-

Solutions

- Solutions

- Individuals

-

Retirement Plan Sponsors

- Retirement Plan Sponsors

- Corporations

- Educational Institutions

- Healthcare Organizations

- Nonprofits

- Government Entities

- Endowments & Foundations

- See All Solutions

Comprehensive wealth planning and investment advice, tailored to your unique needs and goals.Investment advisory and co-fiduciary services that help you deliver more effective total retirement solutions.CAPTRUST provides investment, fiduciary, and risk management services for nonprofit organizations. -

About Us

- About Us

- Our People

- Our Story

- Learn About CAPTRUST

-

Locations

-

Resources

- Resources

- Articles

- Podcasts

- Videos

- Webinars

- See All Resources

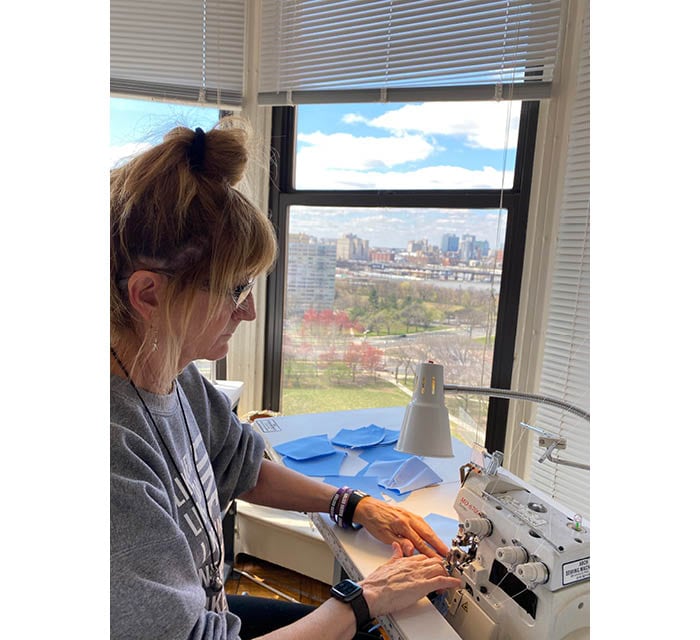

At 64, she made history as the oldest contestant ever on the show, which features up-and-coming designers, mostly in their 20s and 30s.

Yet Beringer herself was an up-and-coming designer.

Rewind just seven years, and you would find a 58-year-old Beringer behind a desk for her 18th year at the New Jersey Education Association.

It had been a good journey for a good mission. The association promotes excellence and equity in public schools and colleges across the state. Beringer helped drive that cause in many roles, from advocacy to program development, communications, and outreach.

She had recently married, gotten a much-sought-after promotion, and enjoyed a financially secure life. However, that coveted promotion landed her in an ill-fitting realm. Throughout her career, her roles had always had a creative component; now, she was managing people.

Her creative side was stifled. “I felt like my oxygen was being siphoned off when I was at work,” said Beringer. “I felt like I was suffocating.” It was time for a change.

That Aha Moment

Beringer remembers the exact moment she made the life-altering decision. “It was three in the morning, and I wasn’t sleeping again because I was not happy with my job.”

Inspired by her sons’ successes as young college grads following their dreams, she felt a twinge of envy and asked herself, “If I was young again, what would I want to learn?”

“It was a simple question, but that question changed my life. I had that aha moment. It was fashion design,” says Beringer.

She had learned to sew at age 12 and enjoyed vintage and thrift store shopping to create her own distinctive looks. But she had no other fashion experience, and her degree was in business education. So, this was a bold leap into new territory.

With encouragement from her husband and sons, Beringer left her education career at the top of her game and enrolled in a three-year Master of Science program in fashion design at Drexel University’s Westphal College of Media Arts & Design.

“I loved it,” says Beringer. “Once I got to Drexel, I felt like I found my home,” she says. “I felt like this is where I belonged, and most times, I forgot that I looked different than my classmates.” Beringer even came to see the humor in frequently being mistaken for the professor.

She was having the time of her life, but it wasn’t an easy path. The intensive program consumed 70 or 80 hours a week, often more. She had little time for anything else and was coping with the onset of painful arthritis. Ultimately, Beringer graduated at the top of her class, with a 4.0 grade point average and a record-setting seven awards at the 2016 Drexel Fashion Show.

And, while many of her classmates went to New York or Los Angeles to apprentice with other designers after graduation, Beringer didn’t have the luxury of time. She immediately started designing under her own label out of her Philadelphia studio.

Joan Shepp’s Window

For nearly 50 years, Joan Shepp in Philadelphia has been a premier fashion destination. The store is known for its collection of creative European, Japanese, and hard-to-find designers.

Beringer recalls that during her time at Drexel, it was always “‘You’ve got to see Joan Shepp’s new window.’ They are pieces of art.”

Recognized as one of the country’s style leaders by publications such as Harper’s Bazaar and Departures, the store welcomed fashion students and encouraged them to explore the collections. “It is just an iconic place; I thought of it as a research lab, and that’s where I would always go.”

Beringer’s first sale was at Joan Shepp. “I remember it well because the woman came out of the dressing room in the Dior-inspired skirt and just started twirling and got teary-eyed. She said, ‘I haven’t felt this beautiful in years.’ That’s when it really hit me how the power of fashion goes beyond the aesthetics; it goes into how you feel inside your heart and soul.”

I remember it well because the woman came out of the dressing room in the Dior-inspired skirt and just started twirling and got teary-eyed. She said, ‘I haven’t felt this beautiful in years.’ That’s when it really hit me how the power of fashion goes beyond the aesthetics; it goes into how you feel inside your heart and soul.

Nancy Beringer

Beringer started freelancing with Joan Shepp and designing those window displays, including one featuring her 2016 collection of evening wear. “This was in my first year out of fashion school. It was such an honor to be able to offer some of my work at her store.”

One garment in the Joan Shepp window would catapult Beringer’s new career to the next level.

Beringer poses with one of her futuristic fluid designs

Beringer poses with her mentees from the Refugee Women’s Textile Initiative

Mistake Gone Magic

Beringer was designing for a runway benefit based on a progressive dark-to-bright theme, symbolic of the emergence from substance abuse. A rainbow-colored swath of faux fur beckoned. A cape, perhaps? The organizers asked for something more dramatic—one of her sweeping, oversized Rosa coats.

“So, I designed this big coat,” says Beringer. “The funny thing is when I cut the first piece, I made a mistake. I cut it upside down.” Beringer goes on to explain.

“Picture your hair as we’re sitting here; it’s just flat. If I hold you upside down, [your hair would be] fighting gravity, and that’s what this faux fur did. So that mistake was the magic of the coat.”

After the charity show, the coat went into the window at Joan Shepp, where it was spotted by Philadelphia-based musical artist Tierra Whack. The 22-year-old star was looking for something to wear on the red carpet at the 61st Annual Grammy Awards. As soon as she saw the coat, she said, “That’s it.”

Beringer and Whack struck up a friendship on social media. “I wanted her to know the back story—that it represented empowering and helping women,” says Beringer.

Whack was enchanted by the coat. When she shared the news of her nomination for a Grammy for best music video, Beringer asked the artist to come to her studio in Philadelphia. When Whack stepped out of the car, “it was like a lightning bolt,” says Beringer, “a creative explosion. We had this instant connection.”

What followed was a whirlwind of preparations. One fitting, then another, and Whack leaves for Los Angeles before deciding on shoes. The coat will have to be hemmed on location.

In Los Angeles, Beringer finds herself at a private party with Whack’s entourage. “I look around the room and I realize I’m the oldest person in the room, designing for the coolest person in the room. Lucky me.” The coat and its wearer were a sensation on Grammy night.

“As a designer of evening wear,” says Beringer, “you fantasize of designing something for the red carpet, but what was important to me was that I had the trust of this genius artist in this big moment of her life.”

The next day’s New York Times featured three looks. The Technicolor Coat was one of them. Adding to the notoriety, E! named the ensemble one of the night’s most outrageous outfits. The coat earned Beringer a Best in Philly fashion design award.

As the Grammy event was going on, Beringer was invited to be a featured designer for Philly Fashion Week. A few months later, Philadelphia Magazine named her Best in Philly Fashion Designer for Artsy Dresses.

A Gift and an Opportunity

Beringer first saw Bravo’s Project Runway 10 years earlier. She harbored a secret, unspoken desire to be a contestant, vying to become the next great American designer. She didn’t even tell her Drexel classmates, thinking they might scorn reality television.

As a fresh Drexel graduate, she applied to be on the show. After making it to the second selection—the callback in New York—she was cut from the cast. But she didn’t take the rejection personally.

When I didn’t make it to the final stage, I viewed it as a gift and an opportunity, because I had affirmation from the judges and former contestants that my work was good enough to be on the show.

Nancy Beringer

“When I didn’t make it to the final stage, I viewed it as a gift and an opportunity, because I had affirmation from the judges and former contestants that my work was good enough to be on the show.”

Beringer viewed it as having another year to improve her craft. She took an intense online draping class out of Paris, a two-week patternmaking class in London, and couture classes.

In 2019, she made it onto the show. Sixteen designers showcased their talents in weekly challenges, with experiments directing them to use animal prints and thrift shop clothes, even taking a shot at designing the tuxedo of the future.

Beringer won the episode 11 challenge, which paired the designers with Olympic and Paralympic athletes to create a victory night celebration outfit. Beringer worked with Tatyana McFadden, a Russian-American athlete who has won 17 Paralympic medals in wheelchair track and field. Beringer wowed the judges with a silver ensemble: a feather bustier with fantasy skirt that doubles as a cape.

Week after week, Beringer kept up with the frenetic energy of the show and its time-constrained challenges, rising to the final four contestants by the last week. “That whole time, I felt it was my destiny,” she says.

Beringer’s on-air effervescence belied the personal physical challenges. “I’m 65 now, and I wake up in pain every day, but, because I’m active in designing, I feel better throughout the day,” she says.

Her Project Runway final collection featured futuristic, metallic, and fluid designs. A sculptural cut-out jumpsuit. A printed, tailored pantsuit. Shimmering dresses in liquid-look fabrics that danced in the runway lights.

