapacitated.

- Review your life insurance coverage to ensure your family has sufficient financial resources if something should happen to you.

- Consider an umbrella insurance policy to provide additional coverage for things like hosting large gatherings or having a pool or trampoline.

Education Savings

- Start saving for your child’s education as early as possible. There are several options for education savings, including a 529 plan, a Coverdell Education Savings Account, or a custodial account.

- Consider having family members and friends help fund the plan with regular gifts.

- Be aware of annual contribution limits.

- Remember that the primary benefit of education savings programs comes from their investment returns, so the earlier you start, the more opportunity for those returns to accrue.

Consult with your financial advisor for additional resources and help with planning.

According to a survey by the Funeral and Memorial Information Council, while 69 percent of American adults want to arrange their own funerals, only 17 percent have put plans in place. Regardless of your age, health, or financial circumstances, CAPTRUST Financial Advisor Christeen Reeg says, “creating a sketch for your own funeral is a smart decision.”

Yet most people don’t.

This inaction is likely because planning for death—or even talking about it with family and loved ones—is uncomfortable for most people. Brit Guerin, co-founder of Current Wellness and a licensed mental health counselor, says talking about death brings up emotions people don’t want to feel. “Talking about a loved one dying often feels taboo, in part because we don’t know what to say. It can bring up intense grief and sadness that are difficult to put words to.” Planning a funeral means accepting death.

But planning also makes death easier for your loved ones to navigate. And, it ensures your life will be celebrated according to your own thoughtful decisions, not the emotional and often rushed decisions of your grieving family.

Plan the Funeral You Want

“It’s important to know in advance what your loved one’s desires are,” says Guerin’s colleague and professional grief counselor, Monica Money. “Many times, family members want to do something different, even if the one who is dying has expressed their plans. That is why it is so important to have your wants and desires put in writing and kept in a safe place.”

When making arrangements, plans can be as general or specific as you like. Things like burial plots, service music, reception locations, and pallbearers can be finalized ahead of time. If you are fond of certain jewelry or clothing items, you can even choose what you will wear in advance.

Financial Advisor Christeen Reeg has personal experience with meticulous funeral planning. “When my husband became terminally ill, we were more comfortable talking about plans,” she says. “We selected a burial plot for both of us, and he planned things like service music, scripture, and even what the pallbearers would wear.”

One easy way to get started is to work with your local funeral home to decide what you want. Having a plan ensures your wishes are honored after you are gone.

A few practical questions to consider when you start planning are:

- What are your main concerns when it comes to your funeral?

- How much do you want to spend?

- Do you want to be buried or cremated?

- What would you like to happen to your remains?

- Where will your service be? What is the décor?

- What type of music do you want played?

- Who would you like to be involved in the service?

Keep the Peace

Having a clear plan to follow eliminates a few of the many difficult decisions your loved ones will have to make after you pass. Instead of having to sort through the details of where your service will be, how you will be buried, and what the ceremony will look like, they can simply follow the plan you have left them.

When Reeg’s husband died, she and her extended family viewed his pre-arranged funeral plans as a gift. “We had been married a long time, but we both had children from different families,” says Reeg. “At the time of his passing, we all met together. Not everyone was thinking the same. But I was able, as the surviving spouse, to pull out the document and say, ‘Well, this is what we agreed to and is already paid for. This is what your dad wanted.’ And so we didn’t have any fighting.”

It’s a natural human tendency to avoid the inevitable, and funeral planning can be an emotional process. But planning now reduces emotional flare-ups later. “It’s emotion that drives us, and it drives people to argue and fight,” says Reeg. “The greatest reason that I tell my clients to engage in funeral planning and put their plans in writing is that it’s going to reduce emotional conflict.”

Talking with your loved ones about these plans might feel awkward at first, but you will grow more comfortable discussing the topic over time. And they’ll most likely thank you when the time comes to put your plans in action.

