-

Solutions

- Solutions

- Individuals

-

Retirement Plan Sponsors

- Retirement Plan Sponsors

- Corporations

- Educational Institutions

- Healthcare Organizations

- Nonprofits

- Government Entities

- Endowments & Foundations

- See All Solutions

Comprehensive wealth planning and investment advice, tailored to your unique needs and goals.Investment advisory and co-fiduciary services that help you deliver more effective total retirement solutions.CAPTRUST provides investment, fiduciary, and risk management services for nonprofit organizations. -

About Us

- About Us

- Our People

- Our Story

- Learn About CAPTRUST

-

Locations

-

Resources

- Resources

- Articles

- Podcasts

- Videos

- Webinars

- See All Resources

His days are packed with emotional conversations, prayers, and acts of kindness for patients and their families as they confront all kinds of loss, including serious illness and death.

“Each day, people surprise and inspire me with their courage, their humor, their generosity, their grace, and their love,” O’Neal says. “The work is uplifting.”

He felt called to this ministry after reinventing himself several times during his business career. “Since I was a kid, I have always thought that life is about adventure. I have always been looking for the next adventure,” O’Neal says.

“Being back in the hospital is a kind of coming home for me,” O’Neal says. “I was pre-med as an undergraduate, and I had worked in Washington, D.C.-area hospitals as an orderly and then as a surgical assistant.” When he didn’t get accepted into medical school, he found industrial chemical sales a natural fit. He had success there and was recruited at a young age to be a sales manager in a small company.

Recognizing that business would be his career for a while, he earned a Master of Business Administration degree from the Kenan-Flagler Business School at the University of North Carolina at Chapel Hill. From there, he went to Northern Telecom and then to the American Social Health Association, where he helped get the National AIDS Hotline up and running.

But O’Neal missed his roots in the natural sciences and, after several years, found his way into the environmental consulting field, specifically around ambient air quality. He and his colleagues at a small firm in Chapel Hill guided sections of industry on air quality science, policy, and regulations. Seeking a solid foundation in the field, he went to graduate school and earned a Master of Science degree in environmental science. In his final role before becoming a chaplain, he was a project manager on a hydrological forecasting project in Eastern Europe.

Turning an Avocation into a Vocation

While juggling demanding careers and raising three children with his wife, Janice Whitaker, O’Neal participated in pastoral care work with his church, Christ Episcopal, in downtown Raleigh. One of these pastoral care roles was that of Eucharistic Visitor, where laypeople take the Eucharist to those who are homebound or in the hospital.

“I think I wore the rector out with my unending stories about ‘how powerful this seems, how meaningful it was to me and to those I minister to.’ He suggested I investigate clinical pastoral education (CPE) at one of the local hospitals. I hemmed and hawed for about a year,” O’Neal says.

Finally, he had the opportunity to talk with a veteran hospital supervising chaplain. About 20 minutes into their conversation, she said, “Jesse, you know what your problem is? You are afraid you are going to get into this, and you are going to fall in love with this work. Then, what will you do?”

He accepted the challenge and took his first CPE training at WakeMed during the summer of 2014.

“I did fall in love with the work,” O’Neal says. “I fell hard.” His first internship with WakeMed’s Clinical Pastoral Education Program led to a second and then a yearlong chaplain residency.

The timing was right. His three children were grown, his wife had retired from a successful career as an executive with a pharmaceutical company, and they had saved well.

“Emotionally, I don’t think I could have done this in my 20s or 30s, maybe not even in my 40s or 50s, because I hadn’t accumulated the life experience that supports me in the work,” O’Neal says.

He draws on his project management experience for his new field. “There are lots of ways to be successful as a project manager,” O’Neal says. “My style was to be aware of and invest in the emotional dimensions of the team, hoping to understand what keeps them moving forward and what holds them back,” he says. “Knowing them emotionally was a dimension of that.”

He says, now, instead of caring about people as an adjunct of the work, caring for people is the work.

Like his other endeavors, O’Neal wanted to be sure he was well trained for his new career, so he recently completed his Master of Arts degree in pastoral and spiritual care at the Iliff School of Theology in Denver. Before COVID-19 hit, he traveled to Denver for several days each 10-week quarter for in-person classes. Under COVID-19 restrictions over the past year, all hybrid classes have become completely online.

Finding Those in Need

Every day is unique for a hospital chaplain. O’Neal leans on emergency room nurses, whom he calls “absolute rock stars,” for guidance on where the pastoral needs might be.

He often meets with patients who have had heart attacks, strokes, or other serious illnesses. He also meets with the patients’ families to help them negotiate their feelings as well as hospital procedures.

Once family members arrive, he stays with them. In all these situations, there is loss: loss of function, loss of capabilities, and, sometimes, loss of life, O’Neal says. “My job is to provide the emotional and spiritual support that allows them to initiate their grieving process.”

“When people lose a loved one, their grief can be overwhelming. The reason people grieve is that they had the courage to love as if that love could last forever. I appreciate that courage. And I want to be around people who have that kind of courage,” O’Neal says.

When they’re grieving, they’re coming to terms with the reality that this grief is going to be with them in some form forever, he says. “When you live in a world that has great love, you also live in a world that has great grief.”

Being there is important, O’Neal says. “I cannot ever fully understand the suffering of another human being, the depth and the texture of their suffering,” O’Neal says. “They are on their own unique path through this world. I don’t know what their suffering can or should mean in this journey.”

Although he doesn’t leave anyone’s side during difficult times, he knows it’s a process that people have to go through themselves with the help of their families, friends, and beliefs. “They have to find emotional traction. They have to find something that allows them to get through to the next minute, and the next, and the next,” O’Neal says.

“When our kindred humans, in the face of devastating grief, find that inner resolve that their life can go on, that their life must go on, and gather their family and their love and leave the hospital burdened with grief, but strengthened by hope, this fills me with wonder,” O’Neal says. “I cannot explain it without God.”

Unfortunately, comforting people with physical touch hasn’t been possible this past year because of COVID-19. Everyone keeps the recommended distance, says O’Neal, and hugging has been replaced with elbow bumping.

O’Neal says physical touch is very important, and it can be reassuring to everyone. “I am a hugger, but, during COVID, we try to keep our distance,” he says.

Offering Company to Others

When he has time, O’Neal does what he calls “cold calls,” visiting patients and their families throughout the hospital dealing with less serious conditions.

Sometimes, these visits and conversations last for five minutes. Sometimes, they are an hour long. “I never know where conversations are going,” says O’Neal. “I try to be receptive to where the patient or family wants to go.”

During the visit, O’Neal usually learns something about the person’s faith. “Some people want to immediately open that door and want spiritual and emotional support, and some don’t.”

Often, the conversations lead to a request for prayer. “I do that with great delight. I am in prayer multiple times a day, really continually throughout the day, which is a great joy to me,” O’Neal says.

He lets patients initiate prayer requests. Sometimes, the requests come in as O’Neal is leaving the room and he asks them, “Is there anything else I can do for you today?” They might look at him and look at his badge and say, “Well, you are a chaplain. You could pray for us?”

“I can never predict what people want me to pray about. Sometimes, they’ll ask to pray about healing or good results for a test they’ve had.” But sometimes, their prayer requests catch him by surprise.

In one case, the patient said, “I have been lying here for the last couple hours, and I can see that the people working here are good people. They have been exposed to all kinds of risks in the last year. I want you to pray for them.”

Another patient spent an hour explaining why he was an atheist. As O’Neal was leaving, the patient said, “You’re a chaplain. Aren’t you going to pray for me?”

He did.

Often patients repay him in kind. “I can’t count the times patients have prayed for me and over me,” O’Neal says. “They lift me up with their humor, resiliency, and grace. It would fill up your heart to the breaking point.”

O’Neal has been trained to minister to people of every faith, including those who are Christian, Jewish, Muslim, Buddhist, and Hindu.

One day, early in the pandemic, he stopped to talk to a Hindu woman. She was quietly weeping against a wall in the emergency department because visitation was so constrained. O’Neal asked how he could be of assistance. “Would you pray for me?” she asked.

He told her he knew a little about Hinduism, but he didn’t know how to pray in her faith. She said to him, “You just pray how you pray. That will be enough.”

Giving It All He’s Got

O’Neal is in awe of his medical colleagues. “I feel extremely grateful to be working with rock stars every single day. If you could see what this team is able to accomplish with their clinical skills and their compassion, it would touch your heart,” O’Neal says.

“I believe in the mission of WakeMed,” says O’Neal. “It’s an extraordinary place that began as a community hospital in the 1960s, with a mission of serving all. It has grown and expanded and is regularly mentioned in the same sentence as the well-known university-based hospitals in the area.”

His wife, Janice, says, “Jesse has been successful in various business roles but never as fulfilled as in the chaplaincy work. Each day, he feels that he’s making a difference by helping patients and families, some of whom are experiencing the most difficult times in their lives. “He is a compassionate extrovert who is able to sense what people need and how to help them,” she says. “He loves his work and has found his calling.”

His daughter, Meaghan O’Neal Woodhouse, adds, “If I or one of my loved ones had to be in the emergency department, I would want someone like my dad there to help support us through the process.”