The looks are eclectic, often androgynous and fantastical. “I don’t have a checkbox of ‘I design for this particular clientele or this look.’ It’s really a journey of exploration with my fabric, and I’m just delighted when it finds the right person to wear it, that it makes them feel empowered and gives them a sense of joy.”

Beringer finished as a runner-up and earned high praise from the judges, who admitted they had initially underestimated her. “I didn’t get the title. I didn’t get the money, which would have been really nice, but I did walk away as the winner because I left it all out there.”

Beringer chose the 10 models for her final collection to represent diversity and inclusion. “When we brought the models together for their first fitting, they looked around at each other, and they all got it,” says Beringer. “They saw that we were making a moment. They felt it.”

Dali Wearable Art Coat and Bottoms

This magical Wearable Art Coat is a tribute to Spanish surrealist painter Salvador Dali, displaying his most well-known pieces.

Fast-Forward to 2020

Life in pandemic days is quieter, with travel and shows on hold. The Joan Shepp store is temporarily closed. Beringer is self-quarantining in her studio, working 12 or more hours a day, seven days a week, on her craft. She avoids the news as much as possible.

When the world emerges from this forced pause, Beringer will be ready with unexpected new designs born out of the colorful chaos of her studio. She is where she is meant to be. “I found out fashion designing is not something I want to do; it’s something I need to do. It is pure oxygen for me.”

Alone in her studio, she will pick up fabrics, drape them over dress forms, transform them with novel techniques, and immerse herself in the joyous journey of letting the materials say what they want to be.

“I have this creative outlet. I can bring empowerment and joy to people, and I can also use my platform to give back and help make the world a little better. I just hope I am inspiring people to see that no matter what their challenge, age, or situation, it’s OK to hope, persevere, and pursue their dream.”

Four Keys to Following Your Dream

Feather Your Nest Egg. In making the career shift, Beringer was walking away from financial security. “But I could do it because of how financially conservative

I had been all along. I led a life that allowed me to follow this dream.” From her first job out of high school, making $100 a week, Beringer still set aside savings, then faithfully maxed out 401(k) contributions, invested, and minimized debt.

Rejoice in the Process. In today’s world, we are accustomed to instant gratification, information, and results, says Beringer. Everything is so immediate, right there. “It doesn’t always happen the first time or the second. My professional background easily translated into an understanding that design is a process.”

Be Fearless. Beringer is all about pushing the boundaries. “When working on a design or experimenting on a fabric, I’m like, ‘I’ll try it.’ What’s the worst that can happen? When you look at what’s happening in the world right now, whether or not it works or I need to start over, that’s not really significant.”

Don’t Wait for the Perfect Time. Had she waited until she was ready to be a red-carpet designer, that moment would have never arrived, says Beringer.

“I seem to be drawn to jobs I don’t know how to do,” she says with a laugh. “It’s OK to not know how to do something. Ask questions. Embrace the unknown. Embrace the learning and find your own joy.”

Q: I have inherited jewelry and collectibles from family members over the years. Are they covered under my homeowner’s policy?

It depends. Typically, insurance carriers don’t assume you have expensive items or rare collections. If you have valuable jewelry, a coin collection, furs, or a room full of expensive guitars, it might be worth getting extra coverage to insure them. You don’t want to find out too late that your policy doesn’t cover them.

Start by understanding what your homeowner’s policy includes and how much coverage is in place to ensure your items are going to be covered in the event of a claim. Know what situations the policy does cover: fire, theft, accidental breakage, water damage, and damage while traveling, for example. And be sure to understand what your responsibilities are under the policy requirements, such as storing your collection under certain conditions like out of direct sunlight, in a temperature-controlled room, or in a dry space.

If the value of your items exceeds the limits on your policy, you can increase your coverage by purchasing either an endorsement or floater. You can also purchase a standalone policy designed to cover specific valuables, such as a collection of expensive handbags or couture clothing.

Your insurer will require you to have a professional appraisal to obtain additional coverage for your valuables. The appraisal establishes an objective value for your property, which may be significantly different from what you think it’s worth. And remember that you’re adding premium for the endorsement on top of what you’re paying on your regular homeowner’s insurance policy.

If you’re interested in such a standalone policy, talk with the insurance professional from whom you purchased your homeowner’s policy. That’s the best place to start. You may also be able to save money by insuring your valuable items with the same company that carries your auto, life, or homeowner’s insurance.

When you’re confident that you’ve purchased the proper coverage at a good price, then it’s time to go enjoy your possessions with the peace of mind that comes from being well-protected.

Q: I want to go live in a warmer state. What do I need to think about from a tax perspective?

Moving to another state for the weather, greater access to the outdoors, or to be closer to loved ones is a big life decision—one that will impact the taxes you pay no matter where you land.

But to make a good decision, it’s important to consider all the taxes that can apply to a state resident. In fact, it’s possible you could pay higher or lower property taxes, income taxes, or sales taxes when you move. How much you’ll pay depends on the individual state’s laws:

- Property taxes. Many states, such as Nevada and Florida, that don’t have income taxes make up for them with property taxes. These spots draw a lot of retirees, but it’s important to consider that they have relatively high property taxes. Some states offer property tax relief programs for older individuals or those with limited income or disabilities. If you’re set on moving to a high property tax state like Texas or California, consider renting as a cheaper alternative to owning a home.

- Income taxes. Many states’ income tax rates range between 1 percent and 10 percent. Some states have no income tax. In Tennessee, for example, regular income is generally not subject to state tax, but a flat tax rate applies to dividends and interest income. Income tax rates will affect different forms of retirement income, as well, such as Social Security, retirement accounts, and other investments. New Mexico and West Virginia are two of the 13 states in the country that apply taxes to Social Security benefits.

- Sales taxes. Thirty-eight states have local sales taxes that can vary widely. A state with a moderate statewide sales tax rate like Louisiana and Alabama could actually have a very high combined state and local rate compared to other states.

Paying attention to tax efficiencies can help you stretch your savings; however, these implications are just one piece of the bigger picture.

It’s important to get an accurate analysis of the true cost of living in your desired location. In addition to state and local taxes, get familiar with the day-to-day life and expenses in the areas you are interested in moving to, such as transportation, groceries, access to good health care, and cultural resources. While it’s important to consider taxes, deciding to move solely based on this factor might have you missing the bigger picture.

Moving to another state can save you money if you plan ahead to maximize all available benefits. Just be sure to consider all the implications before you start packing those boxes. Do some research and contact a financial planner and a tax professional for perspective on your new state. Taking these steps will help you look at the many factors that come with moving and help you avoid making a bad decision that could be difficult and expensive to unwind.

Q: I am planning to retire next year. What should I be doing to prepare given uncertainties in the markets and economy?

Your question is understandable in light of current economic and market circumstances. In addition to the pandemic’s human and healthcare impacts, we will feel the economic fallout for years to come. But that doesn’t necessarily mean you have to rethink or postpone your retirement.

Much of what you should do has nothing to do with the pandemic or current market realities. If you have not worked with an advisor to create a plan for your retirement, do so. If you already have a plan, now is a good time to refresh it to make sure it provides the assurance you need to retire with confidence.

Here are a few recommendations as you enter your home stretch before ending career work:

- Understand your income sources. Social Security benefits provide a foundation for most Americans’ retirements. When do you plan to file for benefits? What benefits do you expect? Do you have other sources of income, such as a pension plan or rental real estate? While you may not be thinking about work during retirement, it’s a great way to stay engaged and keep you from dipping into your savings.

- Get a handle on your expenses. This can be tough. While you will spend less on some things during retirement, you will probably spend more on others. Less on dry cleaning, for example, and more on travel or entertainment. Paying off your mortgage or downsizing your home can also have a big impact on your expenses. Keep a log of expenses to get a sense of your current spending—and note items you think will increase, decrease, or go away altogether. This can provide a good starting point.

- Assess your portfolio. It’s important to remember that, even if you’re retiring in your 60s, you are still a long-term investor. You should plan for your portfolio to sustain your expenses (plus inflation) for 30 years—more if you have extra-long-lived family members. Your portfolio needs a growth element that is balanced with more stable investments to moderate volatility. Make sure to use up-to-date capital market assumptions that reflect the low-interest-rate environment we expect for quite a while.

- Run the numbers. With an understanding of your income, expenses, and portfolio mix, you can validate your plan. Try a retirement calculator that uses Monte Carlo simulation. This kind of simulation incorporates a range of potential market conditions and provides a sense of best case, worst case, and expected outcomes. Tweak the inputs to come up with a plan that you can live with. You may decide to work a little longer to provide a bigger margin of safety—or to retire immediately if the numbers look good.

- Stress test your plan. While a Monte Carlo simulation incorporates a wide range of market conditions, you may find it comforting to further stress test your plan. What if the market falls 20 percent during your first year of retirement? What if you decide to spend more early in retirement? What if you run into a big healthcare expense? Exploring these possible scenarios can provide further confidence in your plan’s durability.

It’s important to realize that retirement is not a set-it-and-forget-it endeavor. Make your decision to retire based upon a thorough analysis that builds in a comfortable margin of error in case things don’t play out as expected. Then, rerun your plan every three to five years or when something significant happens—like a big market move, selling your home, receiving an inheritance, or the death of your spouse.

Remember: Your goals and situation are unique, so make sure that you sit down with your financial, tax, and legal advisors to make sure that your plan is right for you.

The mood of an era is perhaps best captured by its futurists’ visions of tomorrow. An article by John Elfreth Watkins Jr., published in the December 1900 issue of The Ladies’ Home Journal (LHJ) titled “What May Happen in the Next Hundred Years,” envisioned a future of pneumatic tubes, airships, two-day Atlantic crossings, fantastically large fruits and vegetables, and other strangely specific predictions, such as the elimination of the letters C, X, and Q from our alphabet.

However, a few of the author’s predictions are strikingly relevant today, in the wake of the jarring disruption caused by the COVID-19 pandemic. Although many of the changes predicted in the article have been underway for years or decades, the pandemic has served as a growth catalyst for some.

Food

Watkins writes, “Ready-cooked meals will be bought from establishments similar to our bakeries of today. They will purchase materials in tremendous wholesale quantities and sell the cooked foods at a price much lower than the cost of individuals cooking. Food will be served hot or cold to private houses in pneumatic tubes or automobile wagons.”