While you don’t necessarily need to share funeral specifics with your family up front, it’s a good idea to disclose the fact that you’ve made plans, who you have left them with, and how to access them when you pass away. “Albeit challenging, openly sharing end-of-life plans can help normalize death and make it feel less scary,” says Guerin. “Grief is never easy, but knowing your loved one’s wishes can be very meaningful and special.”

Planning also helps prevent family members from overspending out of guilt or grief. “For example,” says Reeg, “what if all you want is a basic casket, but when your loved ones are emotional and grieving, they feel guilty and buy the $20,000 one?”

Marta Warren worked in the funeral insurance industry for decades. She says planning is a gift to yourself as well, and it’s never too early to start. “If you believe that you’re going to die at some point in your life,” she says, smiling, “then that’s the time to prearrange. I planned my funeral at a very early age, and I can modify it whenever I want to.”

Leave Plans with an Advocate

For safekeeping, Reeg says, in addition to your children or beneficiaries, it’s best to share your plans with your banker or financial advisor. “They are some of the first people your family will call when you pass,” she says. “I’ve been working with some of my clients for so long. I’ve been there for weddings and other milestones. And I’m there when someone in the family passes.”

Grief Counselor Megan Money says it’s also a good idea to have an appointed family liaison who will execute your plans. “Designate someone in the family who will follow through with your desires,” she says. The person you choose should be someone who will advocate for your plans and be able to separate their own emotions from the process as much as possible.

Warren equates funeral planning with estate planning. “It’s kind of like your will or your trust,” she says. Just as you manage your assets and plan for their distribution after you die, this is another step in the planning process. “When you’re doing your estate planning, it’s one of the things that your financial advisor should bring up.”

Peace of mind is the greatest benefit. “In my case, there was no fighting because all the decisions had been made,” says Reeg. “Making these arrangements in advance is such a gift that you can give your children. It’s so much more than a financial decision.”

If someone shouts at you to “stay out of the kitchen,” it either means they’re cooking a nice meal for you or—more than likely in 2023—you’ve joined the throngs of Americans having a smashing time on the pickleball court.

Pickleball, the whimsically named paddle game, is fast becoming everyone’s favorite addiction, er, pastime. In fact, it’s the fastest-growing sport in the country, with the total number of picklers reaching more than 5 million at the end of 2022—an increase of 40 percent since 2019, according to the Sports and Fitness Industry Association (SFIA).

Lately, pickleball has gotten lots of buzz from famous folks who love the game, including George Clooney, Leonardo DiCaprio, Bill Gates, and Kim Kardashian, and the pandemic-driven need to find outdoor activities didn’t hurt its popularity either.

Football legend Tom Brady is such a fan that, in 2022, he joined a bevy of superstar athlete-investors buying stakes in professional pickleball teams. High-profile names like LeBron James, Kevin Durant, and Maverick Carter are among those funding the expansion of Major League Pickleball (MLP). The budding MLP launched in 2021 with eight teams and has plans to grow to 24, with six professional tournaments scheduled for 2023.

A Mixing Pot

One of pickleball’s defining charms is its ability to bring people of different abilities and ages together for a fast-paced good time. It was this high fun factor that impressed David Damare, a mortgage lender and a former tennis player from Raleigh, North Carolina.

Damare says he has gotten into a habit of playing pickleball two or three times a week when he’s not traveling. He says the sport is silly yet serious, easy yet competitive, and highly accessible for all levels of players from professional athletes to octogenarians.

It’s a winning mix of attributes that draws the crowds. A park in Damare’s area recently converted two tennis courts to eight pickleball courts. Since then, he says, the courts are packed at all hours. “It’s all types of people, from couples in their early 20s and late teens all the way up to literally 80-year-olds that are playing,” he says. “That’s why you have to get there at 7:30 in the morning—because the retirees come at 8:00.”

“It’s a very equalizing type of game. Older and younger people can easily play together, and it can be competitive because you’re not trying to hit the ball as fast [as tennis],” Damare says. “It’s less about power and more about eye-hand coordination, which makes it more open to all ages.”