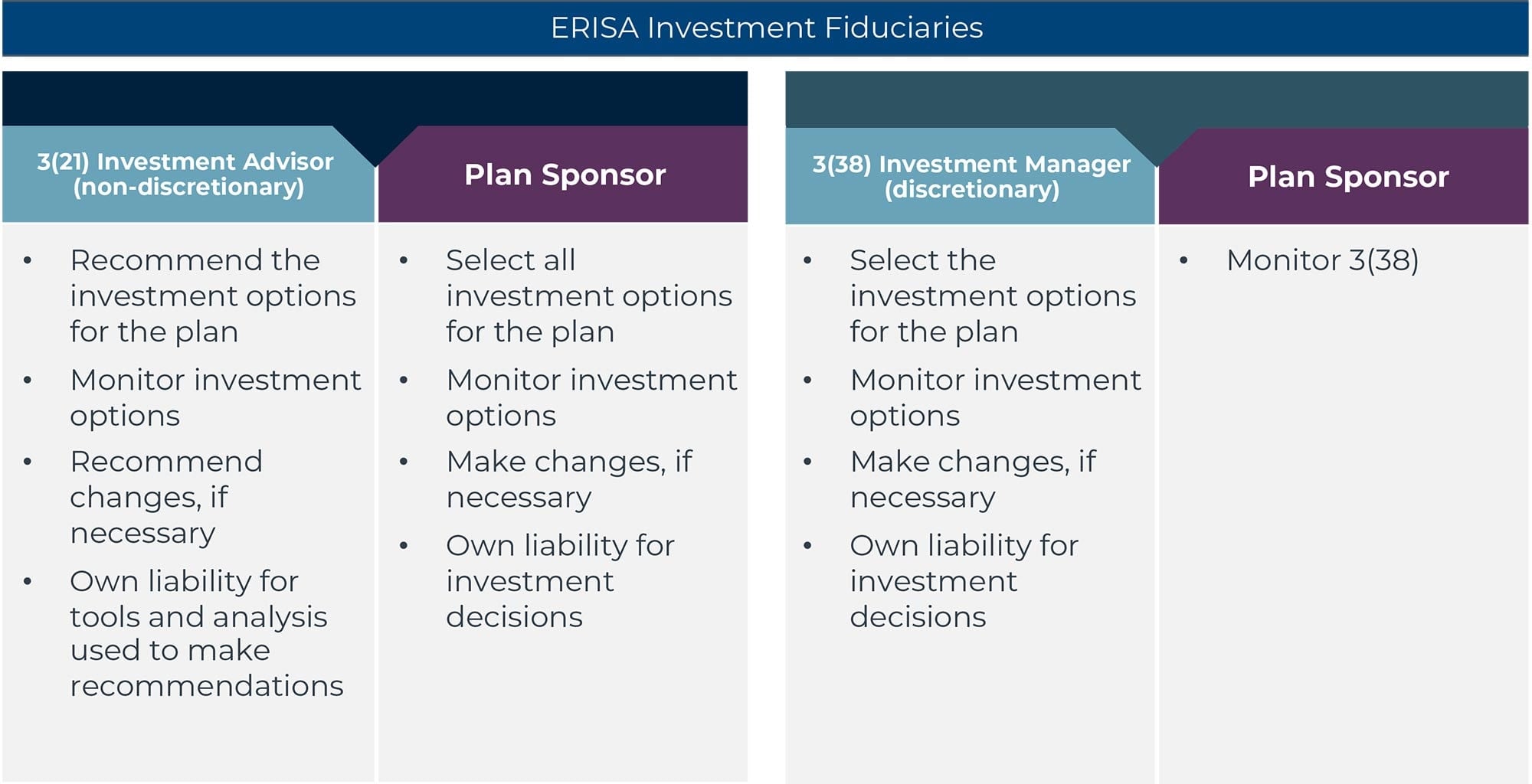

Although similarly named, 3(21) investment advisors and 3(38) investment managers under the Employee Retirement Income Security Act of 1974 (ERISA) are quite different. They provide different services and levels of protection and entail different plan sponsor responsibilities.

ERISA defines a fiduciary as a person involved with plan administration, a person with control over plan assets, or a person who gives investment advice regarding plan assets. Plan sponsors often engage investment advisors to assist with their fiduciary responsibilities if they do not possess the required expertise internally.

When sponsors engage investment advisors to assist with their fiduciary duties, these arrangements are referred to as 3(21) or co-fiduciary engagements. In a 3(21) relationship, the advisor is responsible for investment recommendations made to the plan sponsor, but ultimately the authority to direct assets and the fiduciary responsibility of those investment decisions falls to the plan sponsor.

Alternatively, in a 3(38) engagement, the plan sponsor delegates the decision-making authority regarding investments to the 3(38) investment manager. An appropriately structured 3(38) engagement frees the plan sponsor from the time involved in the selection and monitoring of plan investments and from the liability of those decisions. In a 3(38) arrangement, the plan sponsor’s singular investment-related fiduciary responsibility is the selection and monitoring of the 3(38) investment manager.

Sounds complicated, right? It’s not. Take a look at Figure One, which breaks down 3(21) investment advisor and 3(38) investment manager roles at a high level.

Figure One: Understanding 3(21) Investment Advisors and 3(38) Investment Managers

3(38): Simple and Effective

Many retirement plan sponsors are looking to spend less time on plan investments so they can focus on other aspects of plan management, such as providing participants with the resources they need to help them get in the plan and saving more. One way to do this is by outsourcing investment decision making to a qualified 3(38) investment manager.

But, while hiring a 3(38) investment manager is a simple and effective way to help reduce fiduciary risk, it doesn’t mean all fiduciary duties are eliminated. The process of selecting and engaging a 3(38) investment manager itself is a fiduciary responsibility and comes with some ongoing work. For example, plan sponsors are expected to monitor 3(38) investment managers as they would any other service provider.

“But the thing you monitor is not [the same as] second-guessing their decisions,” says Jenny Eller, chair of Groom Law Group’s Retirement Services Practice Group and Fiduciary Practice. “You monitor their process: Do they continue to have qualified people involved in the process? Do they continue to have the resources they need to engage in their own kind of prudent process?” You don’t get to pick a 3(38) investment manager and set it and forget it, Eller says. “You have to continue to monitor them.”

Unfortunately, it’s not unusual for things to fall through the cracks, even for the most meticulous plan sponsors. But those missteps are avoidable. From understanding what is going to be in or out of scope to making the most of the labor savings plan sponsors hope to recover—in this article, CAPTRUST leans on industry experts to expose some of the most common pitfalls when selecting or working with a 3(38) investment manager and how to avoid them.

Pitfall #1: No Ongoing Formal Monitoring Process

“The law provides a very special benefit for [plan sponsors] who hire a 3(38) investment manager,” Eller says. As long as the plan sponsor has a solid process for selecting and monitoring the 3(38) investment manager, the plan sponsor will not be liable for losses that the 3(38) investment manager causes the plan, she says. Here are a few ways plan sponsors can approach the fiduciary duty of monitoring a 3(38) investment manager’s process.

Keep tabs. “We’re starting to see lawsuits pop up where participants are saying plan sponsors were not paying attention—that a 3(38) investment manager was hired, but the plan sponsor was not asking any questions, or monitoring their process,” Jennifer Doss, senior director of CAPTRUST’s defined contribution practice, says. Maintain a record of your ongoing monitoring process. Take notes. “Because if it’s not documented somewhere, it never happened,” she says. Look for 3(38) investment managers that can provide good documentation for your files.

Ask some hard questions. Plan sponsors should periodically perform due diligence on their 3(38) investment manager. Employers and plan sponsors may want to do a regular request for information (RFI) or questionnaire. This plan sponsor due diligence is intended to verify that there haven’t been any changes to the organization that could affect its ability to fulfill its duties as 3(38) investment manager. This might include changes to its leadership team or ownership and if the firm has, or has not, been subject to a lawsuit or judgement.

Think about the questionnaire as an opportunity to get insight on the firm. Make a point to connect with your 3(38) investment manager on any changes to the investment philosophy of the firm or personnel changes of those making the 3(38) investment decisions for your plan. Experts say plan sponsors may also look to Form ADV for answers—and we’ll get into those details in just a bit. First, let’s talk about the plan sponsors role when contracting with a 3(38) investment manager.

Pitfall #2: Contracting with a 3(38) Investment Manager but Acting in a 3(21) Investment Advisor Capacity

When a plan sponsor engages a 3(38) investment manager, they give up control of the plan’s investment decision-making process. In a defined contribution plan, this means the 3(38) investment manager has full discretion to select, monitor, remove, and replace investment options offered to plan participants. But it’s important that plan committees who utilize a 3(38) investment manager maximize that benefit, Eller says.

Make the most of it. Get the labor savings you intended to get. A 3(38) investment manager is legally required to act in its clients’ best interests when it comes to choosing funds and managing assets. So go do other things! Having someone else manage plan investments allows plan sponsors time to focus on participant engagement, plan design, optimization of other plan vendors—like employee education and financial wellness providers—and overall participant satisfaction or retirement readiness. Don’t squander it.

Don’t forfeit fiduciary protection. Plan sponsor influence over investment decisions comes with potential liability when dealing with ERISA investment management and oversight. “If you hire a 3(38) [investment manager] and then push them out of the way and make the decisions anyway, you have lost all benefits of appointing [the 3(38) investment manager],” Eller says. For example, if the 3(38) investment manager allows the plan sponsor to remain heavily involved in the investment decisions for the plan—whether that is suggesting or influencing the funds in the plan lineup—there is a risk that the plan sponsor loses the fiduciary protection that hiring the 3(38) investment manager is meant to provide.