Today’s pandemic has rapidly accelerated online ordering and delivery of food, whether restaurant meals (Uber Eats, GrubHub), groceries and other staples (InstaCart, Postmates), or meal kits (Blue Apron, HelloFresh). Of course, these meals are delivered not by pneumatic tube but by a decentralized workforce of smartphone-wielding gig-economy contractors. The widespread availability of food-delivery services during lockdowns helped both consumers and restaurants struggling to keep their doors open, although there are concerns about the long-term impact on restaurant profitability with such services often charging restaurants a 15 to 30 percent commission on every order.

Entertainment

With entertainment and sports venues shuttered by social distancing requirements, we turned in record numbers to at-home digital streaming entertainment. The digital availability of the Broadway megahit Hamilton helped drive more than 60 million paying subscribers to the Disney+ streaming service in the first nine months the service was available.

Watkins hits the mark again, writing in the December 1900 LHJ article, “Grand Opera will be telephoned to private homes and will sound as harmonious as though enjoyed from a theatre box. Automatic instruments reproducing original airs exactly will bring the best music to the families of the untalented.”

Consumer Staples

Watkins even forecasted a sophisticated system of package delivery in his LHJ piece. “Pneumatic tubes, instead of store wagons, will deliver packages and bundles. These tubes will collect, deliver, and transport mail over certain distances, perhaps for hundreds of miles.”

Again, the fascination with pneumatic tubes! E-commerce has grown at a breakneck pace since 2000 when Amazon extended its platform beyond books to a wide range of product categories. The pandemic has rapidly increased the range of products bought online, especially supplies difficult to find on store shelves, such as paper goods, personal protective equipment, home office equipment, and other essentials.

In this article, we will explore how technology has impacted our response to the COVID-19 pandemic and how the crisis rapidly accelerated trends already underway. As with any disruption, winners and losers have emerged, with potential impacts to investment strategy. Pneumatic tube investors of the 1900s were likely disappointed, while fortunes were made in the auto industry—and we seek to understand which firms will prosper, strengthen, and gain market share in our post-pandemic future.

The Quick Shift

As the COVID-19 pandemic forced the global economy into suspended animation earlier this year, markets reacted with the fastest-ever bear market. The S&P 500 Index fell 30 percent in just 22 trading days. Yet amid this uncertainty, businesses, organizations, and communities quickly adapted and found creative ways to do business in a bubble.

Clearly, many have suffered and continue to suffer from illness and the loss of loved ones, employment, and income, and we do not minimize the remaining challenges. But a potent combination of technology platforms—including widespread connectivity, e-commerce, cloud computing, and collaboration technologies—allowed many businesses to adapt to a fully remote, work-from-home world far more quickly than feared in mid-March. Technology is the only way to remain connected while physically distant.

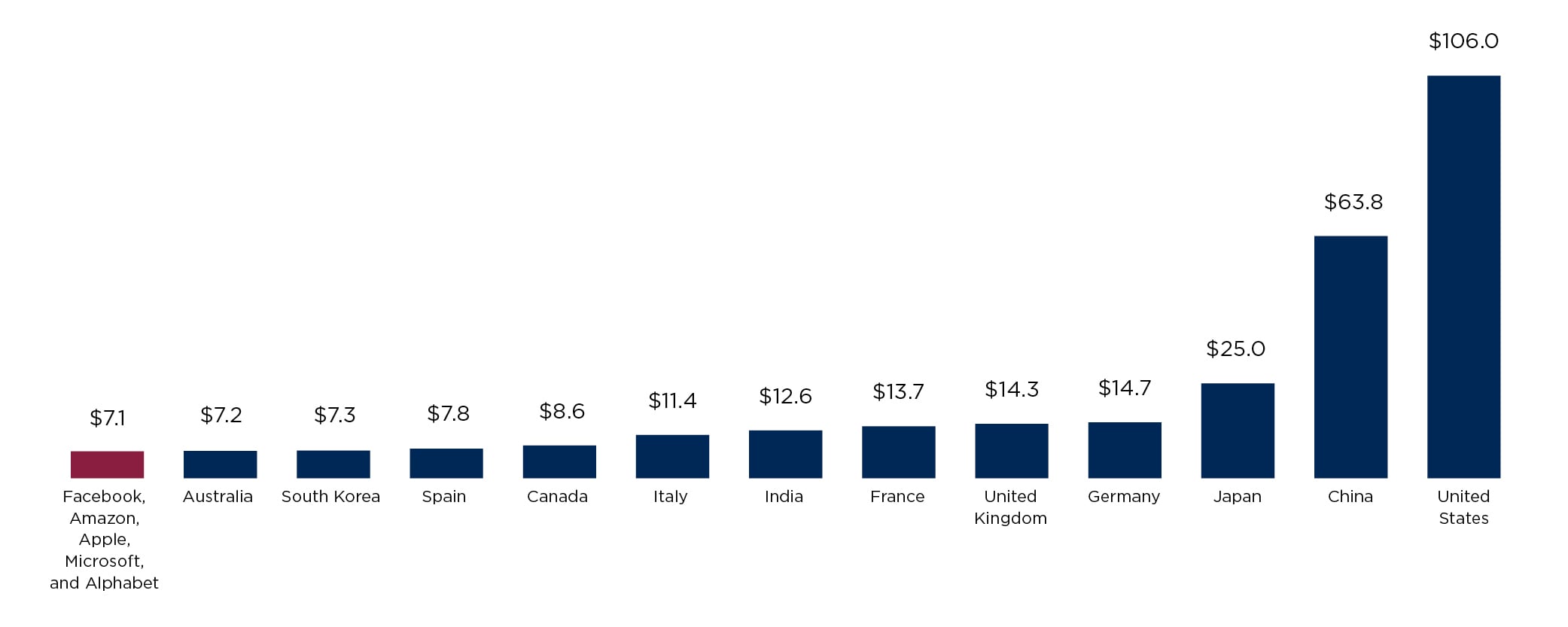

The digital platforms underpinning this transition were richly rewarded in the ensuing stock market recovery. Today, Apple alone has a larger weight in the S&P 500 Index than the entire energy and utilities sectors combined. And, as shown in Figure One, at $7.1 trillion, the combined market cap of the five largest U.S. firms— Facebook, Apple, Amazon, Microsoft, and Alphabet (Google), otherwise known as the FAAMG stocks—is greater than the national wealth of all but the 12 wealthiest nations on earth.

Figure One: Wealth of FAAMG versus 12 Wealthiest Nations (Amounts in Trillions)

Sources: visualcapitalist, Bloomberg

In addition to these technology providers, businesses and organizations that were leaders and early adopters of digital transformation also benefited relative to their competitors. Firms that were well on their way to moving infrastructure to the cloud and collaboration platforms; retailers with online and mobile ordering, curbside pickup, and contactless payment systems; and educational institutions with mature virtual learning platforms found themselves in a strong competitive position. Meanwhile, laggards that had resisted change faced a stark decision: invest in digital transformation or close their doors.

A 2019 study by Accenture sought to measure the performance gap between technology leaders and laggards. The authors surveyed more than 8,000 companies across the globe and assigned scores in three categories, including implementation of a wide range of key technologies, degree of adoption of these technologies once implemented, and their organization and culture of innovation. The performance gap was significant, with companies scoring in the top 10 percent (the leaders) showing double the revenue growth of the laggards in the bottom 25 percent.

This performance gap has likely grown significantly in 2020, creating a winner-take-all environment where larger, better-capitalized, and more innovative firms stand to gain significant market share from those less willing or able to innovate.

Tubes in the Walls

As painful as the pandemic has been, it is interesting to think about how much better prepared we were to withstand such a shock in 2020 than we would have been just two decades ago, when phones were used mainly for talking, medical records existed in manila folders, and business data and applications were locked in company-owned data centers. But when COVID-19 emerged early this year, critical pieces of infrastructure were already in place to support sheltering-in-place and the shift to work-from-home. The pneumatic tubes were already installed, ready to be turned on.

Three technology trends in particular have supported our ability to adapt to the crisis: the three Cs of connectivity, cloud computing, and commerce.

Connectivity

The single biggest contributor to our pandemic response is likely the pervasiveness of high-speed Internet connectivity. Imagine how different the work-from-home transition would have been if nearly everyone didn’t have a powerful, fully networked computer on their desk and in their pocket at all times. And consider how much less effective (and more frustrating) working and learning from home would have been over slow, dial-up connections.

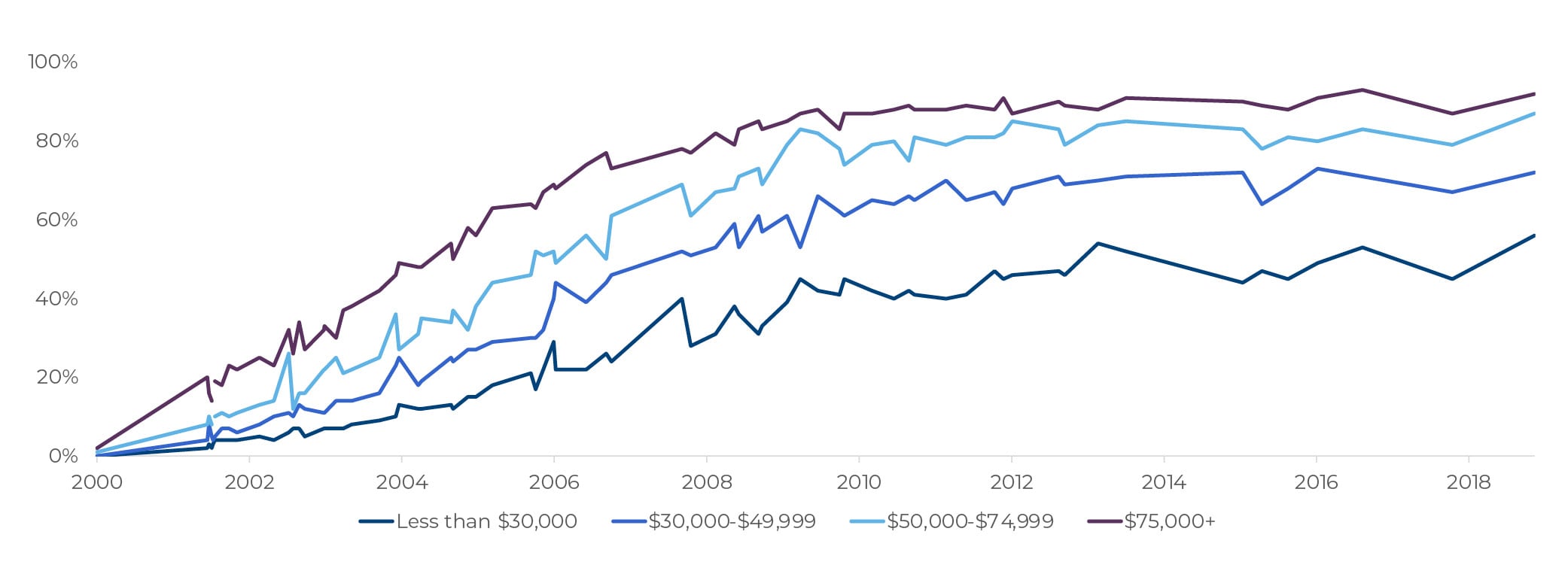

As of last year, almost 80 percent of U.S. adults had broadband Internet access at home, a number likely to grow with the expansion of high-speed 5G wireless networks. However, there are significant gaps in broadband access, with racial minorities, older adults, rural communities, and those with lower incomes showing a significantly lower degree of broadband adoption. As shown in Figure Two, only 56 percent of those with incomes less than $30,000 have broadband access at home, versus 92 percent for those with incomes greater than $75,000. The longer the pandemic crisis continues, the more damaging these gaps will become.