Once they tried it, Damare and many of his tennis buddies couldn’t stop playing, quickly accumulating a pickleball text group of 30 to 40 guys. “It’s not as hard on your body as tennis, but you do get a pretty good workout,” he says. “The ball is zinging back and forth, so your hand-eye coordination and keeping your head in the game are really imperative.” The community of picklers is welcoming to newcomers, and the mental focus the game requires seems to get people hooked.

Not So Serious

Pickleball hails from the Pacific Northwest. It was invented in 1965 by three friends—Congressman Joel Pritchard, Barney McCallum, and Bill Bell—on Bainbridge Island in Washington State. To entertain their kids, they patched together the first games with an assortment of paddleball, ping-pong, and badminton equipment and played on a badminton court with a hard plastic Wiffle ball.

With their families, they made up silly rules and terminology as they went along and took the name from one of their families’ pet dogs, Pickles.

Although pickleball is mostly a social game that doesn’t take itself too seriously, it can also be intense and competitive. Another thing that makes it highly accessible is that pickleball doesn’t require high levels of strength or athleticism since the 44-by-20-foot courts are much smaller than standard tennis courts. Also, the ball is surprisingly lightweight and is only served underhand, which requires less force.

Pickleball’s kitchen rule sets it apart from other racquet sports. Players get a fault if they step into the 7-foot rectangle next to the net, a zone called the kitchen or the non-volley zone, when volleying, which means hitting the ball without letting it bounce.

When serving, the ball is required to bounce once on the return and then bounce once again when it is hit back to the other side. After that, players can choose either to volley or hit the ball after a bounce. When volleying, they must stay out of the kitchen. Since players can’t play close to the net and keep smashing the ball from there, pickleball becomes more about placing the ball skillfully into intentional zones, rather than hitting it forcefully.

That makes pickleball the rare sport that can put a grandma in her 60s on a level playing field with elite athletes. And that’s not a metaphor—it’s a real-life event.

Last summer, Meg Burkardt, an attorney from Lawrenceville, Pennsylvania, joined a pickup game in the park with three young men she did not know. She could tell they were pickleball beginners and lent one of them her racquet.

After partnering with “the guy in the green shirt” and beating the pants off the other two, she learned that they were T.J. Watt, Minkah Fitzpatrick, and Alex Highsmith of the Pittsburgh Steelers defense. It was the crowd of spectators that had gathered that eventually tipped her off. The funny encounter went viral on social media after Burkardt’s daughter posted that “my mom whooped some Steelers in pickleball today lol.”

“These guys are so fast and so athletic and have really quick hands,” Burkardt told triblive.com. “Each game, they were getting exponentially better.”

Give It a Try

You don’t need much to get started in pickleball, just some paddles, some indoor or outdoor Wiffle balls, and a pickleball court. Any loose-fitting, comfortable clothing will do. Online vendors such as pickleballcentral.com, totalpickleball.com, and Amazon sell many inexpensive wooden or composite racquets that are suitable for beginners.

There are pickleball venues in every state. They’re often located in schools, parks, YMCAs, and community recreation centers. You can easily locate a court in your area by entering your zip code in the appropriate form on USA Pickleball’s places2play.org or by searching the Places2Play mobile app. Its database lists over 38,000 indoor and outdoor courts at nearly 10,000 locations.

The official rules are available online through USA Pickleball, but the best way to learn is just to visit a local court and give it a try. You can connect with potential practice partners by searching “pickleball groups near me” or joining Facebook pickleball groups. Soon enough, you’ll be the one yelling about the kitchen.

Pickleball Patter

A sampling of pickleball terms that may sound silly, but picklers take seriously.

- Kitchen: The non-volley zone, a 7-foot rectangle next to the net on both sides

- Pickled: Losing the game without scoring any points

- Dill ball: A ball in play that has bounced once and is inbounds

- Dink: A soft hit that lands just beyond the net, often in the kitchen

- Flapjack: A shot that must bounce once before it can be hit

- Erne: An advanced and often surprising shot that is hit from outside the court and usually close to the net (pronounced “Ernie”)

- Bert: Same as an Erne but on your partner’s side of the court instead of your own

- Volley llama: Illegally hitting a volley from the kitchen