“It can be difficult for some plan sponsors to pass the reins,” Doss says. Some want to retain the ultimate decision about which funds should be offered, which isn’t possible in a true 3(38) relationship.

Pitfall #3: Allowing Room for Guesswork or Interpretation

The details of a 3(38) investment manager relationship are not something to leave to chance, so do your homework.

Ask about any potential conflicts of interest. One best practice is to make sure your 3(38) investment manager discloses all sources of revenue related to the relationship, says Martha Tejera, founder of Tejera & Associates, a consulting firm helping employers meet their fiduciary responsibility in the selection of their retirement plan providers and advisors.

Integrity is also important, Tejera says. “An issue I just recently came across is fund managers paying for [or] providing training for registered investment advisors.” Providing completely objective advice to clients is paramount for 3(38) investment managers, Tejera says. For example, find out if the 3(38) investment manager receives gifts of any kind from the vendors and companies they do business with. This includes pay-to-play arrangements, sponsorships of company events, lunches and dinners, or trips from vendors the 3(38) investment manager does business with.

Obtain and investigate disclosure of any litigation. Tejera says one of the most important documents to check is Form ADV. This free disclosure document reveals everything from an advisor’s fee structure and firm history to its management style and any misconduct. You can get a copy of Form ADV through the 3(38) investment manager’s website or on the Investment Adviser Public Disclosure website at adviserinfo.sec.gov. You can also check state regulator websites where the advisor operates.

Get the details in writing. If you are engaging a 3(38) investment manager, they must acknowledge their fiduciary status in writing to you. A written contract between a plan sponsor and a 3(38) investment manager with a defined set of services is a way to ensure the agreed-to terms of the relationship are upheld and that the right parties are receiving proper fiduciary protection. Written documents can also serve as legal evidence in court, if necessary.

Pitfall #4: Assuming All 3(38) Investment Manager Services Are Equal

3(38) investment manager services can vary widely from one service provider to another, and it’s the plan sponsor’s responsibility to get into the weeds to understand what is in scope and what is not in scope, Doss says.

Get specific. “If plan sponsors just assume, ‘I’m asking for 3(38) investment manager services and I’m going to get the same package with different 3(38) investment managers,’ they’re wrong,” Doss says. Plan sponsors should review the definitions of actual services offered and “Get the details in writing about what the 3(38) investment manager is going to take discretion over and what functions remain a plan sponsor responsibility,” she says.

Drill into the details with the provider: Find out how they are going to make the most out of your time as a plan sponsor. For example, does the 3(38) investment manager tailor investment recommendations to fit each plan, or does the plan have to transition to a defined menu of investments? If the 3(38) investment manager offers custom or proprietary funds, will they be included in the lineup?

Most 3(38) investment managers will assume full responsibility for selecting and monitoring plan investments, including your qualified default investment alternative (QDIA). Find out if this work will be in scope. Which party will define asset classes used for the plan’s investment menu? Which party will define what type of share classes or investment vehicles are used? Moreover, does the plan have self-directed brokerage accounts or company stock, and how will those be handled? Think about all the individual components of your plan. You’ll want to know what is in scope and what is out of scope.

Look at potential changes. While some 3(38) investment managers take discretion over current plan lineups, others will opt for a complete revamp of the plan’s current fund menu, Doss says. Keep in mind that any changes made to the plan will need to be communicated to plan participants, so consider the time, effort, coordination, printing, and postage costs involved with that.

“Implementation could mean a complete lineup overhaul—or it could mean absolutely nothing, but it’s important to understand exactly how much change is required and what will need to be managed by the plan sponsor,” Doss says.

Plan sponsors can take simple steps that can lead to a happy and healthy retirement savings plan if they avoid the common pitfalls described above. A well-structured 3(38) investment manager agreement can facilitate fiduciary risk transfer and create labor savings that will allow employers to focus on more meaningful things for their participants. While it requires some homework up front and a little management along the way, the payoff in hiring a 3(38) investment manager can definitely be worth it.

NOTE: Information on this page has been updated as of August 2024.

Today’s 401(k) industry has grown to more than 60 million participants, $3 trillion in participant assets, and a whopping $30 billion in annual fees, according to the Plan Sponsor Council of America. With numbers like this, it should come as no surprise that the way plan sponsors assess their service provider fees is receiving a lot of attention.

In this article, we’ll explore three key options for retirement plan sponsors that are considering how service provider expenses will be paid by participants. Each option has its own potential benefits and considerations. The three most common approaches include:

- A built-in method whereby provider costs are covered through revenue sharing;

- An institutional method in which participants are assessed a flat fee and revenue sharing is removed from the investment lineup; and

- A fee-leveling method whereby revenue sharing is credited to each participant and a flat fee is assessed.

Let’s take a deeper dive into each.

Built-In Method

The built-in fee allocation model uses fund revenue—known as revenue sharing—to pay for recordkeeping fees. Revenue sharing consists of 12(b)-1 and sub-transfer agency fees built into the expense ratios of a plan’s investments. These fees are collected by the investment managers, paid to the recordkeeper, and used to offset plan expenses, typically for recordkeeping fees. In this fee allocation method, the total fund revenue is collected by the service provider and aggregated at the plan level.

The total amount of revenue sharing in a plan is often enough to cover the entire recordkeeping fee. If not, the recordkeeper charges an additional fee to cover the gap. When revenue sharing exceeds the amount owed to a recordkeeper, the surplus can be used to cover other qualified plan expenses or rebated to participant accounts.

The benefit of this method is it’s easy to implement and reduces, or even eliminates the need for explicit participant fee charges. Additionally, the net investment cost of the funds may be overall lower than when non-revenue sharing share classes are utilized. However, it may be harder to hit a specific revenue target since each investment option’s revenue sharing amount will vary from fund to fund.

Institutional Method

Another method for covering recordkeeping fees is to offer a menu of institutional share class funds that do not pay revenue sharing and charge each participant a dollar or basis-point amount. The recordkeeper deducts the amount from each participant’s account either annually or quarterly. The fee is stated clearly on participant statements and in fee disclosures. This approach is straightforward to implement, transparent, and easy to explain to participants.

While simple in execution, the institutional method can be met with some challenges. The most common issue occurs when a fund company does not offer a share class without revenue sharing, resulting in a fund lineup with some funds that pay revenue sharing and others that do not. In this scenario, plan sponsors must decide where the received revenue will go and how it will be used to offset service provider fees.

Fee-Leveling Method

Fee leveling is an allocation approach that rebates any revenue sharing back to the participants who paid the fees. Typically, this revenue is distributed on a monthly or a quarterly basis. Then, each participant is assessed a dollar or basis-point amount for the services provided.

In another version of the fee-leveling method, the recordkeeper assesses a fee or rebates revenue at the individual fund level for each participant. If the investment has exactly the required revenue amount in revenue sharing built into its expense ratio—let’s say 0.20 percent or 20 basis points as an example—no additional fees or rebates are needed.

If revenue sharing in the fund exceeds required revenue—for instance, 0.25 percent or 25 basis points—the recordkeeper credits each participant who has assets in the fund with the amount of the excess. In our example, the revenue sharing would exceed required revenue by 0.05 percent, resulting in a 5 basis-point credit returned to participants. Meanwhile, if the fund provides less than the required revenue amount, the recordkeeper would add a billed fee in the amount of the shortfall to the accounts of each participant using the investment.

The benefit of either of these fee-leveling approaches is that the plan sponsor can combine the use of both revenue sharing funds and institutional classes to arrive at the best net cost lineup. The drawback is that each service provider offers its own accounting methodologies based on its system’s capabilities for fee-leveling, which can make a difference in how fees get allocated back and how often. Additionally, lots of debits and credits on each fund within participant accounts can create investor confusion.

Plan Sponsor Considerations

Each methodology has its own potential advantages and considerations. There is no single correct approach to fee allocation. In most cases, philosophical perspectives will drive an organization’s fee allocation decision. Plan sponsors should speak with their advisors about which fee allocation model might make the most sense for their organization. Contemplating a consistent approach to pay for fees can assist fiduciaries in fulfilling their plan oversight responsibilities while providing continuity in future decision-making.

Legal Notice

This material is intended to be informational only and does not constitute legal, accounting, or tax advice. Please consult the appropriate legal, accounting, or tax advisor if you require such advice. The opinions expressed in this report are subject to change without notice. This material has been prepared or is distributed solely for informational purposes. It may not apply to all investors or all situations and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. The information and statistics in this report are from sources believed to be reliable but are not guaranteed by CAPTRUST Financial Advisors to be accurate or complete. All publication rights reserved. None of the material in this publication may be reproduced in any form without the express written permission of CAPTRUST: 919.870.6822.

With only 50 percent of Americans having access to a workplace retirement plan, the Setting Every Community Up for Retirement Enhancement (SECURE) Act included reforms meant to broaden retirement plan coverage. The Act passed in 2019, but many key provisions are only now taking effect. One example is the pooled employer plan (PEP) provision. One of the most hyped elements of the Act, some say PEPs may become the dominant retirement plan type within the next ten years.

But do PEPs live up to the hype? What about similar SECURE Act provisions that created group of plans (GoP) and enhanced existing multiple employer plans (MEPs)? Let’s take a closer look at all three types to understand which—if any—plan type is poised for long-term success.

What are PEPs?