Figure Two: U.S. Adult Broadband Users, by Income

Source: Pew Research Center

An enduring shared experience of the pandemic will be the informal Zoom social gatherings, not to mention weddings and, tragically, funerals. In July, Microsoft reported that the use of its Teams online meeting software reached 5 billion meeting minutes in a single day.1 Social media platforms served as a vital way to connect and share information with friends and family while stuck at home, and as platforms for social movements.

Cloud Computing

Futurists in 1900 may have envisioned doing business in the clouds from the comfort of an airship. But today, cloud computing refers to the movement of computer hardware, data, and applications away from on-premises servers to Internet data centers, often providing advantages in reliability, security, the ability to scale up (or down) based upon demand, and greater speed to integrate future capabilities, such as machine learning.

The migration of computing applications to the Internet has been underway for more than two decades. But the modern era of cloud computing began in 2006 with the launch of Amazon’s Elastic Compute Cloud, a breakthrough service that allowed any business to rent Amazon’s world-leading Internet infrastructure.

New consumer applications of the technology are also emerging, such as cloud gaming, offering anyone with a high-speed Internet connection access to the latest cutting-edge gaming hardware. And regardless of their physical location, students studying artificial intelligence or even quantum computing can affordably access and experiment with highly specialized, extremely expensive hardware in the cloud.

An industry survey completed before the pandemic indicated that almost 60 percent of technology buyers expected to be mostly or completely in the cloud within 18 months.2 Polls taken after the pandemic show that the trend is only accelerating, with 40 percent reporting an acceleration of cloud efforts and 76 percent reporting an increase on cloud spending.3

Commerce

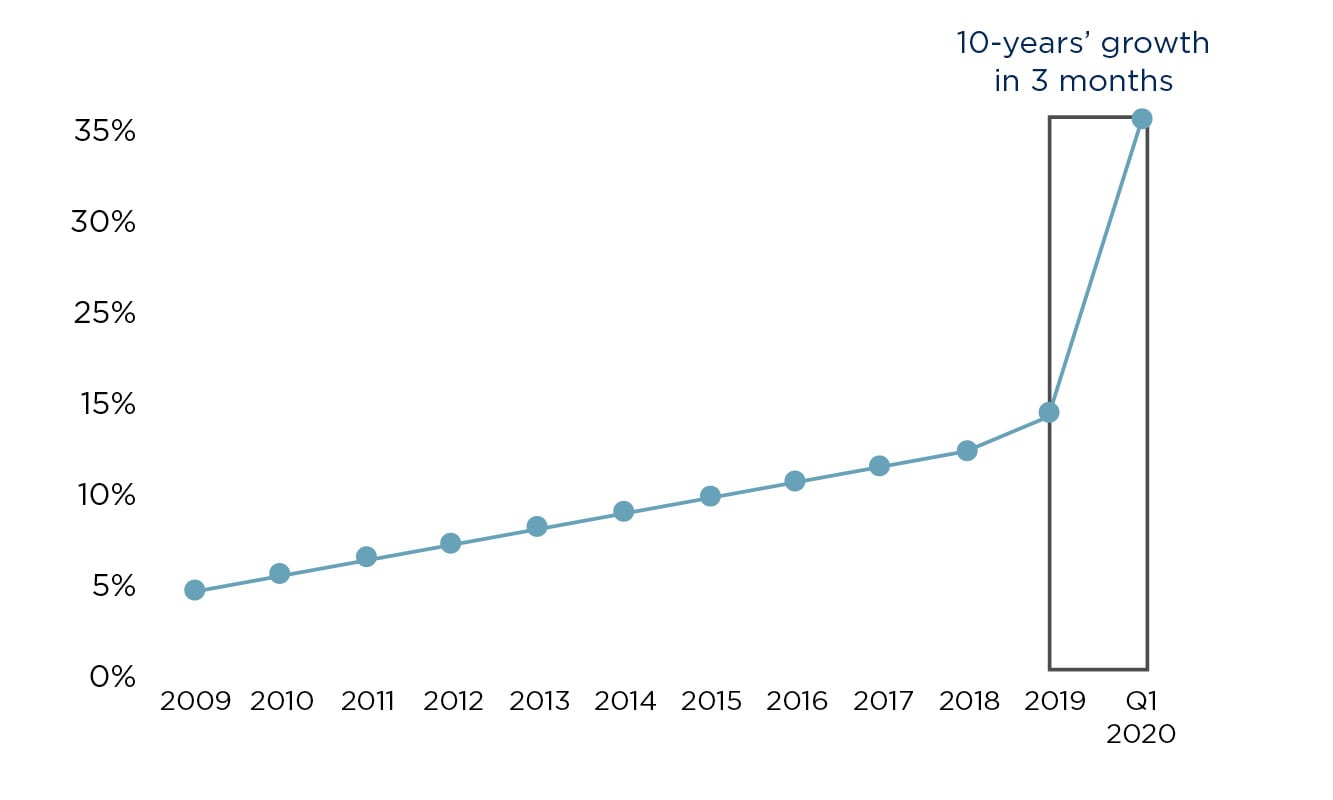

There was a time at the height of stay-at-home orders when it seemed that vehicles on the road came in just three colors: gray (Amazon), brown (UPS), and white (FedEx, USPS). While e-commerce has been a steadily growing influence on the retail world over the past 25 years, the pandemic has both accelerated and broadened it to include more product categories, businesses, and customers, representing both challenges and opportunities for traditional retailers. During the early days of the pandemic, as shown in Figure Three, it is estimated that e-commerce witnessed 10-years of growth in a span of just three months.

Figure Three: U.S. E-Commerce Penetration

Source: McKinsey

Historically, the growth of e-commerce has been driven by three factors: convenience, product selection, and price. However, as physical stores moved to restrict occupancy and with store shelves laid bare by demand spikes and supply chain disruptions, consumers turned to e-commerce out of necessity in new categories of goods. In March, the largest year-over-year e-commerce sales increases occurred in the categories of disposable gloves, bread machines, cough and cold medicine, staple food items, and exercise gear. The largest declines were seen in luggage and briefcases, swimwear, and bridal clothing/formalwear.4

It was not just the digital-native platforms such as Amazon that benefited from the surge in online shopping. The largest percentage change in online purchases was seen by traditional chain stores, signaling that the long-heralded transition to the hybrid clicks and mortar or omnichannel model has arrived. Firms such as Target that already offered this service saw usage soar by more than 700 percent, as others scrambled to launch their own. One survey of large retailers found that the number offering curbside pickup increased from 7 percent at the end of 2019 to nearly 44 percent in August.5

Implications for Investment Strategy

The CAPTRUST Investment Committee has been following these changes closely to consider potential impacts to investment strategy. Key themes include:

Dominant business models. The pandemic has pulled forward years of expected change into a matter of months. In an expected low-growth environment, we favor companies and sectors with strong balance sheets, higher return on equity, and higher earnings growth rates.

Uneven landscape. An uneven economic recovery creates winners and losers. Some businesses will continue to struggle and ultimately fail, while others will prosper. We continue to examine these dynamics for more resilient business models with tailwinds, search for shorter-term opportunities when price action overshoots, and consider the long-term impact of changes to corporate budgets and priorities.

Lean into disruption. We have begun developing disruptive innovation portfolios that seek to capture the potential long-term investment opportunities created by foundational technologies that will drive change and growth over the next 100 years, such as genomics, automation, autonomous vehicles, and artificial intelligence.

Amid the fear, uncertainty, and loss triggered by the pandemic, it is heartening to consider the resiliency and adaptability of businesses and communities in the face of a significant threat. While we may not yet enjoy the peas as large as beets delivered by pneumatic tubes (as predicted in 1900), we have witnessed rapid shifts in behavior, technology, and productivity, many of which will remain long after the virus threat has passed.

1 Microsoft Q4 2020 Earnings Call Transcript, June 2020

2 Knorr, Eric, “The 2020 IDG Cloud Computing Survey,” infoworld.com, 2020

3 Donnelly, Caroline, “Coronavirus: Enterprise Cloud Adoption Accelerates in Face of COVID-19, Says Research,” computerweekly.com, 2020

4 “Top 100 Fastest Growing & Declining Categories in E-commerce,”

Stackline, 2020

5 Ali, Fareeha “Charts: How the Coronavirus Is Changing Ecommerce,” digitalcommerce360.com, 2020

With the election right around the corner, now is the time to understand what tax changes may occur and what can be done to take advantage of the current rules. One such planning strategy is a spousal lifetime access trust (SLAT). A SLAT is an important tool for married couples with estate assets generally in excess of $20 million who are seeking tax savings now that may not be available in the future. Depending on the results of the November election, a potential reduction in the gift and estate tax exemption could substantially increase the federal taxes that are owed. Individuals and families should speak with their advisors as soon as possible to weigh the pros and cons of an estate planning strategy that utilizes SLATs.

Very often when there is a change from a Republican to a Democratic administration, estate and gift tax exemptions as well as tax rates become a political football. The estate and gift tax exemptions are currently $11.58 million for each taxpayer and this amount is subject to yearly inflationary adjustments. These thresholds were established by the Tax Cuts and Jobs Act, which was signed into law under the current administration in 2017. This means an individual can currently make gifts of property or cash to others valued at or up to $11.58 million over his or her lifetime without paying federal gift taxes. For purposes of federal estate taxes, this means an individual may currently have an estate of up to $11.58 million without paying federal estate taxes at death. It should be noted that if the exemption amount is used with gifts, the estate tax exemption is reduced dollar for dollar and only the balance, if any, of the exemption is available to reduce estate taxes. Estates and gifts over the exemption amount are currently taxed at a federal rate of 40 percent.

Estate and gift tax exemptions are subject to attack on two fronts. First, the exemptions are slated to sunset on January 1, 2026, meaning the exemptions will return to around $5 million, adjusted for inflation; and second, in the event the Democrats take control of the White House and Senate, they could reduce the exemptions more drastically and sooner than 2026 or increase the tax rate. For instance, a recent proposal by Senator Bernie Sanders advocated for a reduction of the exemption to $3.5 million. Other proposals are even more extreme, advocating for a reduction of the exemption amount to just $1 million. Despite these potential drastic changes, establishing a SLAT now provides a defense from both potential attacks while still allowing access to assets and the added benefit of tax-free appreciation.

Most gifting strategies require the taxpayer to give assets away with no strings attached. Couples with assets valued from $20 million to and as high as $75 million typically are reluctant to give away $10 million or $20 million in case they someday need the gifted assets. A SLAT, coupled with the purchase of some life insurance, may provide the best of both worlds: a completed gift, removal of trust assets from a couple’s gross estate, and a tax-favored leveraged death benefit, all while allowing a beneficiary spouse the flexibility of retaining access to trust investment values if needed in the future.

A SLAT allows one spouse to gift assets to the trust for the benefit of the other spouse or their dependents. This transfer to the SLAT removes the gifted assets from the estates of both spouses and depending on how the trust is structured, from the estates of the dependents. Further, SLATs are typically grantor trusts, meaning that the transferor-spouse is responsible for paying income taxes associated with the SLAT. This provides the transferor-spouse the option to pay the income taxes associated with the SLAT’s investments without the government treating the payments as an additional gift. Generation-skipping transfer tax planning can also be included in a SLAT.

In short, a SLAT allows for the avoidance of probate, avoidance of estate taxes, the transfer of tax-free appreciation, ability to own policies and pay life insurance premiums, and asset protection while still allowing some access to the assets in the trust.

Because any assets transferred to the SLAT are removed from the transferor-spouse’s estate, the spouse’s estate, and possibly the estates of their children, the assets will not be subject to probate and will not trigger estate taxes upon the death of either spouse or upon the death of the children even if the assets have appreciated in value. Any assets transferred to the SLAT are well protected from claims of creditors of the spouses and other SLAT beneficiaries. In addition to all of these benefits, the transferor-spouse does not lose all access to the assets because he or she can still indirectly benefit from the use of trust assets through the other spouse. As mentioned above, a SLAT is also an excellent way to own life insurance that could leverage the benefits.

If you think a SLAT may benefit you, you should start speaking with your advisor now, as some believe tax law changes may be retroactively enacted to January 1, 2021. Although there are many benefits to utilizing a SLAT, the best option for you will depend on your specific situation. Although we cannot predict the future of the estate and gift tax exemptions, one thing is certain: uncertainty. Planning now with a SLAT can help you take advantage of current exemptions while hedging against future reductions.

Even before research told us that pursuing our individual passions can have benevolent effects on the body and soul, Thurman could see that passion sparks a happy life and provides a way to transcend the ordinary. And if you move through life with passion, people notice.

Consider symphony musicians, who have polished skills but often become bored performing pieces over and over. A Harvard University researcher recorded one group of musicians that was asked merely to replicate a past performance. A second group was instructed to refresh their performance of a piece through subtle changes. Audiences overwhelmingly found the mindful performance to be more enjoyable, even though they didn’t know why.

Why does passion bring happiness? The answer may lie in flow, an enjoyable state that comes when you’re so absorbed that you forget yourself and tune out the world. This positive psychology concept from the University of Chicago’s Mihaly Csikszentmihalyi has reportedly influenced slews of world leaders and sports luminaries, including Bill Clinton, Tony Blair, and former Dallas Cowboys coach Jimmy Johnson.

Flow is “being completely involved in an activity for its own sake. The ego falls away. Time flies. Every action, movement, and thought follows inevitably from the previous one, like playing jazz. Your whole being is involved, and you’re using your skills to the utmost,” Csikszentmihalyi told Wired magazine in an interview.

For a deeper look at the play of flow in a passionately lived life, we asked three people with extraordinary passions to share their thoughts.

The psychology concept known as flow has reportedly influenced slews of world leaders and sports luminaries, including Bill Clinton, Tony Blair, and former Dallas Cowboys coach Jimmy Johnson.

Roy Heger, Ultramarathoner

Roy Heger found his passion for ultramarathons in middle age. He completed his first 50-mile race in Punxsutawney, Pennsylvania, shortly after his 40th birthday. Now 66, he has an astonishing 75 100-mile races under his belt. One favorite, the Massanutten Mountain Trails 100 Mile Run in Virginia, he’s completed 20 times.

Most humans of any age would consider running nearly four regular marathons in a row to be grueling, if not unbearable. But Heger makes it sound like nirvana.

“Running on trails like that, you lose track of everything except where you’re going to put your next step, and then next step. At night, your world goes down to a circle—you see only the light from your headlamp,” says Heger, who lives in Wadsworth, Ohio.

“In the deepest, darkest parts of night, you’re supposed to be sleeping,” says Heger. “When you run all night, you overcome that, and it changes your brain chemistry. As it gets closer to the second sunrise [of the race], there is a slight brightening in the eastern sky. You feel yourself getting stronger with the light returning. With that little boost, you begin to see, maybe I can make it.”

Heger runs without headphones or music, not even a watch. “A watch is a distraction and hinders achievement of flow. There’s no time inside of flow,” he says.

“Flow comes during exercise when all the fluids in your body are up to operating temperature, and you’re in the moment. Trying to achieve flow is like trying not to think about something,” says Heger. Instead, something about the long exertion, repetitive motions, and sheer physical exhaustion does the trick.

Heger says once you’ve tapped into flow, it spills into other parts of your life—when washing dishes, mowing grass, or weeding the garden. “When you see a dandelion, twisting this way and that, and you pull it just right so that you get the whole root out—that’s flow,” says Heger.

John Bukovac, Modern Gold Prospector

Did you know there are still flecks and nuggets of gold in creeks and streams across the U.S.? John Bukovac used to daydream about prospecting and finding “enough gold to make an engagement ring for a future fiancée or wife.” A few years ago, when he finally tried panning for gold, what he found was a hobby that he enjoys passionately and wants to continue for life.

Bukovac uses a plastic pan with grooves on one side and a classifier—a type of sieve for separating rocks from material that might contain gold. He also has a sluice, a narrow box with a multi-textured bottom that sits in the flowing water to separate gold from lighter material. It’s a modern version of the wooden sluices used by 19th-century prospectors.

“Every time you see gold in your pan or sluice, it brings a smile to your face. It never gets old, seeing that shiny, bright yellow popping out of the black sands when you’re washing your concentrates in your pan,” says Bukovac, 50, an engineer in Oberlin, Ohio.

Standing in the water and working with extreme concentration lulls him into a meditative zone. “The gold is so small here [in Ohio] that it can easily float on the surface and get washed out. You have to really focus on how much water you have in your pan, and the movements you use to clean the concentrates. It’s very easy to get lost in the process and lose track of time,” he says.

It’s not even about potential riches. “There’s nothing more relaxing to me than being on a creek or a river listening to the sounds and watching nature unfold around you,” says Bukovac. “You can make a little bit of money, but the pay is really the adventure. That’s invaluable to me.”

Stephanie Han, Writing Instructor and Author

A longtime writer and teacher, Stephanie Han says recent life upheavals threw her passions into sharp relief. The surprising result was that she was able to zero in on her true calling: guiding women and girls to be storytellers.

“I was divorced a few years ago. And, really, divorce is a type of death. But it also offers an opportunity to reexamine and reinvent. Like the phoenix, one rises from the ashes,” says Han, 55, who lives in Honolulu, Hawaii.

Then came the pandemic. Sheltering at home, Han pondered a new path. She loved teaching, but she’d been especially passionate about women’s issues from a young age. Her book of short stories, Swimming in Hong Kong, was chock-full of women protagonists. The writing group she’d started in the 1990s had attracted all women writers. “I saw there how the real narratives, even among those who occupy a privileged position in society, are often untold,” says Han.

The realization hit: “There is a gap in education for girls and women. Women want to write their stories down. It’s my mission to help them to craft their narrative. The better we write, the more clear we are with our prose, the more we can write into our dreams and stories and move to manifesting our lives,” says Han, who launched an online platform to offer writing workshops at drstephaniehan.com.

Getting clarity on her desire to help women storytellers has brought her great joy. “I am different now,” she says. “I wake up excited to think about what I will teach. I experience flow for most of my waking hours because I am living my life’s purpose now. I feel free,” says Han.

It’s never too late to pursue an interest that you may have put on the sidelines. Just put some time aside. Make it a gift to yourself. This commitment is what’s necessary, more than having any particular skills. “Especially as we age, it’s more important to have a great deal of passion about what you’re doing than it is to be good at it,” says Heger.

Your adult child would not have to pay the fees associated with a residential mortgage loan through a bank if you provide the loan at a lower interest rate than commercial lenders would charge. Also, the loan is as an income-generating asset in the fixed-income portion of your investment portfolio, says Jeremy A. Altfeder, CFP®, senior financial advisor at CAPTRUST.

An intra-family loan, in the right circumstances, can be “a really easy tool for parents looking for a way to do something nice for their children,” Altfeder says.

First Steps

This is not a do-it-yourself proposition, especially given the potential tax, legal, and other complications, says Lauren Campbell Maxie, an attorney and partner at NC Planning in North Carolina, whose primary practice area is estate planning for high-net-worth families.