Pooled employer plans, also known as PEPs, allow unrelated employers that meet certain requirements to band together to participate in a single retirement plan, sponsored by a pooled plan provider (PPP). A PPP can be any entity that registers as such with the Department of Labor (DOL) and the Internal Revenue Service (IRS). Recordkeepers, third-party administrators, payroll providers, and registered investment advisors are the parties most likely to sponsor a PEP.

The idea is that employers in a PEP can take advantage of their collective purchasing power to potentially obtain lower fees and more comprehensive services. And by offloading certain nonfiduciary responsibilities to a third party, an employer’s administrative burden is reduced.

Employers that are not currently sponsoring retirement plans may make strong candidates for PEPs. Plan sponsors that already offer single-employer plans may find PEPs less attractive. This is because the ability to customize is limited. Plan sponsors interested in joining a PEP should fully understand the costs and restrictions associated with the plan, and the responsibilities of all parties involved. Currently 403(b) and governmental 457(b) plans are not permitted to participate in PEPs.

What are MEPs?

Multiple employer plans, or MEPs, allow related businesses to join together to participate in a single retirement plan. Unlike PEPs, MEPs can only be sponsored by certain entities related to the employers. The SECURE Act made MEPs easier to establish by eliminating the unified plan rule, also known as the one-bad-apple rule, which stated that compliance failures of one employer could disqualify the entire plan. Additionally, smaller MEPs (and PEPs), with fewer than 1,000 participants, are now exempt from a potentially expensive audit requirement, if no one employer exceeds 100 participants.

Many of the same benefits and considerations associated with a PEP also apply to a MEP and MEPs will most likely appeal to the same types of employers.

What are GoPs?

The SECURE Act also established a plan type called a group of plans, or GoP, where employers—whether unrelated or related—can file a single IRS Form 5500 for multiple defined contribution plans. A GoP must have the same trustee, administrator, fiduciaries, investments, and plan year. Unlike PEPs or MEPs, GoPs are not single plans, but do allow a single Form 5500 filing, which can reduce cost. Unfortunately, for plan sponsors looking to adopt a GoP, the audit exception for smaller MEPs and PEPs does not currently apply.

Where Do We Go from Here?

For plan sponsors of smaller retirement plans, the expansion and creation of these arrangements is beneficial but may not be a cure-all. For existing MEPs, the SECURE Act provides an opportunity to band together to create a super-PEP, which might dramatically lower fees and enhance services for participating employers.

However, MEPs existed prior to the SECURE Act without widespread adoption. Since they are primarily used by small employers with limited options this makes it difficult for the MEPs to accumulate assets quickly. For example, the average size of an employer plan inside a MEP is under $1 million. Generally, the threshold for price concessions is close to $100 million—a level to which most MEPs never come close. This lack of scale makes it difficult to obtain the type of purchasing power to deliver on the promise of lower fees and enhanced services. Despite the efforts of the SECURE Act to broaden these arrangements, it does not address this fundamental issue of scale, which will likely prevent MEPs and PEPs from becoming a retirement plan industry game-changer.

In practice, GoPs may be the most successful arrangement in the long-term since they alleviate the administrative burden of filing Form 5500. However, retirement plan sponsors need to wait until regulations are issued around filing a single Form 5500 for multiple defined contribution plans. Also, while PEPs and the new rules for MEPs are effective in 2021, the GoP provision is not effective until the 2022 plan year.

The DOL is also expected to provide additional guidance clarifying roles and responsibilities of each party involved with a PEP, including whether a PPP can delegate nonfiduciary administrative responsibilities to a third party, and regulations on PPPs satisfying multiple roles in a PEP—such as being both the PPP and 3(38) investment manager.

The SECURE Act’s expansion of MEPs and creation of PEPs and GoPs may not be a panacea for smaller employers, but these changes are a positive step toward providing Americans greater access to retirement plan benefits.

A glaring regulatory hole in recent years has been the lack of guidance from the Department of Labor (DOL) on the emerging issue of cybersecurity, despite some high-profile cases of theft from participant retirement plan accounts. However, that changed on April 14, when the DOL issued guidance on best practices for maintaining cybersecurity, including tips on how to protect participants’ retirement benefits.

The guidance comes as somewhat of a surprise, as it was not expected until later in the year and the new DOL secretary was only recently confirmed. However, it follows a March 15 report from the Government Accountability Office (GAO) that urged the DOL to expedite its timeline.

Following are some highlights from the DOL guidance:

- The DOL’s service provider review suggestions range from the obvious—such as confirming that the provider is properly insured against participant account theft and asking about the provider’s information security standards—to the more comprehensive—such as inquiring about past security breaches and the provider’s response to them, along with seeking contractual confirmation of the plan sponsor’s notification timeframe in the event of a breach. Though the DOL has communicated these as Tips for Hiring a Service Provider, plan sponsors should review the provisions with existing service providers that maintain plan records and participant data to confirm safeguards are in place.

- The DOL provides a 12-part menu of cybersecurity best practices for plan service providers, which includes implementing a formal and documented cybersecurity program, ensuring that assets or data stored in a cloud or managed by a third party are subject to independent security reviews and assessments, and encrypting sensitive data.

- The DOL provides tips for participants to help protect their own data and dollars, such as registering online accounts, regularly checking account status, using strong and unique passwords, avoiding free Wi-Fi, and reviewing information on identifying and avoiding phishing attacks. Plan sponsors should consider communicating these tips to their participants on a regular basis.

The guidance is concise and practical, offering a variety of best practices. Plan fiduciaries should pay special attention to this guidance and act accordingly to prevent cybersecurity breaches and theft from their retirement plans.

Vendor consolidation has become a common theme in the defined contribution industry. Over the past decade, the universe of retirement plan recordkeepers has been reduced from 400 to approximately 150—and this trend shows no sign of slowing.

This shifting industry landscape means that many retirement plan sponsors have had to endure a transition they were not expecting. What are the considerations for plan sponsors caught in the recordkeeper consolidation shuffle?

The Reasons Behind Vendor Consolidation

While all consolidations are different, the primary driver is scale. Larger scale equates to more profits to invest back into the organization. Today’s recordkeeping business requires significant investment in technology. For vendors that have not achieved enough scale, partnering with another organization may make sense to ensure viability.

Many of the recordkeepers that are no longer in the market were not predominantly focused on recordkeeping services. The retirement plan space has also experienced significant fee compression over the past several years. Because of this, vendors where recordkeeping is an ancillary business may find that it is no longer profitable, and through the divestiture of recordkeeping, they can instead focus on their primary business line (e.g., banking, insurance, asset management, etc.).

It is important to note that not all vendors consolidate due to negative reasons. For those recordkeepers looking to access new markets or services, partnering with another company may help advance their cause. Regardless of the reason, vendor consolidation is a trend that is unlikely to disappear in the near future.

Plan Sponsor Considerations

For plan sponsors faced with a consolidation, there are some key lessons to be aware of. First, consolidation timelines can vary widely—from as little as two months to as long as 18 months. Understanding the timeline, particularly in terms of key dates for paperwork—such as opt-in and opt-out deadlines—is imperative. Additionally, realizing the participant communication cadence is also important to prepare for questions and the integration of any additional communication campaigns.

Plan sponsors should also be aware of the potential for blackout periods following a recordkeeper consolidation, which can result in transaction restrictions, like delays in loans and disbursements. These periods are typically shorter during consolidations than they are following a traditional conversion (i.e., recordkeeping change due to a request for proposal, or RFP); however, it is important to understand the length and timing of the blackout period.

For plan sponsors, there are fiduciary considerations regardless of whether the recordkeeper is the acquiree or the acquiror. For those plans where the recordkeeper is the acquiree, plan sponsors should exercise the same degree of fiduciary due diligence in determining whether to remain with the new recordkeeper as was taken to select the existing recordkeeper. For plans where the recordkeeper is the acquiror, plan sponsors should verify that the acquisition will not impact the recordkeeper’s ability to provide best-in-class service. This could a particular area of concern for larger consolidations.

Using the consolidation as a catalyst to conduct a recordkeeper RFP may be a smart consideration for plan sponsors, particularly those where several years have passed since the last search was conducted. There is no better way to ensure recordkeeping value while documenting fiduciary due diligence process than by conducting an RFP.

Ultimately, it is important for plan sponsors to fully understand the process and potential impact recordkeeper consolidations may have on the plan and its participants.

While consolidations may be challenging to navigate, they can also result in benefits such as technology improvements, additional services, or even lowered fees as the result of a RFP. Due to the continued presence of marketplace drivers, plan sponsors can expect that recordkeeper consolidation will continue.

To learn more about vendor consolidation, click here to view a recording of our recent webinar on the topic.

The American Rescue Plan Act (ARP) of 2021 contains approximately $1.9 trillion worth of fiscal stimulus intended to address issues resulting from the COVID-19 pandemic. While the ARP contains a variety of fiscal stimulus measures, this summary focuses on the provisions impacting multiemployer and single-employer retirement plans. It is not intended to be a detailed analysis of the comprehensive measures contained in the ARP.

Multiemployer Plan Funding Relief Measures

Subtitle H—Pensions: Sections 9701 – 9704 and a new ERISA Section 4262

All multiemployer plans are characterized by an economic risk zone of red, yellow, or green. When plans are characterized in the yellow (endangered and seriously endangered) and red (critical) zones, current law requires certain remediation actions such as funding improvement or rehabilitation plans. The ARP provides relief by temporarily delaying the designation for those in the yellow and red zones, delaying certain participant notices and other requirements. Additionally, the ARP provides an optional and temporary five-year extension of the funding improvement and rehabilitation periods for plans in endangered or critical status.

The most significant provision for multiemployer plans creates a Special Financial Assistance Program for financially troubled plans. This legislation allows for funds from the general fund of the Treasury to be transferred into a special fund in the Pension Benefit Guaranty Corporation (PBGC) at the direction of the Secretary of the Treasury and the director of the PBGC. These funds will provide financial assistance to multiemployer pension plans in danger of insolvency (critical and declining), subject to certain provisions. Those plans will not be required to repay this financial assistance. For potentially impacted plans, the ARP contains further detailed provisions, which should be reviewed to ensure appropriate utilization of the relief measures provided.

Finally, the ARP includes adjustments to the funding standard account rules detailed in the legislation.

Multiemployer plan sponsors should work with their actuaries to determine the appropriateness of available temporary relief provisions offered under the ARP. Additionally, plan sponsors with plans characterized as critical and declining should consult with professionals to determine their eligibility in the Special Financial Assistance Program.

Single-Employer Funding Relief Measures

Subtitle H—Pensions: Sections 9705 – 9706

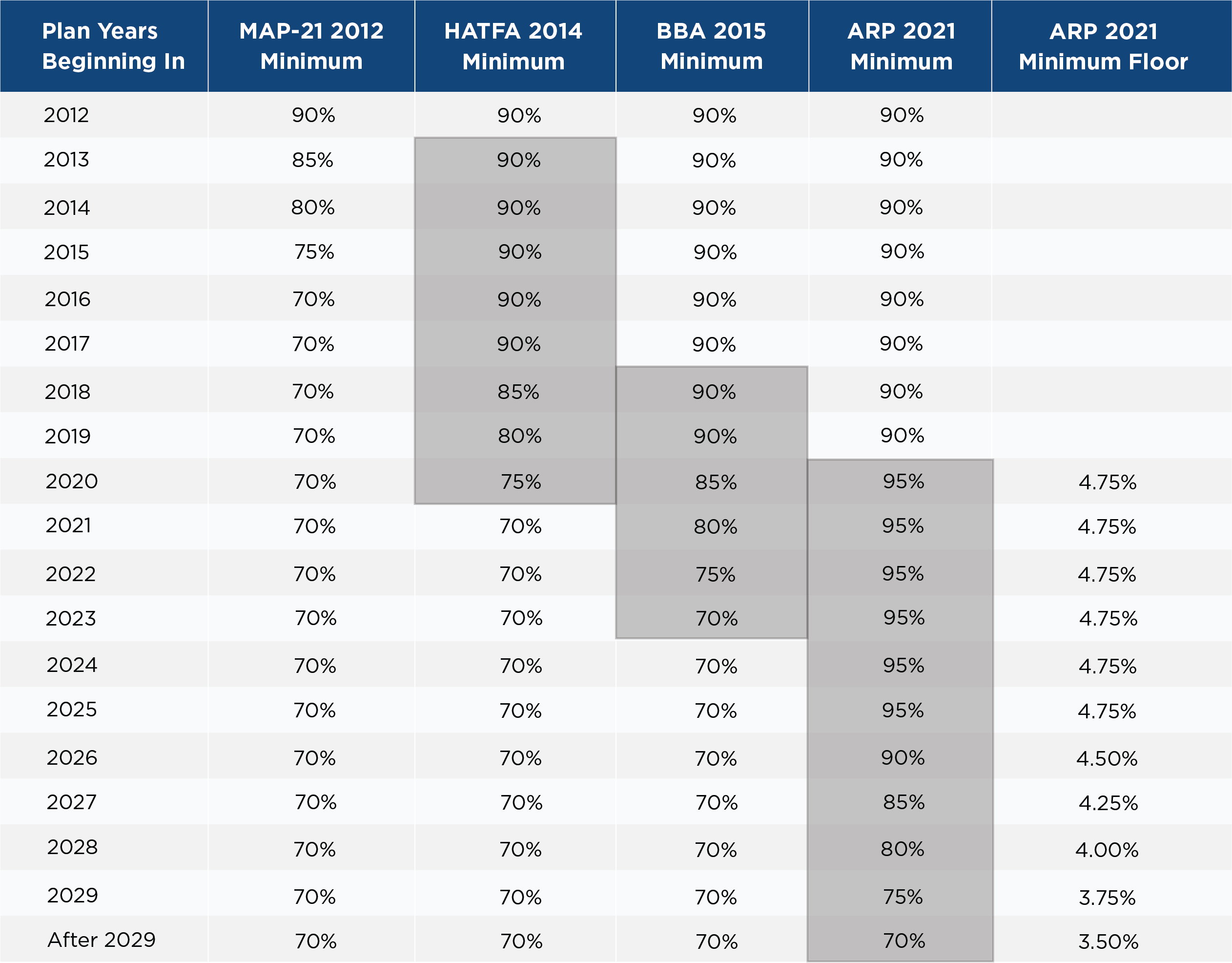

Corporate pension plan sponsors must estimate their defined benefit pension plan’s funded status on a regular basis to determine if they possess adequate assets to meet the benefit obligations promised to participants and determine minimum required contributions. To provide this estimate, actuaries determine the present value of future benefit payments, or the liability (in today’s dollars) for comparison to current assets. Actuaries discount future payments by an assumed interest rate often referred to as the discount rate. When this discount rate is higher, the present value of liabilities is lower, and vice versa.

The ARP eliminates any existing shortfall amortization basis for historical years preceding the 2022 plan year. This effectively provides plan sponsors a clean slate; prior shortfalls will not be factored into minimum required contribution calculations. It also increases the current seven-year amortization schedule to 15 years, which will reduce minimum required contributions in the coming years. Plan sponsors may elect to apply this fresh start to shortfall amortizations to an earlier plan year, specifically 2019, 2020, or 2021.

Previous legislation allowed actuaries to shift from using a two-year average of interest rates based on maturity to allowing the use of a corridor around 25-year averages. Essentially, actuaries reference the two-year average of interest rates at a given maturity. If that number is below the corridor relative to the 25-year average, as shown in Figure One, actuaries use the minimum rate, which is defined as a percentage of the 25-year average.

The ARP essentially extends the minimum corridor provisions of several previous Acts, including MAP-21 2012, HATFA 2014, and BBA 2015, which prescribe the use of higher historical interest rates, higher funding ratios, and therefore lower minimum required contributions.

Figure One: Minimum Corridor Percentage Applied to the 25-Year Average Discount Rate*

*If the two-year average discount rate is below the 25-year average under current and previous legislation, which Is also subject to an absolute minimum under ARP.

Source: CAPTRUST Research

Lastly, the ARP creates a minimum deemed 25-year average discount rate, which essentially creates an absolute interest rate floor, as noted in Figure One.

Plan sponsors should work with their actuaries to determine the implications of these new rules on minimum funding requirements. While this legislation will create more flexibility in funding strategies, we encourage plan sponsors to consider a defined funding policy based on their specific objectives. Ultimately, plan sponsors will need to determine the appropriate balance between contributing to their plans to shore up funding and investing in their core businesses and operations as allowed by the law.

As always, we continue to monitor the legislative and regulatory landscape. We look forward to assisting you in evaluating the implications to your organization.