Maxie says she gets the parents involved in a strategic discussion at the start, including their legal advisor, financial advisor, and others, to make sure they understand the details. She also brings in the prospective borrower early on, making sure he or she understands the benefits and obligations. “We tell them it’s a loan, not a gift, and that it has to be repaid,” Maxie says.

Parents may be uncomfortable with formalizing the loan, and they may not want the added expense of engaging various advisors, says Eric L. Green, an attorney with Green & Sklarz LLC, a Connecticut-based law firm, whose practice includes taxpayer representation before the Internal Revenue Service (IRS).

“But the reality is, if you do it correctly, you’re protecting your investment—and protecting the child” from creditors or would-be creditors, says Green, author of The Accountant’s Guide to IRS Collection.

“Everyone hates lawyers. I’m a lawyer, and I hate lawyers. But you’ve got to take the proper steps,” he says. For example, have the loan and related documents formally drawn up, signed, and officially recorded. That also helps avoid family fights down the road. “You don’t want a family to rip itself to pieces” over financial disagreements later on, he says. Also, keep track in writing of each payment to avoid unfavorable tax treatment.

Overall, you have to take a step back and make sure that the intra-family loan is the right fit for all involved, “because there’s lots of tools in the toolbox,” Maxie says. Altfeder agrees, saying, “It’s all about it financially making sense for both parties.”

A True Loan—with Interest

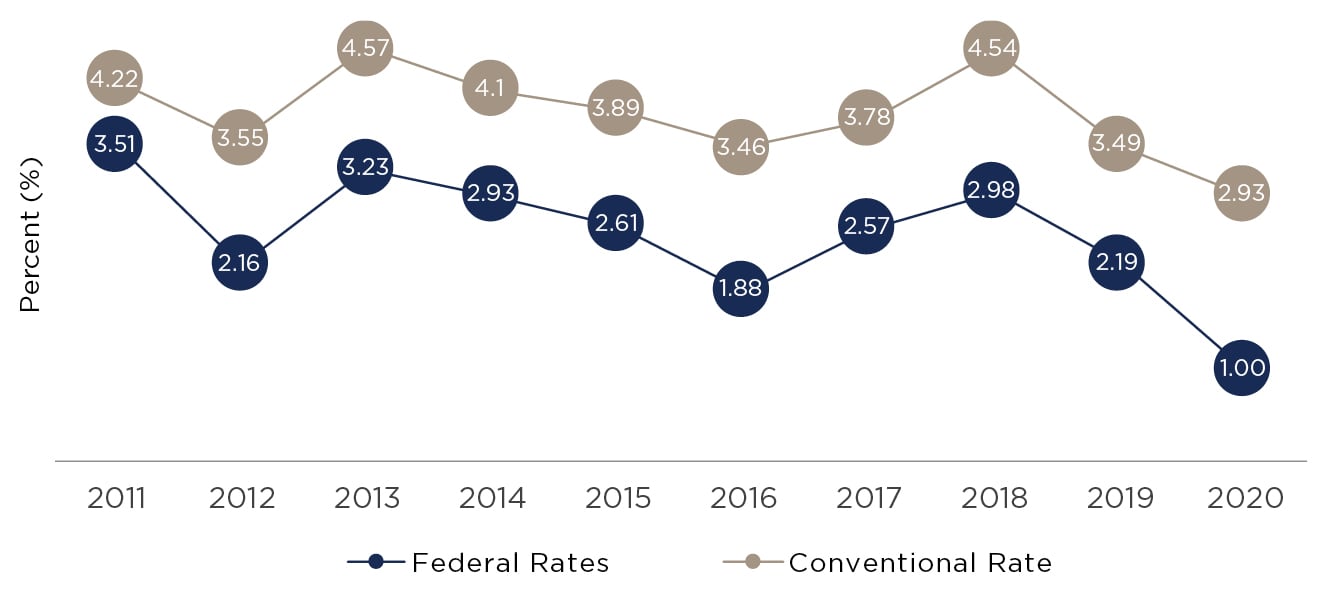

An intra-family loan must be a true loan, not a gift. Otherwise, it can trigger tax snags. To avoid such problems, charge at least a minimum amount of interest, using the rate from the table of applicable federal rates published monthly by the IRS.

Conventional rates for 30-year, fixed-rate residential mortgages lately have been among the lowest in at least 10 years—and the applicable federal rates for long-term intra-family loans have been even lower, as shown in the rate survey illustrated in Figure One.

Figure One: Interest Rates for Conventional Mortgage versus Applicable Federal Rates for Intra-Family Loans

Sources: Freddie Mac, Internal Revenue Service. Data is for 30-year fixed rate as of first week in September of each year. Data for conventional (i.e., bank) loans is based on Freddie Mac survey. Data for intra-family loans uses Internal Revenue Service’s long-term applicable federal rate.

At the time of the survey, the average fixed rate charged by banks was 2.93 percent, while the applicable federal rate for a long-term intra-family loan rate was 1 percent. That makes the intra-family loan “a great tool to look at while we’re in this low-interest-rate environment,” Maxie says.

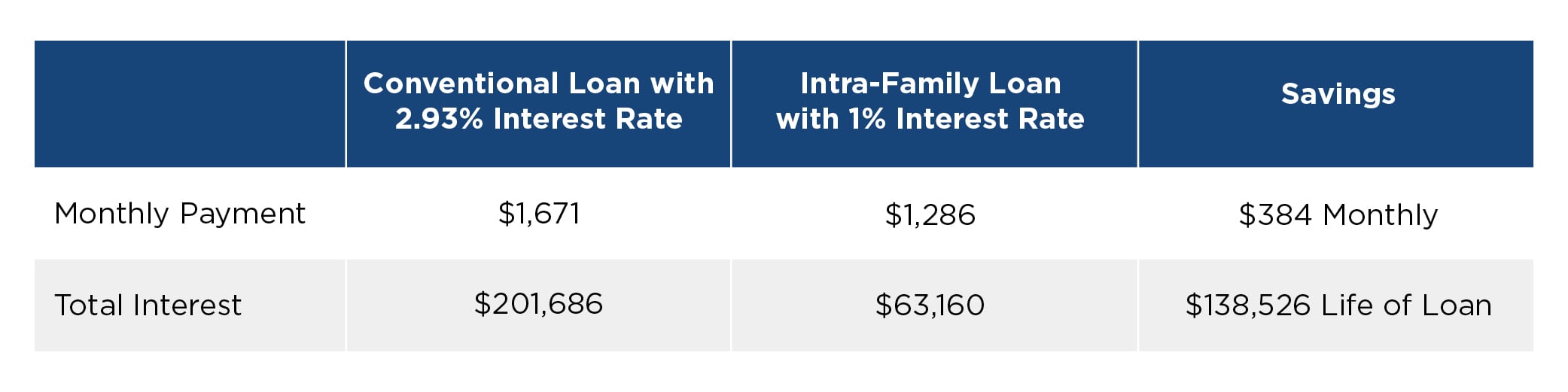

Suppose Harold and Maude plan to lend their son, Bud, $400,000 to buy a house. With a conventional 30-year, fixed-rate loan of 2.93 percent, he might pay about $1,671 a month in principal and interest as shown in Figure Two. But if he takes the loan from his parents, who use the long-term applicable federal rate of 1 percent, he’ll pay about $1,287 a month—saving about $384 monthly.

Figure Two: 30-Year Residential Mortgage versus Intra-Family Loan

Sources: Freddie Mac, Internal Revenue Service

Over the life of the loan, he’d pay about $201,687 in interest on the conventional mortgage, but about $63,161 on the intra-family loan—saving about $138,526 in interest expense overall.

An intra-family loan can also be from a grandparent, aunt, uncle, or any high-net-worth family member to a child or other relative. Such loans aren’t just for mortgages. They can also help the child or other relative pay college expenses, start a business, or accomplish other long-term family goals.

By following the proper procedures, no federal gift tax will apply and the interest paid by the adult child can generally be deductible as personal mortgage interest or as a business expense (depending on the purpose of the loan and other factors). And the interest received by the parent will be treated as ordinary income.

Flexibility

Intra-family loans can be more flexible than working with a bank, Maxie says. For instance, you can structure the loan as interest-only, with a balloon payment at the end, she says.

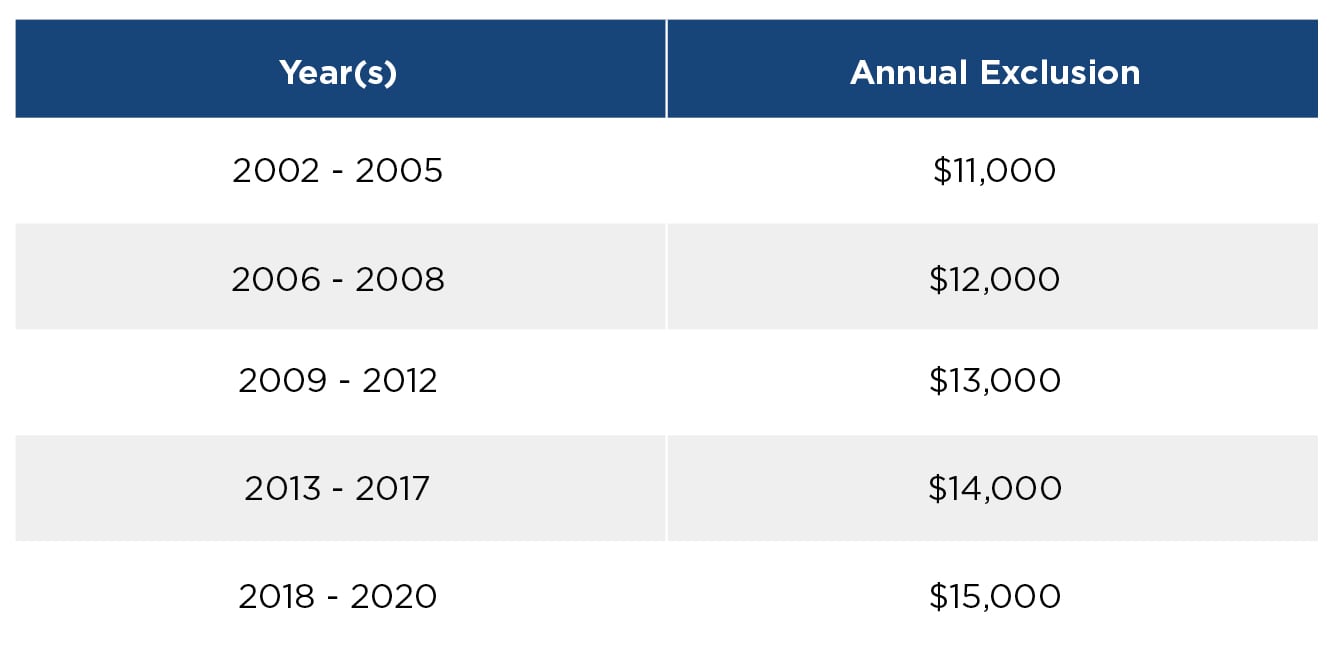

Another option is for parents to forgive some principal, perhaps annually, Altfeder says. Forgiving some principal on the back end can be the “icing on the cake,” turning a 30-year loan into a 15-year or 10-year loan, he says. Altfeder explains that to avoid federal gift-tax complications, be sure that the portion of the principal you forgive is within the annual federal gift-tax limit.