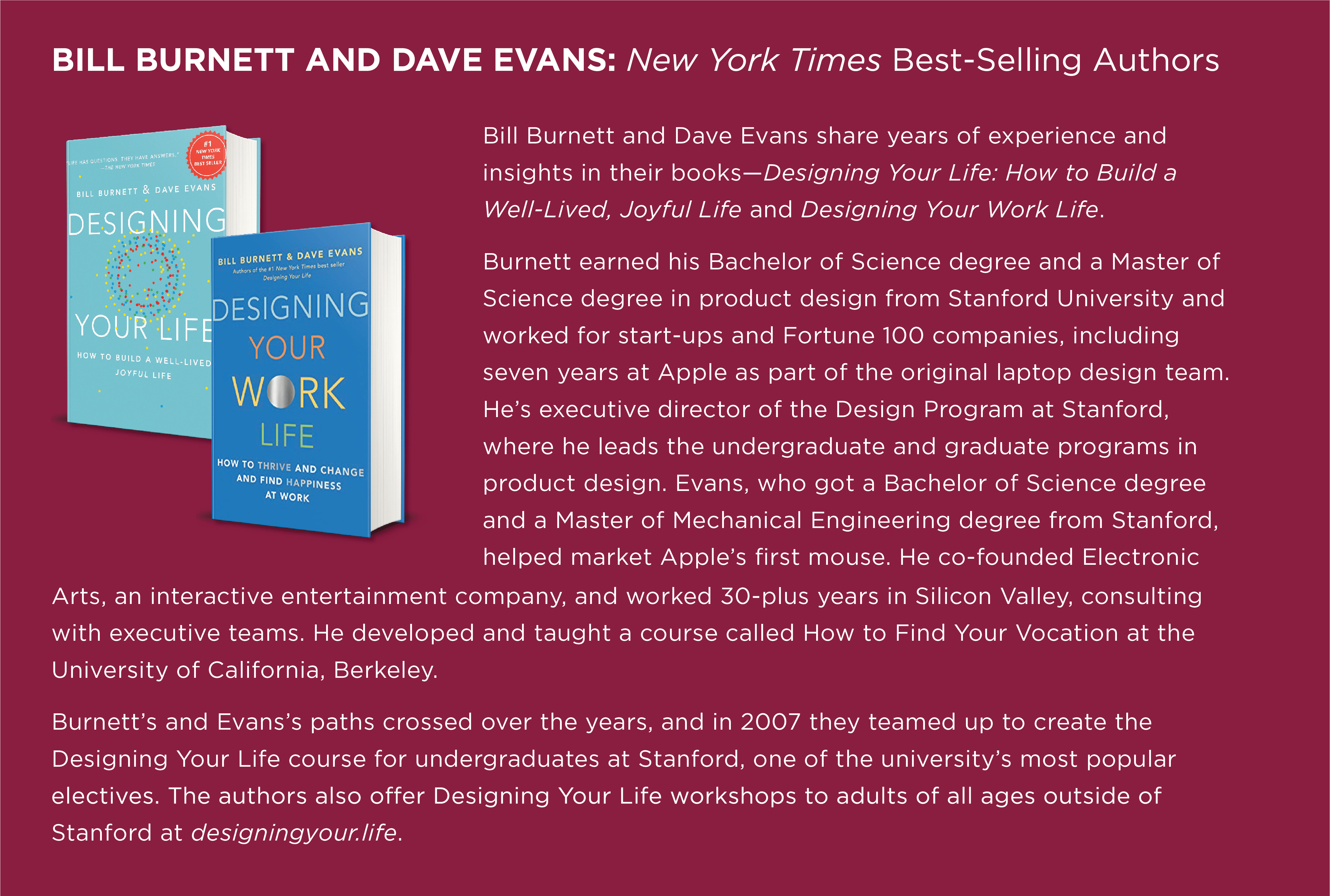

“I’m going to repurpose my time doing things that I find meaningful,” says Burnett, a product designer, who with Dave Evans wrote the bestselling book Designing Your Life: How to Build a Well-Lived, Joyful Life.

The authors, both Silicon Valley veterans who worked on creative teams for Apple, developed Stanford’s Designing Your Life course, as well as workshops for people retooling their careers, considering encore professions, and planning for retirement.

Burnett is applying the same design thinking he used to create the latest technology and products to prepare for the next phase of his life.

“Designers think differently than other people,” says Burnett, executive director of the Design Program at Stanford, where he oversees the undergraduate and graduate product design programs. They approach problems with curiosity, reframe dysfunctional beliefs that hinder creativity, prototype ideas to figure out what works, and form radical collaborations with others.

“People can use these design tools as they move from the money-making phase of their lives to the meaning-making phase,” he says.

Too often busy professionals don’t give enough thought to retirement, finding themselves adrift after leaving careers, Burnett says. “At work, they have a social network, status, a role they play in the organization. The day after they leave that job, they are just somebody sitting in a Starbucks drinking a coffee. It’s pretty jarring for people who haven’t prepared for it or designed for the change.”

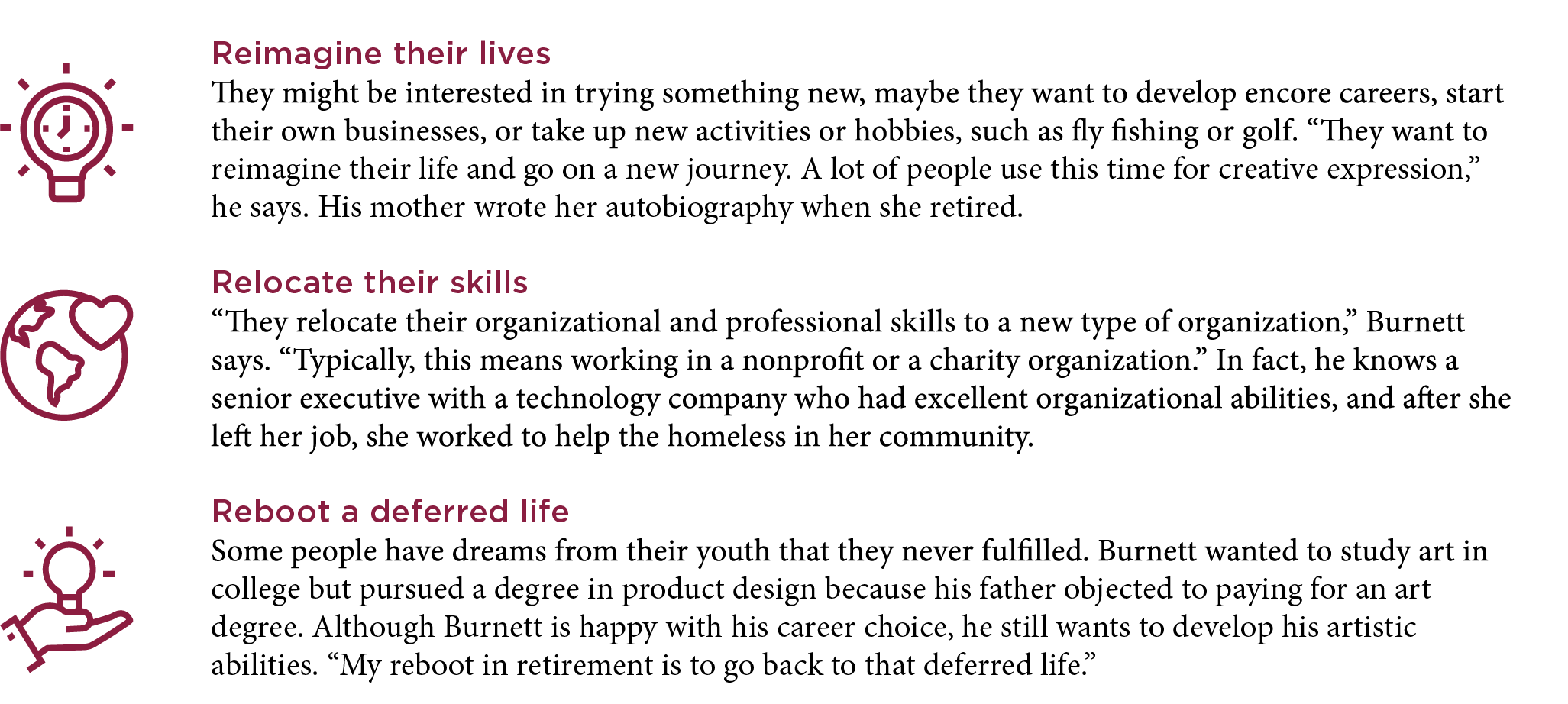

Burnett says people preparing for retirement often use one of three strategies:

All these strategies require designing your way forward, he says.

Explore New Ideas

To begin the process, many people must overcome the fear of leaving their job, which often provides them with their identity, routine, and relationships, says Kathy Davies, managing director of the Life Design Lab at Stanford. The teaching lab runs the university’s Designing Your Life classes, develops the life design curriculum, and trains other universities to teach life design.

One key to making this leap is using your curiosity to explore several ideas, Davies says. “People need to reframe the dysfunctional belief that there is just one good direction in retirement. There are many.”

To help you get started, the Stanford experts suggest that you:

- Write a short reflection of 250 to 500 words about your future. This is a general statement of what you consider good and worthwhile in work, where work is not necessarily a paid endeavor but how you use your time and energy to accomplish things in your life and community, Davies says.

- Write another 250 to 500 words about your view of life. These are your critical defining values—what matters most to you, the meaning and purpose of your life, and how spirituality, family, where you live, and the rest of the world fit into your life.

- Review your statements and see where your views complement each other and where they clash.

These two views are your compass for your life and future.

Outline Your Plans

Burnett suggests developing three Odyssey Plans for yourself. Keep a journal and write down the times you feel energized about your life. Consider what you would do in retirement if you didn’t have to worry about money or the possibility of someone laughing at you for doing it.

Create three wildly different five-year timelines filled with activities you might pursue. Developing these three future visions helps people brainstorm ideas for their future, he says.

Maybe you want to become a bartender in Belize or a clown in Cirque du Soleil, Burnett says. “We are not encouraging you to sell the house and join the circus. We’re telling you to let your imagination go for a while.”

Davies says having several routes to explore can open new possibilities and set you free from perfectionist tendencies that could limit you.

Test Your Ideas

After you have plans, prototype some of your ideas, Burnett says. One of the easiest ways to do that is to talk to someone who is living the type of lifestyle you’re considering.

Testing your plan requires a small investment of time and can lead to a big payoff in the long run, Davies says. “The magic of prototyping is that instead of sitting around and talking about your plan, you do something. You get out of your head and into the world to try things.”

Davies worked with a retired couple who planned to become what they called silver-haired gypsies by selling their home and touring the U.S. in an RV. They tried it out for a week and found they loved RV life but didn’t like all the driving, so they decided to take occasional trips and maintain a home base.

People sometimes pay a high price for not prototyping an encore career. One example is a woman who left her job in human resources for a large corporation to fulfill her dream of opening a small Italian deli and café. She renovated the space and launched her business. Her café was successful, but she was miserable. She didn’t enjoy hiring staff, tracking inventory, and ordering stock.

The former human resources professional could have avoided a costly mistake by interviewing small café owners, bussing tables at an Italian deli, or working for a catering business. Eventually, she sold her business and went into designing restaurant interiors, which was her favorite part of opening the café.