The annual limit—the annual exclusion—applies to each person to whom a gift is made and can increase each year, as shown in Figure Three. For 2020, the limit is $15,000 and the total amount of the gift can double if both spouses agree. In our example, Harold and Maude could forgive up to $30,000 of the loan’s principal each year, with no federal gift-tax consequences.

Figure Three: Federal Gift Tax Annual Exclusion Amount

Source: Internal Revenue Service

Suitability

An intra-family loan is best suited for those who can afford to offer it—typically high-net-worth couples who have a portfolio that sustains them in retirement and who are looking to help their adult children with a life-cycle event, such as buying a house or starting a business, Altfeder says.

Maxie says it’s not suitable if the parents need cash flow, or if the loan would affect the parents’ retirement. And according to Altfeder, he typically only recommends intra-family loans if the parents have at least $3 million to $5 million of liquid net worth.

Consider family issues, too. You may want to avoid making a loan if “it’s going to cause a big upheaval” in the family, Maxie says. Make sure that the family member borrowing the money will be in a position to repay it consistently. Overall, the intra-family loan is “a great tool. It’s just got to make sense for the family,” Maxie says.

Risks

Understand the risks involved. At the top of the list: “The kids stop paying,” Altfeder says. Family relations may suffer, too. So, follow the proper procedures from the start.

If the money is for buying a house, make sure the loan is formalized, with the various parties signing all of the mortgage, security, and related documents that would be involved if a bank were doing the loan, including having the formalized mortgage recorded in the local land-office records, Green says.

The same principle applies if the loan is for another purpose, such as helping the adult child establish, buy, or expand a business. Make sure there’s a promissory note [the written promise to pay], and a security agreement [giving the lender a security interest in the assets], Green says. Be sure, too, that the terms of the security agreement are filed under the Uniform Commercial Code with the Secretary of State and the local land-office records, he adds.

Intra-family lending isn’t for everyone, but in the right circumstances, “It has the opportunity to be mutually beneficial to the parents and the children,” Altfeder says.

Just make sure to get professional advice first, understand the family dynamics and risks involved, and make sure the proper steps are followed.

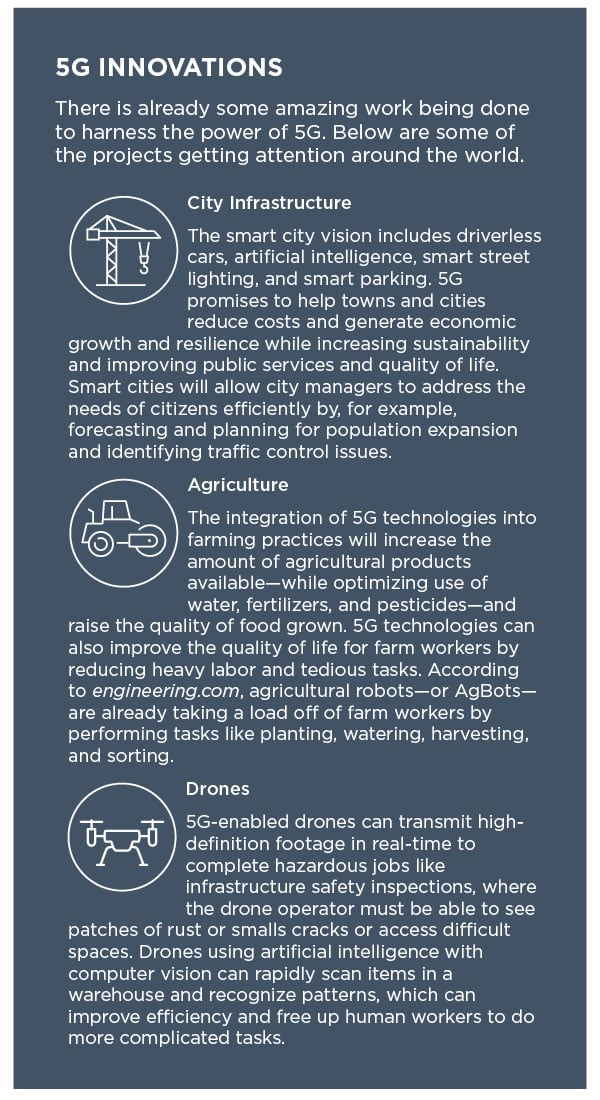

Faster Internet speeds have helped generate innovative new services and products. Think back to the early days of smartphones. Americans learned patience, along with the word buffering, as they waited in anticipation for a YouTube video to load on their phones. Now, 4G networks allow us to watch live events on our handsets and get real-time traffic reports on apps like Waze.

Game Changer

Proponents of 5G say it will be a greater leap than previous upgrades. “5G is a game changer,” according to Global Head, Telecoms & Media Alex Holt from accounting and corporate consulting firm KPMG. In a blog post earlier this year, Holt wrote that 5G “will connect everything and everyone and unleash the potential of technologies like artificial intelligence (AI), the Internet of things (IoT), augmented reality (AR), virtual reality (VR), and robotics.”

5G will push these technologies forward because of lower latency and greater bandwidth. Latency is the time it takes for data to move from one place to another across the network. Greater bandwidth means more devices can be online at the same time, moving us closer to connecting pretty much everything, including appliances, medical devices, automobiles, trucks, and traffic lights. This will push us further down the path of IoT. Experts say IoT will be the key to innovations in energy, traffic management, autonomous vehicles, and manufacturing because it will allow real-time interactions.

However, there is a darker side to IoT: security. More devices mean hackers with nefarious intentions will have more ways to break into systems like the power grid. Such security concerns will need to be assuaged before certain operators and manufacturers jump into the IoT world with both feet.

Mobile phone and tablet users will experience these advances in the form of very, very fast downloads. For example, Verizon says a video that took over two minutes to download on 4G will take 30 seconds on 5G. That’s fast enough to download an entire season of Game of Thrones in about a minute.

Verizon says a video that took over two minutes to download on 4G will take 30 seconds on 5G. That’s fast enough to download an entire season of Game of Thrones in about a minute.

Let’s look at health care as a sample of the potential of 5G networks. Imagine if you need brain surgery, you’re too sick to travel, and the greatest surgeon for your condition is in Europe. The low latency times of 5G combined with advanced robotics will finally make it possible to do precision surgery remotely. In fact, according to the Robotics Industry Association, a trade group, a surgeon in China successfully operated on a Parkinson’s patient from 1,500 miles away.

5G experts at the consulting firm McKinsey predict a revolution at home for medicine. Sensor devices on or underneath the skin can send heart rate, blood pressure, glucose level, and oxygen saturation readings to your doctor in real time. This can help patients manage diseases such as diabetes, chronic obstructive respiratory disease, heart failure, and hypertension, and cut down on doctor visits.

5G will also make it easier for artificial intelligence to scan vast amounts of data stored in the cloud or online. This will make it possible for physicians to input symptoms they are seeing in patients and make more accurate diagnoses.

Virtual reality headsets may finally stop making people dizzy and nauseous because images load too slowly. Live performances can incorporate virtual reality experiences that can be seen through the lens of a mobile phone as an overlay on reality; virtual balloons or bouncing balls can appear to be thrown in the air by a performer.

Unfortunately, the road to 5G is filled with potholes. Earl Lum, founder of ELJ Wireless Research, thinks many of the promises of 5G, such as remote surgery, will take a while to reach most people. “Availability of something like that is probably five to 10 years away in terms of someone trusting their life to someone thousands of miles away,” he says.

The Lengthy Deployment

Deployment of 5G is being hindered by concerns about security, health, and regulatory issues.

On the health front, there have been some wild conspiracy theories making their way across the Internet, including the belief that 5G causes COVID-19, a claim that has no scientific basis. The Federal Communications Commission (FCC) says “the weight of scientific evidence has not effectively linked exposure to radio frequency energy from mobile devices with any known health problems.”

But health concerns about 5G may have some merit, and they may be a real hindrance to its deployment. In fact, more than 400 scientists in Europe have signed a petition asking for a delay in the rollout of 5G until further study of its health impact.

Some scientists and lawmakers are skeptical of the FCC’s assessment. “The exposure limits aren’t even government standards,” says Joel M. Moskowitz, director of the Center for Family and Community Health at the University of California, Berkeley. “They were adopted from industry in the 1990s.”

Moskowitz argues there is a lot we just don’t know: “With regard to electromagnetic radiation, we hardly do any research.”

Part of the pushback against 5G has to do with the need for many small cells in order to get the lightning-fast speeds of what’s known as high-band or millimeter wave. Current cell towers cover a several-mile radius, but they are the size of tall pine trees. High-band 5G cells are the size of laptops, and they cover only a radius of around a couple thousand feet. Their reach also can be hindered by buildings, trees, and other objects in dense urban environments. So, telecom companies are hanging the cells fairly close together on telephone and light polls, and that is sparking pushback in many communities.

Residents in Northern California have been especially active in fighting against deployment. Cities like Mill Valley have enacted bans on placement of 5G cells in residential areas. However, a recent lawsuit gave the FCC the power to overrule most municipal ordinances, but cities still have some power over the deployment for aesthetic reasons.

There are two other types of 5G that don’t require such close placement of cells—mid- and low-band 5G. Neither mid- nor low-band wave has the lightning speed of millimeter or high-band wave, and low-band 5G is only slightly faster than 4G. But, because they need fewer cell towers and the signals are less easily obstructed, mid- and low-band 5G are likely to be much more common than high-band 5G.

It’s likely to take a while for entrepreneurs to develop applications that take full advantage of what 5G has to offer.

The immediate question most of us may be asking is: Do I run out and get the latest 5G phone? If you’re an iPhone user, you’re still waiting on Apple to release a 5G phone. For others, “It’s an incredible amount of hype from the operators and the industry,” says ELJ Wireless Research’s Lum.

He thinks most people will be fine with their 4G phones for quite some time. “At the end of the day, you have to ask yourself, what do I really need?” Lum thinks initially the only use for 5G on a handset will be for people who want to take and upload 4K video and photos.

Ultimately, faster speeds have always sparked new innovations—such as real-time traffic maps and live streaming. But it’s likely to take a while for entrepreneurs to develop applications that take full advantage of what 5G has to offer. For most of us, the promise of 5G will only slowly materialize over the next decade. That might be just in time for the launch of 6G.

When the Setting Every Community Up for Retirement Enhancement (SECURE) Act of 2019 became law, it included a long-overdue safe harbor provision for defined contribution plan sponsors interested in offering annuity-based guaranteed retirement income products in their plans.

“The safe harbor makes annuity selection very mechanical, very prescriptive, and very easy to comply with,” says Institutional Retirement Income Council (IRIC) Executive Director Robert Melia.

The SECURE Act’s safe harbor will protect employers from liability related to their annuity selections if they select a provider that, among other requirements, has been licensed by the state insurance commissioner to offer guaranteed retirement income contracts for the preceding seven years; has filed audited financial statements in accordance with state laws; and has maintained reserves that satisfy all the statutory requirements of all states where the annuity provider does business.

“This provision has the potential to alleviate plan sponsor anxiety about evaluating insurers by extending protections to sponsors who offer guaranteed income products,” says CAPTRUST Senior Director of Retirement Services Phyllis Klein. “By reducing barriers for plan sponsors considering in-plan annuities, the SECURE Act makes it easier for fiduciaries to meet the requirements that are imposed.”

Asset managers, insurance companies, and many plan sponsors around the U.S. have breathed a collective sigh of relief in response to the SECURE Act’s safe harbor. And while early indications suggest that a handful of interesting new guaranteed income-oriented products are in the offing, it’s important to remember that adding a new and potentially complicated product or service to a plan investment lineup may not be the solution to participants’ retirement income needs.

As with most things, there is no silver bullet.

State of Income-Oriented Products

Over the past 30 years, plan sponsors have shifted their focus from defined benefit plans to defined contribution plans to reduce benefit costs and fiduciary risk. This shift has brought innovation to defined contribution plans, including features like automatic enrollment, default contribution rates, and automatic escalation, to name a few.

However, while many employees see their large account balances as security for life, this shift has posed problems for many—mainly the loss of a reliable source of guaranteed lifetime retirement income, says Glenn Haskell, New Balance benefits director and New England Employee Benefits Council board member.

Today, fewer retirees are walking out the door with a pension check in hand. More likely, the retiree takes a lump sum 401(k) distribution into retirement with little idea how that balance translates into monthly retirement income.

But things could be changing for the better. Many plan sponsors are looking to help workers with retirement income generation and are offering up new options. Some of these options include modeling tools to help participants evaluate and compare withdrawal strategies, additional distribution options, and investment options such as managed payout funds and yield-focused fixed income funds.

In fact, SHRM.org reports that, last year, 30 percent of large employers offered one or more retirement income solutions, up from 23 percent in 2016. And the SECURE Act’s safe harbor is poised to move the needle even further by clarifying plan sponsor responsibilities around annuity provider selection for guaranteed retirement income solutions.

And while this new legislation is making strides to increase interest around solutions, according to Jeff Eng, managing director at Nuveen, it’s still very early.

“As of now, most plan sponsors are still in research mode,” says Eng. “Plan sponsors that are in the paternalistic camp are starting to wonder, ‘OK, well, how can we incorporate guaranteed lifetime income solutions into our retirement plan?’”

Some might be thinking about rolling out a guaranteed lifetime withdrawal benefit (GLWB). A GLWB is a form of group annuity offered to employers as part of an in-plan option. “It is sort of a cross between systematic withdrawals and the guarantees of a fixed annuity,” says Eng.

A GLWB offers the participant the ability to withdraw a fixed percentage of his or her account balance for life, starting at retirement. The guaranteed amount is based upon the amount invested and investment performance over time. Balances are generally invested in target date funds or asset allocation strategies appropriate for the participant, and the guaranteed amount can then increase if investment returns justify it, but it cannot decrease.

GLWB-based retirement income solutions have been around for years but have not achieved the lift-off that many providers had hoped for.

Eng believes that incorporating annuities within the qualified default investment alternative (QDIA) is the innovation needed to drive mass adoption through the simplicity of a target date fund. Further, offering a default investment with a guaranteed retirement income solution eliminates “analysis paralysis,” he says.

Automatically placing participants in a default investment with a guaranteed retirement income solution is a good thing, says Eng. It’s also going to help plan sponsors make sure participants don’t pass up the opportunity for a lifetime income stream simply because they were not aware it’s available.

“If you don’t make it a choice for them, and you just let them know [they have been placed in the plan default investment option], I think that’s the better option,” says Eng.

Managed accounts are another innovation that has been receiving a lot of attention lately. “Because they are tailored to the participant’s finances, goals, and risk tolerance, these accounts deliver a high level of customization and do not require a high level of participant involvement, if any,” says Klein. However, managed accounts traditionally have only offered investment guidance and advice during the accumulation stage for participants—and no income guarantees.

But that is changing. Some of these programs now include managed distribution modules to help participants move seamlessly from the accumulation to the decumulation phase with the assistance of personalized advice.

Some plan sponsors are addressing the need for guarantees by adding stable value vehicles to their asset allocation strategies, says CAPTRUST’s Mike Pratico, senior vice president, financial advisor. “The incorporation of stable value vehicles into the asset allocation strategy will give participants an element of guarantee.”

“And with the new safe harbor legislation, managed account providers are working on incorporating guaranteed retirement income products like annuities into their services,” says Pratico. It’s a very exciting area of development.”

The SECURE Act’s safe harbor has also nudged some plan sponsors like footwear manufacturing company New Balance into considering including access to an annuity purchasing service at retirement. “What we’re thinking now is to institutionalize the purchase process,” says Haskell. “Folks will be able to buy annuities under the umbrella of say, [an employer like] New Balance.”

“The idea is that New Balance makes that available to participants, to say, ‘Look, you’ve got a million dollars in your 401(k), and it might be prudent for you to take $500,000 of that and annuitize it for $2,500 a month for the rest of your life.’”

Among the newer annuity products available to help bridge the gap to sufficient retirement income are qualified longevity annuity contracts (QLACs), which let participants move 25 percent of their plan assets, up to $135,000, into an individual retirement annuity that typically begins making distributions at or before age 85.

While the number of workers interested in purchasing a QLAC is small, the Employee Benefit Research Institute (EBRI) measured the impact of QLACs in its Retirement Security Projection Model and found the product can provide great benefits for improving financial security for older seniors.

Create Context

Of course, adding a complex product or service—guaranteed or not—to a plan investment lineup is not a silver bullet. Without communication and education targeted at the right participant segments, adoption of new features can be destined for a lackluster future. Plan sponsors need to be prepared to communicate clearly and actively with participants about retirement income solutions if they want adoption.

According to Melia, it’s probably not worth a plan sponsor’s time or effort if they are not committed to a participant launch campaign for the product. “Unless you promote it, unless you really spend the educational capital that you need to educate folks, you’re not going to get a return on the effort that you put in,” he says.

There is a lot of room for improvement on the education and marketing front, especially for guaranteed retirement income solutions, Eng says. “I think the marketplace has to do a better job in education and marketing these types of distributions and not just call them annuities but call them guaranteed lifetime income solutions.”

When properly implemented and communicated, however, lifetime income solutions can make your plan a better human resource management tool that “helps achieve the goals of the organization by managing, protecting, and securing your most precious resource: your human resources,” says Melia.

A good example of an effective communication campaign is Yale University in New Haven, Connecticut. With the help of the university’s recordkeeper and the plans’ investment consultant, Yale’s four defined contribution plans now offer a custom target-date series that includes a guaranteed annuity within the QDIA.

Yale’s Hugh Penney, senior advisor for benefits planning, told Pension & Investments that the university went above and beyond last year to communicate the plan enhancements. Yale officials held dozens of town halls on campus and developed a detailed guide that explained all the moving parts, Penney said.

Yale leaned on its consultant for help selecting the products in its portfolio, and Pratico says that is a good idea. “A consultant might be helping to select the asset allocation strategy within a managed account or helping a plan sponsor select the best possible guaranteed income or lifetime income product,” he says.

Don’t underestimate how important good-quality advice is, whether it’s coming from the consultants or a recordkeeper, says Pratico. He points out that recordkeepers are often able to help with access to educational and promotional materials, solutions like income tools and calculators, and systematic withdrawal programs that address income needs.

“I think a lot of our recordkeepers working with the plan sponsors are now starting to offer different tool sets that will help [participants] do projections in terms of how much they are saving, how they are investing for retirement, and how much money they will have when converting that into an income stream,” says Eng.

What’s Next?

Not a silver bullet, unfortunately. “I think [the solution] needs to be cheaper, simpler for participants to understand and utilize, and yet still provide them with the ability to not outlive [the benefits] but also to give them access to their assets,” says Eng.

For plan sponsors committed to offering retirement income, consider discussing these questions with your retirement committee and financial advisors to determine what strategy works best for your organization:

- Do you understand the costs of offering a solution, and do you understand your fiduciary obligations in making any decision regarding income solutions for your plan?

- How will retirement income information be communicated to participants—at launch and ongoing? How will it appear on participants’ statements and online accounts?

- What happens when a participant leaves the plan? How will the retirement income solution be impacted?

- Will the solution provide an in-plan guaranteed retirement income option as the plan’s QDIA? Where will it sit in the investment menu?