Burnett suggests giving yourself time to make the transition into retirement. Some people take at least a year’s sabbatical after they leave their jobs before they try something new. He has a friend who retired from his career as a venture capitalist, a lucrative but stressful job. He told Burnett, “I plan to take three years to ride my bicycle and read books because I don’t want to make a decision about the future with a burned-out brain.”

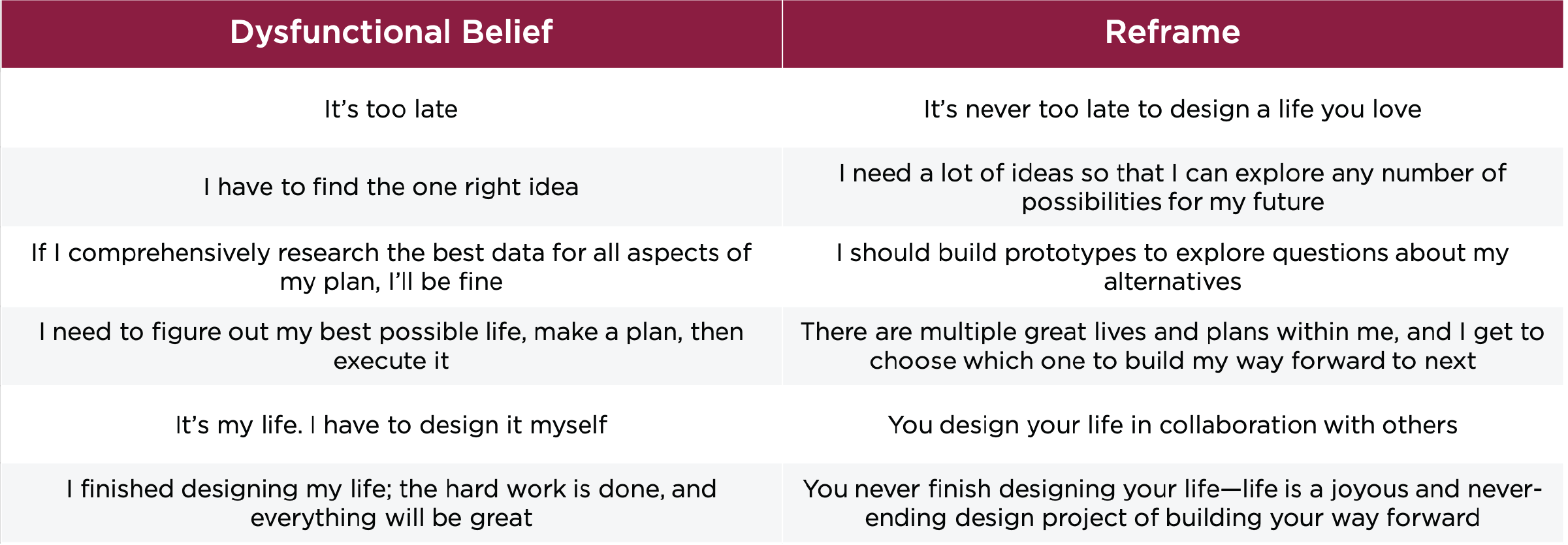

Reframe Your Dysfunctional Beliefs

One of the keys to a well-designed life in retirement is reframing some of your dysfunctional beliefs to create a better life for yourself. Here are some examples, according to Designing Your Life: How to Build a Well-Lived, Joyful Life:

Ask for Help

No matter what your retirement plan is, it’s important to form radical collaborations, Davies says. Talk to your spouse and other people who have retired or are considering it, she says. Get input from people who have different perspectives.

Davies says one woman she worked with created three Odyssey Plans for retirement but didn’t know if her husband would be supportive of some of her more creative ideas. It wasn’t until he also outlined some plans, and they shared ideas, that they both fully appreciated one another’s dreams and began working on plans together. Their lists created lively conversations that helped them prepare for the next stage of their lives.

Burnett has been talking to his wife and others about the future, as well as prototyping some of his ideas. Eventually, he’s going to step back from some of his administrative roles but wants to continue to teach. “I love teaching, I love writing, and I love art.”

He is prototyping his future life with a small art studio down the street from his home. He plans to write a book on designing your life for retirement, and he has other creative projects he’s discussing with potential collaborators.

“I am going to spend the next 10 or 20 years doing something interesting,” he says. “I’d like to hang out more with artists and musicians. I’ve got at least two more lives in me.”

It’s that passion for the acoustic guitar industry that helped him steer the family-owned business through good times and bad for the past 34 years.

Martin, 65, is playing his swan song this summer, retiring as chief executive officer of Martin Guitar, as well as finishing his tenure as chair of the National Association of Music Merchants (NAMM).

His retirement will mark the end of six generations of Martin men running the 187-year-old Nazareth, Pennsylvania-based company, whose guitars have been played by Elvis Presley, Johnny Cash, Hank Williams, Paul McCartney, Eric Clapton, and Gene Autry.

Martin wanted to exit on a high note. “I have been talking about retirement for at least five years. My father retired under duress, and my grandfather forgot to retire,” he says. His father left the business after making some unsuccessful business decisions, while his grandfather ran the company until his death at age 91.

Martin Guitar’s board was “hoping I would work for the next 100 years. I knew I would get pushback about the decision. People said, ‘Are you sure? Don’t you want to wait a year?’ But I thought, ‘I don’t know what I’m waiting for.’”

He wants to focus on his family and health. He is receiving treatment for bladder cancer, and his wife, Diane, is being treated for breast cancer. He says they’re both thankful for the excellent medical care they’re receiving. “It’s the journey Diane and I are on now, and we want to prolong that journey because we have a teenage daughter.”

The company, which also makes guitar strings and ukuleles, is searching for a new leader, and for now, someone outside his family will run the business. But one day, another C. F. Martin, Martin’s daughter, Claire Frances, 16, might want to take over.

Martin has been talking to her about inheriting the business. “I told her, ‘You don’t have to run it, but you have to manage the people who run it. You are going to own it. You are going to have the opportunity to be chairman of the board.’”

In the meantime, he’ll remain chairman and assume a new role as executive chairman, working far fewer hours but still representing the company.

When the pandemic has subsided, he plans to travel to trade shows, distributors, and guitar stores around the world to share the company’s history. “People get a big kick out of me telling the story about my family business,” he says. “It’s not a video. It’s not a salesman telling the story. It’s a Martin telling the story.”

Learning the Business

What a story it is.

Martin’s great-great-great-grandfather was German-born Christian Frederick Martin, the son of a cabinet maker who apprenticed with a renowned guitar maker. He immigrated to the U.S. in 1833 and founded the business.

“For whatever reason, God bless him, C. F. Martin learned how to make guitars, and he decided to make great ones,” Martin says.

Chris Martin IV’s path to CEO took several twists and turns. His mother and father divorced when he was three, and he lived with his mother in New Jersey, but he visited his grandparents, C. F. Martin III and Daisy, in Nazareth during the summer. “I would go to work with my grandfather and pack guitar strings and move wood around in the shop,” he says. “I never got to use a tool, but I got to be around the tools. That was my first exposure to the shop.”

During the summer between high school and college, he worked in the shop. “I followed a guitar through the guitar-making process and gained tremendous respect for my colleagues who do the work. I learned I’m a klutz when it comes to doing woodworking.”

He also didn’t have an affinity for playing the instrument. “I took guitar lessons as a kid,” he says, “but I didn’t click with the teacher, so I never learned to play, which is okay, because I am surrounded by great guitar players.”

After graduating in 1978 from Boston University with a bachelor’s degree in business, Martin joined the family business full-time.

His father, Frank Herbert Martin, struggled toward the end of his tenure as president of the company, so he retired, and his grandfather, C. F. Martin III, assumed control again. “My father and I had a bit of an estranged relationship,” Martin admits. “My grandfather saw my interest in the company and was a great mentor to me.”

His grandfather named him vice president of marketing in 1985. “It was a way for him to say to everyone else, ‘Chris is sticking around, and I want to give him a title that gives him a little bit of heft,”’ Martin says.

After his grandfather died in 1986, Martin was named chairman of the board and chief executive officer. He was 31 and scared to death. He didn’t consider himself a natural leader, and he faced several obstacles. “My father left a whole cadre of mostly male appointees his age who were looking at me a bit skeptically,” Martin says.

Another obstacle: At the time, the acoustic guitar industry was floundering. “Business was terrible,” Martin admits. “We went from making 23,000 guitars a year in the 1970s to 3,000 a year in the early 1980s. And we had some quality issues. It was little stuff that we needed to address.”

However, Martin’s vision and entrepreneurial spirit turned the business around, says Jackie Renner, president of Martin Guitar. “When the company had quality issues in the 1980s, he brought his manufacturing colleagues together and said, ‘What do we have to do to make this company vibrant again?’ The answer was focusing on the musician and making the highest-quality instruments possible,” Renner says.

Evolving Over Time

As the quality issues were resolved, something else happened to turn things around: MTV Unplugged made its debut in 1989, and by the early 1990s, the phone started ringing off the hook, Martin says.

“MTV recognized how cool the acoustic guitar was and promoted it to an audience that was a little jaded,” he says. “It didn’t start out wildly successful for us, but pretty soon, the momentum was building, and people said, ‘I have to get an acoustic guitar like the one Eric Clapton played on MTV.’ We paid attention at the time, and we got very lucky.”

Clapton was a fan of the guitar, saying, “If I could choose what to come back as, it would be a Martin OM-45.”

Martin built on that momentum by starting the Signature Series guitar line, featuring instruments played by acclaimed musicians such as Johnny Cash and Gene Autry.

“If you are famous and you agree to do an artist’s model, we will give you a guitar, and you can buy a few for your friends and family,” Martin says. “Then we give some of the proceeds from the other guitars we sell in that line to the artist’s favorite charity.”

The company has made 175 signature models since it launched the series in 1993.

During his time as CEO, Martin began profit sharing with his employees, offering college tuition reimbursement, and working on sustainability issues. “We use rare exotic timbers—rosewood, ebony, mahogany—for our products,” he explains. “We are trying to find a way to make the supply chain more sustainable.”

Renner says Martin has nurtured the culture of Martin Guitar, which employs about 1,000 people in its two factories—one in Nazareth and the other in Navojoa, Mexico. “He introduces himself to all of our new employees in Nazareth and takes them on a tour of our guitar museum to hear a little more about his family history. Chris is incredibly energetic, passionate, and committed to Martin Guitar,” she says.

Continuing to Contribute

As Martin winds down his role as CEO, he looks forward to what’s next and to reallocating his time to other causes. The first thing he wants to do in retirement is to take a breather. “I want to do nothing,” he says. “I’m test-driving that idea now during COVID.”

After the pandemic, he and his wife plan to travel more, and he wants to build a kit car, a Caterham, in his garage. “A bunch of crates will be arriving soon at my house from England. This kit is relatively simple. You hear stories that people buy a kit car, and it never gets done. I don’t want that to be me. With the help of some friends, I think I can get it on the road.”

Attorney Chuck Peischl, a longtime friend and a member of the company’s board, says he’s glad that Martin will assume the role of executive chairman. “He really is Mr. Martin, just like his grandfather before him. He was the personification of the company, and Chris is in that same image mold.”

“One time, I asked Chris what he would be if he wasn’t CEO of Martin Guitar, and, without missing a beat, he said, ‘a philanthropist,’” Peischl says. He expects Martin will spend more time serving as chairman of the Martin Guitar Charitable Foundation, which gives money to charities in the community, such as food banks, as well as nonprofit music, arts, education, and environmental action organizations.

Martin says he’s grateful for his career in the music industry. “People are passionate about being part of this industry. Once people join it, they never leave it.”

But he’s especially grateful to have served as head of a company in which both employees and customers value a guitar that’s as good as it can be.

It’s a good thing we have collective names for these houseguests. After all, there are about 100 trillion of them, mostly bacteria, in our digestive systems alone. And they are not all alike: Hundreds of species live in the average colon. So, while you don’t need to get to know them individually, you should probably think of them more than you do, health experts say.

These microbes “have a very symbiotic relationship with us,” says Sonya Angelone, a registered dietitian in San Francisco and a spokesperson for the Academy of Nutrition and Dietetics. “We need them for good health. And they need us. They’re like pets, only smaller.”

And, like pets, the microbes in our guts are forced, for good and ill, to adjust to our lifestyle choices. When we choose apples over cheeseburgers and brisk walks over sofa time, our microbes, in their own way, notice. They repay us for healthier choices in ways that scientists are just beginning to understand.

It now appears that these microbes play key roles in regulating the immune system and may affect a long list of conditions, including obesity, diabetes, heart disease, and, of course, disturbances in the digestive system itself. The mix of microbes in your gut might even influence your appetite and your mood.

“We think about our gut health as just about our gut, but it rules the rest of our body,” says Jill Nussinow, a registered dietitian in Santa Rosa, California, who has written several books on vegan cooking. “When something is good for your gut, it’s good for you.”

But what is good for your gut or, more specifically, the bugs that live there? Some of the answers may surprise you.

Diversity Is Good

Like fingerprints, no two gut microbiomes are the same. Your gut is different from your neighbor’s, and intriguingly, the guts of people from different cultures around the world tend to be quite different from one another. That genetic variation has allowed scientists to study the associations between certain microbial patterns and differences in lifestyle and health.

One key finding: People with greater diversity in their gut microbiomes—a higher number of species—tend, on average, to be healthier. While cause-and-effect relationships have not been established, lower diversity has been found in people with conditions including inflammatory bowel disease, type 2 diabetes, psoriatic arthritis, eczema, and cardiovascular disease. Some studies have found a link between obesity and low gut diversity; others have not.

Another key finding: Western diets, high in fat and processed foods, are associated with lower gut diversity than are diets higher in plants and whole foods.

“We are a long way from being able to clearly describe what is a healthy microbiota, and there are likely many pathways to [it],” says Wendy Dahl, an associate professor of nutritional sciences at the University of Florida. But, she says, “It’s generally thought that high diversity is good and low diversity is maybe not.”

The reason diversity might matter, she and other experts say, is that the microbes in our guts are down there doing important work. And they are specialists: Think of a hard-hat crew that includes the equivalent of carpenters, roofers, plumbers, bulldozer operators, and the like. Now imagine that each of these groups prefers a different diet, but you are delivering food that only the bulldozer guys will eat. Pretty soon, the rest of the crew all but disappears, and you’ve got a leaky roof, rusted pipes, and crumbling walls.

And some of the microbes left behind may be real troublemakers—bugs that prefer eating the lining of your gut to eating whatever food you send down. That may be a pathway to a condition sometimes called leaky gut, in which microbes and food particles escape the gut, potentially triggering inflammation, not only in the digestive system but throughout the body.

The good news about a messed-up microbiota? “You can change it,” Nussinow says.

Feed Your Friends

When most Americans think about eating better for gut health, they probably think about probiotics—beneficial microbes found in or added to fermented foods or supplements. Potential sources include some yogurts, sourdough bread, sauerkraut, kombucha teas, kefir (cultured milk), Japanese miso (a soybean paste), and Korean kimchi (a vegetable mix typically served as a condiment or side dish). All contain live microorganisms that might have some beneficial effects. In some circles, fermented foods have become trendy, with aficionados exchanging home fermentation recipes and getting together for festivals and impromptu kraut mobs.

Nutrition educators say these foods can play a role in day-to-day gut wellness. But they are not the secret to long-term microbial bliss. Among the reasons: The microbes in foods (or supplements) do not all survive the digestive process, and even when they do, they do not take up permanent residence in your gut. They are, at best, friendly visitors. There’s also the question of whether the particular bacteria in any batch of sauerkraut or carton of yogurt happens to be what your gut needs that day.

But there is one kind of food that experts agree is good for every gut, every day—and it’s something woefully lacking in most American diets: good old-fashioned fiber.

“In the past, we thought that all fiber was good for was to relieve constipation and, in the case of soluble fiber—like that found in oatmeal—lower your cholesterol,” Angelone says.

But now, she and other experts say, fiber is known to be the most important food source for the microbes in our colons that produce the most benefits. These microbes have evolved to make use of food remnants that travel through the upper digestive tract largely intact—the hard-to-digest fibers in fruits, vegetables, whole grains, beans, and nuts.

The average American adult gets just 17 grams of fiber each day, instead of the recommended 25 to 35 grams, recent research shows. That’s the result of a diet with too few whole, unprocessed foods, Dahl says.

“Probably the biggest problem with our ultra-processed diet is that we are starving our microbes,” she says. That’s the root cause of our often-underpopulated guts, she adds.

And the answer, according to Dahl, is not to load up on fiber supplements or any one food. It turns out that different beneficial microbes feed on different kinds of fiber. So, “a diverse, fiber-containing diet is going to support diverse microbes,” she says.

Details, Details

That’s not to say that all foods with fiber are created equal. Some foods are particularly rich in so-called prebiotics, substances known to feed beneficial microbes. The list includes onions, garlic, leeks, jicama, asparagus, and Jerusalem artichokes.

Another kind of fiber with special benefits is resistant starch. Unlike starches that are digested quickly, raising blood glucose levels, these are starches that arrive undigested in your colon, where they feed some especially helpful microbes. Sources include plantains, green bananas, white beans, lentils, and whole grains such as oats and barley.

Resistant starch also can be created in your kitchen from a few foods that might surprise some healthy eaters: potatoes, rice, and pasta. The secret is that you have to cool these foods after cooking them to produce high levels of resistant starch. You can then eat them cold or reheated. In practical terms, that means leaving cooked rice, potatoes, or pasta in the refrigerator overnight before enjoying them, Angelone says.

Lifestyle Factors

A healthy gut is about more than what you eat. It’s also about what you do.

One big factor: exercise. Regular exercisers tend to have healthier guts with higher counts of bacteria thought to fight inflammation. It’s unclear why. Exercise may be especially important in establishing the microbiome in childhood. And it might be one way for older adults to stave off age-related declines in microbe diversity.

Another factor: stress. Stress hormones can disrupt gut microbes in ways that promote inflammation. Stress-eating can also wreak havoc, of course.

And then there are antibiotics. Antibiotics are meant to kill harmful bacteria, but often kill helpful strains too. The gut fallout—which can range from brief bouts of diarrhea to life-threatening infections with drug-resistant bacteria—is a good reason to avoid these medications except when needed.

The bottom line: There’s a lot you can do to nurture a healthy gut. Start with a varied fiber-rich diet. Sprinkle in foods containing probiotics that might help keep digestive microbes in balance. Consider supplements only in consultation with your doctor. Get or stay active. And do what you can to avoid and manage stress. Be good to your gut and your gut will be good to you.